News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

RIP IRECQ

IRECQ SEC Suspension:

http://www.sec.gov/litigation/suspensions/2014/34-72611.pdf

Order:

http://www.sec.gov/litigation/suspensions/2014/34-72611-o.pdf

The saddest part of this whole mess is that the technology works, it only needed some additional fine tuning to make it more robust and less prone to operational failures. Management had two options, spend an additional $100K on refining the very technology they are peddling to the companies out there or spend it on lavishness to support their upper management status... it's pretty obvious what choice they made....

As the echo of your applause fades, a heavy wall of silence falls like a guillotine blade upon the neck of spoken opinion. A stainless blade still wet from fresh kill in chapter 7.

THAT post almost made it worth losing my money here. LOL Sheer brilliance! Standing ovation. Bravo my friend, BRAVO!!!

He was the wished-upon falling star -- MIA in the final act. A suddenly falling star or important name dropping? The brilliant flash of light in the night, as Springer exits from center stage? Effectively, a curtain tugging [desperate?] non-event, slamming the casket lid on IREC -- buried [alive?] with tainted memories forgotten. A coroner's report was not requested.

A fanciful casket designed by whom, is the million dollar question. Six zeros and the big number one. [shrugging shoulders]

The near-death experience leading to the final and total abandonment of the common shareholder, continues to interest and amaze me. The story of IREC now rests within an unmarked grave. Meanwhile, the vital organs go elsewhere... leaving us haunted by the ghost of a slaughtered dream. IMO.

Hi was doing some research on the guy...who is Owen Shuler?

The disclosures of illegalities made by IPRC's whistle-blowing accountant provided proof of an effort to destroy the company. I was hoping for a better outcome, considering the company was internally wounded and made to bleed.

The health of the company directly impacts the shareholders. 'Therapy' for recovery from such deliberate acts and damages, was at least necessary to regain strength and develop forward momentum. But here we are, a crippled company with shareholders as roadkill now left to die....

This fractured story doesn't end well. The head was chopped off the goose able to lay the golden egg, IMO.

No big surprise. Probably can't pay the hosting fees.

The Adversary cases filed by IRECQ are also getting dismissed because of the conversion to CH 7.

It is the beginning of the eventual liquidation of the company.

I'm more amazed that there are buyers at any price.

Over a million shares dumped yesterday. Getting out with whatever they can before common shares are cancelled. I am always amazed at how many investors ultimately end up just eating their shares in these cases and actually never sell.

No Owen Shuler, no $1.4 MM dollar cashiers check, no common shares surviving.

Stick a fork in it.

Regarding the mystery money man - Owen Shuler. (Did he ever show up in court with the check?)

adstrategiesconference.com/43

Owen Shuler

CEO, Shuler Capital Corp.

Before becoming CEO of Shuler Capital Corp., Owen Shuler's career started with family interests during the 1970s in health care, construction and real estate. It has evolved over 35 years from advisory work in several sectors to leading an aerospace technology startup serving the U.S. government, and eventually to the early stage projects development or takeover of projects-in-progress in the transportation infrastructure, communications, medical and energy technologies industries. SEP was started by Shuler Capital Corp. in 2005 to hold an initial investment in a natural gas prospect, and it spun out as a stand-alone entity in 2009 as a private M&A platform for middle market O&G and electric power generation utilizing fossil and renewable fuels.

Same guy?

Barely anybody is following this one IMO. And even more so Springer's credibility is so shot at this point.

Well concerned wouldn't be the issue. Paid off might be. I can't imagine they wouldn't be happy with cold hard cash, if that's what's going on.

The creditors would continue to push forward until that check is in hand. Wouldn't you?

Then again, I wouldn't be surprised at this point if even that cashier's check doesn't arrive.

Thanks.....bizarre for sure. I wonder how the number $1.6 million came up?

What's the total debt again, not including insiders? $3 or $4 million?

Kind of interesting there was no buying on this 'news'. In all Ch11 cases in any turning events there is some form of pre release accumulation. Might not be overwhelming but it is always there. Too many parties involved with front knowledge.

Here .....zilch......just light selling.

Might not mean much ultimately but I would have expected something .

One last thing. These lawyers for both parties talk all the time.

It is not confrontational to them as it is to their clients, it is a business they are paid for and they have little emotional involvement.

In court they seem to get involved, and then out in the hallways they are joking around, and that includes the Judges also.

They wouldn't be 'blindsided' with the info in this Motion.

The counsel for the Creditors has been proceeding with all Motions right up to, and including the day this was filed, to convert to Ch 7.

It would appear they are not too concerned with this turn of events.

A few things.

It sounds like they don't even know if he is actually going to be there.

They state it is for funding the Modified Plan yet that plan has already been denied by the Court.

Like you mentioned it does not cover fully paying off the creditors.

And according to the now denied Modified Plan ( that may or may not be allowed to be resubmitted if these funds are actually presented....this Judge has clearly made several statements looking to end this) if the Plan does not adequately address Absolute Priority and any of the Creditors object to the POR Class 6 common shareholders get cancelled. And those thresholds were met on both accounts.

So although the check might show up, it is for a Ch 11 Plan that if resubmitted and ultimately approved looks to cancel Class 6 shareholders by it's own definitions.

Lastly, although a one time check might possibly be a stay of execution for Ch 7, this Judge has made it clear in denying the Modified Plan that the Debtor has generated no income since the inception of this case and thereby doubted the ability to continually raise the capital needed to execute the POR presented over the term of years the Treatment described for the Creditors Classes. My opinion would be the check is nice but the Debtor would have to convince the Judge it is more than a one time financing and that it is definitely, and without question associated with a source of future revenue.

I would love to be in that courtroom on Monday. It is either going to be very funny, or very ugly.

Mr. Straw,

I would be curious as to your opinion of this:

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=98091083

I realize $1.4 million doesn't cover all of the creditors, but it begs several questions.

Is there more money behind it?

Could IRECQ be actually closing a real deal, hence the financing?

Who is Owen Shuler?

Could this be the final hour savior of the shareholders I was hoping for but though there was no way (99% chance no)?

Sincerely,

Mr. Noc

THE PLOT THICKENS:

Imperial Petroleum Recovery Corporation (“IPRC” or “Debtor”), files this Conditional

Objection to Creditors’ Motion to Convert, and in support thereof would respectfully show the

following:

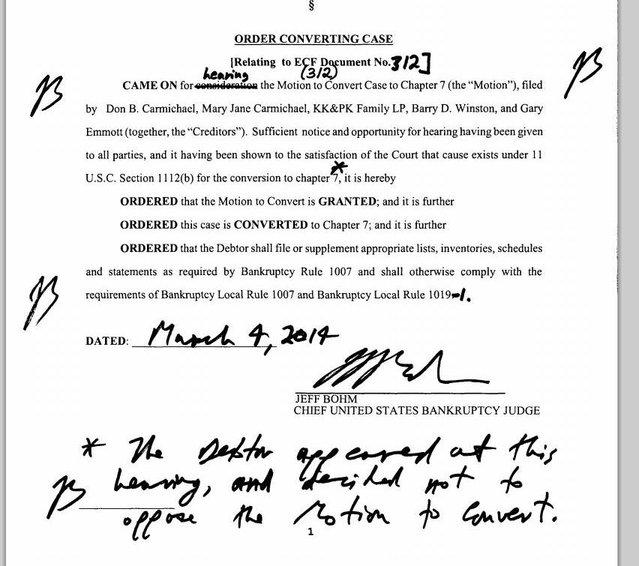

1. Debtor is still anticipating the appearance of Owen Shuler at the hearing

scheduled for 9:00 am on March 4, 2014, with a cashier’s check for $1,400,000 to fund the

Debtor’s Plan, as Modified. Failing same occurring, Debtor will not oppose the conversion to

Chapter 7.

https://ecf.txsb.uscourts.gov/doc1/178132922108

Dead Stock Walking. LOL

Nothing left to do but speculate and wait for the ultimate outcome.

Still one foot in and one foot out of the grave, until the next step proves otherwise.

I think it's beyond death row. IRECQ is strapped to the execution table waiting for the final injections.

Only hope is some last minute forensic contract evidence and a pardon from the governor. It's not looking good.

Someone seems to be buying shares today.

Oh well, good-bye to February. March hearing, coming right up. We're overdue for a big sale. It sure would help the share value and lift some spirits around here. Starting to feel like IREC is on death row.

Good-luck to us all.

Not enough hope yet for me to buy some even at subpenny. I'm hoping to find a reason to be optimistic again.

I believe there's room for more than 1% hope. At least, I haven't given-up on this thing. But I've quit speculating on what's next.

Good-luck to us all in March.

Agreed, but perhaps, at best, he was vastly overoptimistic since it's been 2-3 months since 8 different contracts were "imminent" yet there is still nothing. I have about 1% hope.

Seems like Springer wouldn't waste the effort, gathering funds, etc, at such a late stage, continuing on by doing all it takes to make the company compliant with the SEC and IRS, if sales weren't truly, almost, nearly, pretty much in the bag.

Another month about gone. No news doesn't increase my confidence, but still I keep looking and waiting. A signed sales contract would sure change everything fast.

Judges don't like being bullshitted. :)

The admittedly snowballs chance in hell is the same. Either the asshole (Springer) coughs up a deal that pays the creditors off and makes the court proceedings basically irrelevant or the shareholders are wiped out.

If by some miracle the asshole isn't full of shit, then time can only help shareholders and an extra month until the hearing is time (should be more than enough time). If Springer doesn't have something by then he's risking perjury IMO to keep talking about "imminent deals."

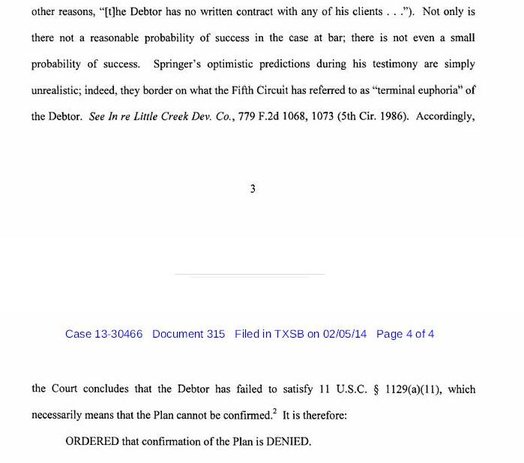

Order Denying Second Amended POR

http://www.scribd.com/doc/205239463/Order-Denying-Second-Amended-POR

Hearing is to convert to Ch 7 because the POR was denied ?

A long shot just became looking for nothing short of a miracle.

The Judge basically tells Springer he is full of shit for seeking Ch 11.

Using phrases like 'terminal euphoria', 'not even a small probability of success;, and 'simply unrealistic' is never good.

I'd expect a quick ruling on the Motion to Convert to Ch 7 hearing after reading those comments.

http://www.scribd.com/doc/205239463/Order-Denying-Second-Amended-POR

There's a hearing scheduled for March 4 now so it looks like the battle will continue at least another month and likely into April is my wild guess because that hearing then has to be ruled on and whatever other crap.

https://ecf.txsb.uscourts.gov/doc1/178132783319

It still give IRECQ time to land something though as each day passes Springer smells more and more full of shit about his "imminent" talk from now months ago.

That could be. Then again a month should be more than enough time for IRECQ to score a contract if it's not completely full of shit.

I won't hold my breath.

I doubt it will go on much longer. It will be over by end of month latest.

The Judge has stated a few times he is looking for a quick conclusion to the Ch11 process and even threatened to convert it back to Ch7 if they did not.

Some of these Judges are very clear in their desire to never let these small BK proceedings drag out and bog down their docket.

The ballots are already being tabulated and estimation hearing is over in order to proceed without Adversary Case.

I believe the Hearing on the POR is on the 7th.

That is only days away.

I saw that. Let me give you the quick summary:

Judge thinks IRECQ management is full of shit regarding landing any contracts (there's some specifics in there).

So IRECQ's only hope is to prove the judge wrong, and do it almost immediately, then take the resulting cash and pay off the creditors with it with an emergency order/request. I'm not a bankruptcy expert, but if IRECQ won a contract and got paid enough cash from it I have a hard time believing it couldn't then just pay off the creditors, and the creditors would have a hard time convincing the judge as to why they shouldn't take the cash.

The judge is asking for a hearing to avoid months or years of further litigation. This implies this crap still have some time to drag on either way giving IRECQ weeks, at least, to land one or more contracts.

In December IRECQ said each of 6 contracts were basically almost to be executed. Now it's February and still nothing. So, again, either they are full of shit or something is about to land. So far, at the very least in terms of timeframes, IRECQ is completely full of shit. We shall see. Would love them to actually land something and load, but I won't buy without some evidence of this. I doubt very many are even watching besides you and I so I think I'd have an edge to buy cheap if in the unlikely event IRECQ actually accomplishes something in this final hours.

Order Regarding Estimation Of Claims 1/31/2014

http://www.scribd.com/doc/204030965/Claims-Estimation-Order

Not good for Debtor. Not reduced by much at all.

How would the market know, though? They have like TWO employees. I doubt anything would be leaked. If and when a final contract shows up, I imagine we would know publicly almost instantly and there wouldn't even be time for a leak.

It just seems too good to be true that all these years other than Petrobras they have had jack shit then all of a sudden six monster deals will close all at once just in time to save the entire company. That being said, I don't think the share price could possibly leak it IF the story(stories) are true. The only ones truly in the know would be the customers themselves.

Likewise, if those customers are serious, they have to know about the bankruptcy proceedings so it's a question if they want to deal with current management of the debt-holders who seem like dickheads. I guess the dickheads may accept better terms for the contracts though in which case IRECQ is toast.

But again, who knows. I wish there was concrete info in the positive so I can slam the ask, but there is none as of yet. Watching for new court filings 2-3 times a day just in case.

My thoughts exactly. If there was even a snowball's chance of the contracts happening and a payoff of the creditors as well, the market would tell us the story with volume. The fact there is ZERO volume tells us this thing is DEAD!

As we already discussed, if IRECQ magically gets the contracts it is claiming to the court *cough, yeah right*, then they can pay off the creditors in full with cash, and they go away.

Obviously a massive change in assets, should it occur in the final hour, would change the settlement. "Your honor, we would like to pay off the creditors in full."

Obviously I'm extremely skeptical since there's zero volume today or I'd be buying at the ask. But if you believe what the company is telling the court, it's very possible.

We will see. I will be shocked if something comes through, but stranger things have certainly happened.

Actually all the objections to the POR/DS by the higher classes will deem that equity should be cancelled under Absolute Priority.

The revised DS had this in it's revisions.

Remains to be seen either way. It's still being battled in court while supposedly contracts are being finalized that could supposedly turn IRECQ from rags to riches literally over night. The details of which are in several pages of the court filings. Unless those details are fraudulent or badly exaggerating, there's still hope of a monster. That said, IRECQ has a history of exaggerating at least in terms of timeframes or at least way overoptimistic. It also has a history of delivering with Petrobras. It can still go either way.

The stock trading at half a penny or two pennies doesn't tell us if it's going to zero or going to a dollar. The court records tell us, not the trading of a stock that sometimes goes weeks without a trade.

Well IRECQ has tanked. Looks to me like the doctor has pronounced this patient DOA. R.I.P. IRECQ

I'm finally taking a peek at the court stuff again. Creditors calling bullshit on the pending contracts and want to move forward and reject IRECQ's plan of BK. IRECQ claiming with detail all sorts of contracts about to happen. What a drama story. It sounds way too good to be true by IRECQ despite the details though why would the creditors be so anxious unless there is something of value. Both sides sound full of shit.

We shall find out soon....

Total Potential Contracts: $23,445,000 from 6 different prospects.

Total closed so far: 0 for 6.

Prospect 6: expected to begin in January 2014

Prospect 5: waiting on final budget approval of that company

Prospect 4: nothing since Nov

Prospect 3: the company's general manager directed the documents be finalized by Dec 20.

Prospect 2: testing was to be done in Dec. 2013 for a Q2 2014 deployment

Prospect 1: firm contract was waiting on lab reports then start date in Q1 2014

5 of 6 prospects discussed conference calls in December and finalizations of contracts that made it sound any day. Now January 29 with nothing.

PROFESSIONAL TO BE EMPLOYED AND SERVICE TO BE RENDERED

1. Debtor seeks to employ Thomas C. Pritchard of the law firm of Brewer & Pritchard,

PC, a law firm with offices at 3 Riverway, Suite 1800, Houston, Texas 77056, to perform or provide

the following professional services: preparation of three Forms 10-Q and one Form 10-K for the

fiscal year ended October 31. 2012; and preparation of three Forms 10-Q and one Form 10-K for

the fiscal year ended October 31, 2013.

IV.

NECESSITY FOR EMPLOYMENT AND REASON FOR SELECTION

2. It is necessary for the Debtor to employ a professional to perform these services so

that the Debtor can satisfy certain requirements for making public filings required of public

companies by the SEC. Thomas C. Pritchard of the law firm of Brewer & Pritchard, PC is an

attorney who is specialized in the preparation and filing of such SEC required documents, and is

well-qualified to perform such services.

V.

PROPOSED ARRANGEMENT FOR COMPENSATION

3. Debtor desires to employ Thomas C. Pritchard of the law firm of Brewer & Pritchard,

PC on a flat-fee basis. Debtor has agreed to pay a flat-fee of $15,000, which includes the flat fee

of $5,000 for the filings in fiscal 2012, and $10,000 for the filings in fiscal 2013.

Filed 1/22/2014

Estimation Hearing for Class 3 creditors was yesterday and the day before .

Since their claims were failed to be dismissed by the Debtor they used the Ch 11 process to get the Court to decide on the value of their claims and how they will be treated outside of the adversary case..

This is potentially very bad for common shareholders if the Court rules for a low estimation.

It will most likely result in all, or some, of these creditors voting against the POR/DS and thereby potentially making Class 6 common shares cancelled per the treatment proposed.

"Claim Estimation: Potential Pitfall For Creditors In Chapter 11 Matters"

http://www.metrocorpcounsel.com/articles/18824/claim-estimation-potential-pitfall-creditors-chapter-11-matters

|

Followers

|

6

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

259

|

|

Created

|

03/21/05

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |