News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

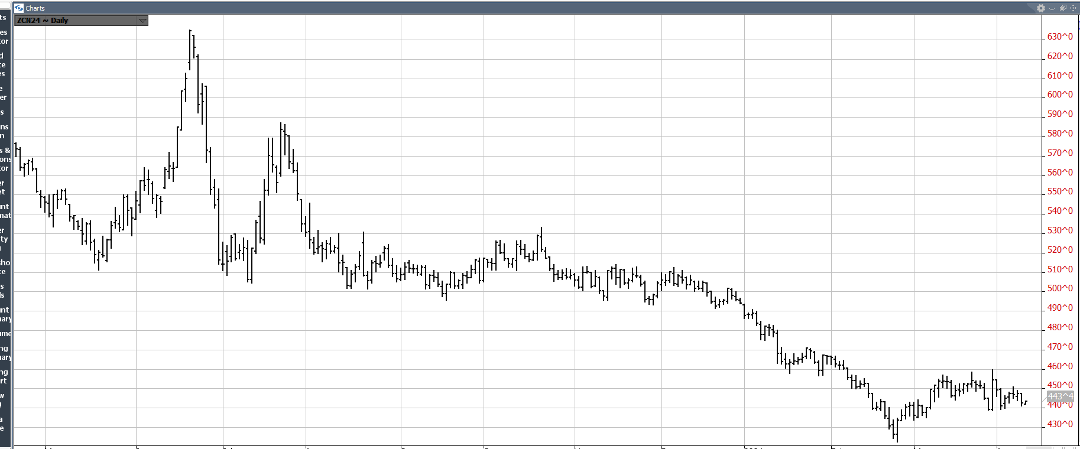

Natural Gas Rebound Faces Resistance at Moving Average Zone

By: Bruce Powers | April 18, 2024

• Trading in natural gas expected to be choppy, as volatility declines in the narrowing pennant.

Natural gas bounces to test a moving average resistance zone with the day’s high of 1.78. Today’s advance (Thursday) broke out above the high of Wednesday, which was an inside day. Natural gas is on track to end the day above yesterday’s high of 1.72. However, it remains inside the wide trading range from Monday, and it is also within a developing bearish pennant consolidation pattern.

Signs of strength seen today may take the price of natural gas up to the top boundary line to test resistance. However, it is not clear whether Tuesday’s swing low will be the low of the swing until there is an advance above Monday’s high of 1.80.

Choppy Moves While in Consolidation

Until natural gas breaks out of the pennant consolidation pattern trading will likely be choppy and difficult to predict, as with any consolidation period. Volatility can be expected to decline as the pennant narrows the trading range as the apex of the triangle is approached.

Further, the three moving averages representing different time frames of 8-Day, 20-Day, and 50-Day have converged. This is another indication of low volatility. How natural gas behaves when testing the upper or lower boundary lines will provide clues as you whether a breakout to the upside or downside may occur.

Consolidation Could Continue for Weeks

The pattern is bearish since natural gas remains in a downtrend and there was a sharp decline prior to the formation of the pennant. Nevertheless, it is not determined until a breakout occurs. A breakout either up or down should occur before the apex is reached. This means that trading within the pennant could go on for as long as more seven weeks. Regardless, a breakout could occur at any time as the pennant is already well defined.

8-Week Moving Average Recaptured

It is interesting to note that there was a breakdown from last week’s bearish shooting star candlestick pattern (not shown) before this week’s low of 1.65 was reached, leading to a bounce. Also, the 8-Week MA, which had marked support for the last two weeks was broken to the downside. Today’s advance has recaptured the 8-Week MA, a sign of strength. Confirmation of strength will be provided on a daily close above the current price for the 8-Week MA at 1.75. Natural gas exceeded that level today.

Read Full Story »»»

DiscoverGold

DiscoverGold

The Corn & Ethanol Report

By: Daniel Flynn | April 18, 2024

We kickoff the day with Export Sales, Initial Jobless Claims, Philadelphia Fed Manufacturing Index, Continuing Jobless Claims, Jobless Claims 4-Week Average, Philly Fed Business Conditions, Philly CAPEX Index, Philly Fed Employment, Philly Fed New Orders, and Philly Fed Prices Paid at 7:30 A.M., Fed Bowman Speech at 8:05 A.M., Fed Williams Speech at 8:15 A.M., Existing Home Sales, Existing Home Sales MoM, and CB Leading Index at 9:00 A.M., EIA Natural Gas Storage at 9:30 A.M., Fed Bostic Speech at 10:00 AM.,4-Week & 8-Week Bill Auction at 10:30 A.M., 5-Year TIPS Auction at 12:00 P.M., and Fed Bostic Speech at 4:45 P.M.

Grain futures are mixed in a reversal of yesterday with corn & soybean futures lower while wheat futures get a dead cat bounce. Low volume totals reflect lack of trading interest as the bulls & Bears debate the upcoming Northern hemisphere growing season.. Expect another choppy trade in today’s action with a modest bounce on Friday as we head into the weekend with many geo-political risks-on-at play. The Phillips 66Rodeo California Refinery (Rodeo Renewed) announced it is operating and producing 27,000 barrels of renewable diesel daily as of April 15th . Rodeo Renewable plans to reach it’s plant’s production capacity of 50,000 barrels per day later this quarter. At the current rate of renewable diesel production, the Rodeo Phillips 66 plant is consuming 8.6 Mil pounds of feedstocks daily with a push to reach 16.1 Mil pounds of feedstock consumption by late June. At capacity, this would add 15% of US biofuel production. Rodeo is the largest US biofuel producer and will significantly boost US renewable diesel production. Phillips 66 has not announced what feedstocks the plant will utilizing, but soybean oil should hold a sizable percentage of the feedstocks based on current price relationships, The US Soybean Crush industry has been waiting for Rodeo to come online for years. And talk of squeezing out more fuel from the Strategic Petroleum Reserves (SPR’s) instead of replenishing always at a loss from where and when the government tap’s into the Reserves. This is dangerous to National Security as the administration as both domestic and foreign policy extremely dangerous and just another self-inflicted failure that needs to be held accountable.

The Rosario Grain Exchange raised corn crop size questions on Wednesday with their crop size questions suggesting that corn stunt losses could grow with N Argentine fields reporting harvested yield losses of 40-50%. Also, corn stunt disease has pushed unusually far south into Central Santa Fe and Cordoba. BAGE may further lower their ’24 Argentine corn production estimate later today, but additional harvest data is required to define the disease’s full impact. Play It Again Sam! For the Bears & Bulls it’s the US Marine line of Hurry Up & Wait!

Read Full Story »»»

DiscoverGold

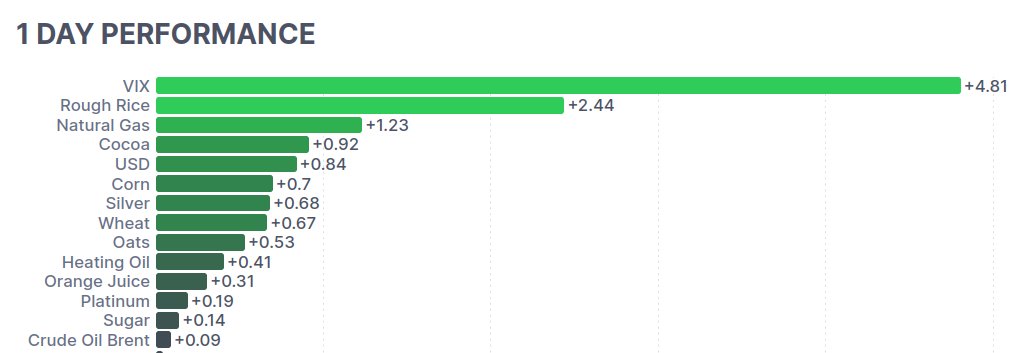

Commodities Daily Market Movers (% Price Change)

By: Marty Armstrong | April 18, 2024

• Top Movers

LBMA Silver in USD 0.74 %

• Bottom Movers

Tokyo Platinum Futures 2 %

NSW Baseload Electricity Continuous 1 %

Tokyo Rubber Futures 0.89 %

AU - Victoria Base-Load Electricity Futures 0.58 %

Tokyo Corn Futures 0.27 %

*Close from the last completed Daily

DiscoverGold

You Can’t Hurry Cuts. The Energy Report

By: Phil Flynn | April 18, 2024

Jerome Powell hints: You can’t hurry cuts. No, you’ll just have to wait. Inflations not easing, But It’s a game of give and take. You can’t hurry cuts, no, you just got to wait, just trust in the Fed’s time, it’s a game of interest rates. How many heartaches must we stand before inflation’s so tame to let us live again. Rate cuts were the only thing that kept us hanging on. When I feel my paycheck, you know it’s almost gone. No, you can’t hurry cuts….

Well after trying to hold support for days, the market had the rug pulled out from underneath it as the market seemed to lose the Fed and the Strategic Petroleum Reserve (SPR) put in quick succession. Backing off rate cuts and the Biden administration switching to a potential seller from a buyer for the SPR took away the invisible floor that oil had. We also saw an easing of war premium in part because of an Axios report that said that Israel considered a retaliatory strike against Iran on Monday but decided to wait.

The market also was less than inspired by the weekly Energy Information Administration (EIA) status report that seemed to suggest the gasoline demand in the United States is struggling but at the same time so are the inventories of oil products. Yet the tightness of diesel supply and gasoline, especially in certain parts of the country, seem to be overshadowed as the market tries to reprice oil and gas in an environment where we might not get any rate cuts this year after all and perhaps a measured response to Iran’s unprecedented attack on Israel.

Federal Reserve Bank of Cleveland President Loretta Mester seemed to echo the sentiment from Fed Chair Jerome Powell by saying monetary policy is in a good place, adding that the central bank shouldn’t be in a hurry to cut interest rates. Yet by backing off the suggestion that rate cuts would be coming, it took away what some might say was the Fed oil put that would keep a floor under oil just a day after the Biden administration took away the Strategic Petroleum Reserve put by saying that instead of buying back for the reserve they might be selling.

Add to that its seems that the market believes that the Biden administration will not impose sanctions on Iranian oil because they fear a shortage. Even so called reimposition of oil sanctions on Venezuela will not impact their exports to the US ahead of the election. Bloomberg News reports they intend to reimpose oil sanctions on Venezuela, ending a six-month reprieve, if Nicolas Maduro’s regime does not take steps in the next two days to honor an agreement to allow a fairer vote in elections scheduled for July.

The US plans to allow a Treasury Department license permitting oil and gas production to expire without renewal on Thursday, according to people familiar with the plan, who asked not to be identified without permission to speak publicly if Venezuela fails to act. Sounds ominous but as oil analyst Anas Alhajji points out, the reimposition of sanctions will not cover Venezuela’s oil exports nor U.S. oil imports from Venezuela. So, while the Biden administration is trying to act tough protecting free and fair elections, they are more worried about the price of oil and diesel hurting their reelection chances.

In fact, John Kemp at Reuters pointed out that Brent crude oil calendar spreads have continued to soften as traders downgrade the probability the conflict between Iran and Israel will escalate to the point where it disrupts oil production and exports. The spread from June to December 2024 has fallen to its lowest for more than five weeks. Most of the softening has come in the nearest-to-deliver June-July and July-August spreads where most of the speculative money is concentrated and where the supply-demand balance would be impacted most immediately by any escalation that threatened oil production and exports from the Persian Gulf. Traders have concluded Iran will not risk any disruption of its exports; the United States will not risk higher oil prices in an election year; and the United States will restrain the next round of responses by Israel. Then again, if it does happen, well, stay tuned.

How about gasoline futures which in recent days has been surging also saw the bottom drop out after the Energy Information Agency {EIA) report. The market became concerned about the strength of the consumer after another week of subpar 8.862 million barrels a day demand. Even though it was stronger than the week before, the market is concerned that this summer driving season might not be getting off to a bang up start.

We did see a big rebound in U.S. oil exports that surged to a whooping 4.726 million barrels a day, that probably included some post Easter Holiday work. Then I would have to say that the report really wasn’t bearish. In fact, I would suggest you could even see green shoots in this report that would suggest more bullishness in the weeks to come. Yet when we lost the Fed put and with the market taking off some more premium, we started the see people’s online positions after they took out support.

According to the EIA, demand in the four-week moving average, which is really what you must keep an eye on, showed that based on total products supplied over the last four-week period averaged 19.8 million barrels a day, down by 0.2% from the same period last year. Over the past four weeks, motor gasoline products supplied averaged 8.8 million barrels a day, down by 1.9% from the same period last year. Distillate fuel product supplied averaged 3.5 million barrels a day over the past four weeks, down by 8.4% from the same period last year. Jet fuel product supplied was up 0.8% compared with the same four-week period last year.

EIA said supplies of U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 2.7 million barrels from the previous week. At 460.0 million barrels, putting U.S. crude oil inventories are about 1% below the five year average for this time of year. Total motor gasoline inventories decreased by 1.2 million barrels from last week and are about 4% below the five-year average for this time of year. Finished gasoline inventories increased, while blending components inventories decreased last week. Distillate fuel inventories decreased by 2.8 million barrels last week and are about 7% below the five-year average for this time of year.

After taking off support both oil and products are vulnerable from a price standpoint. There is still geopolitical risk in the marketplace even though it’s been downplayed in the short term. If the demand side of the equation bounces back just a little bit, we can see by the inventories that supplies will tighten significantly. And while right now we are vulnerable to see oil retest near $80.00 a barrel, we believe it would be prudent to put on some call positions on breaks.

Gas producers are praying that today’s natural gas inventory report will throw them a lifeline so they can survive another week. The U.S. likely saw a below-average build in natural gas inventories last week, lowering slightly the storage surplus as the injection season gets under way, according to a survey by The Wall Street Journal. Natural gas in underground storage is expected to have increased by 45 billion cubic feet to 2,328 Bcf as of April 12, according to the average estimate of nine traders, brokers and analysts. Estimates range from a storage increase of 39 Bcf to one of 51 Bcf.t Journal writes that “the EIA is scheduled to report last week’s storage levels on Thursday at 10:30 a.m. EDT. The projected rise is smaller than the five-year average injection for the week of 61 Bcf and would reduce the surplus from 633 Bcf the week before. The large surplus over the five-year average follows an unusually mild winter that limited inventory drawdowns. The U.S. Energy Information Administration estimates that natural gas in storage will end the injection season at a record 4,120 Bcf, or 10% above the five-year average.

Read Full Story »»»

DiscoverGold

Natural Gas Volatility Decline Setting Stage for Pennant Breakout

By: Bruce Powers | April 17, 2024

• Natural gas is consolidating within a bear pennant pattern, with volatility declining as it trades inside a narrowing price range.

Natural gas further consolidates on Wednesday within a bear pennant pattern. It is on track to end the day as a relatively narrow inside day. Yesterday’s low of 1.65 approached a test of support at the lower trendline of a developing bear pennant consolidation pattern. This week’s decline has clarified that pattern as an attempt to hold support above the 50-Day MA and long-term trendline failed earlier this week.

Declining Volatility Likely to Continue

Volatility has been declining and it will likely continue to fall as natural gas further trades inside the small triangle pattern with a narrowing price range. The decline in volatility is also indicated by the three moving averages that have converged. The 8-Day, 20-Day, and 50-Day have come together.

What follows a period of low volatility is a clear increase in volatility. That will likely happen upon a breakout of the pennant. Natural gas remains in a clear downtrend and there was a relatively sharp decline prior to the pennant consolidation pattern. However, the downside may be limited.

29-Year Low is 1.44

In June 2020 a low of 1.44 was reached and price was quickly rejected to the upside. Natural gas traded below the prior support level of 1.52 for only one day before buyers took back control and the early stages of an advance began. That is the lowest price that natural gas has traded at in approximately 29 years. This means that 1.52 is a key low price to watch if a breakdown from the pennant occurs. Given the quick rebound off the 1.44 price level it seems unlikely that that price area will be tested again as support. Nevertheless, it is always a possibility.

Breakdown Signal

Until it is clear that Tuesday’s low of 1.65 is going to be a swing low, a breakdown is triggered on a drop below the earlier swing low at 1.59. It is confirmed on a daily close below that price level. Otherwise, support is likely to continue to be seen near the lower boundary line with trading contained within the pattern. Such a low volatility environment is likely to keep some traders on the sidelines until price breaks out.

Upside Trigger

Although the bear pennant is considered a trend continuation pattern, it is not valid until a breakout is triggered. Therefore, an eventual upside breakout remains a possibility. An upside breakout is triggered on a move above the recent swing high of 1.94. The next time that a bullish breakout could occur would be on the next rally towards the top of the pattern if it does occur.

Read Full Story »»»

DiscoverGold

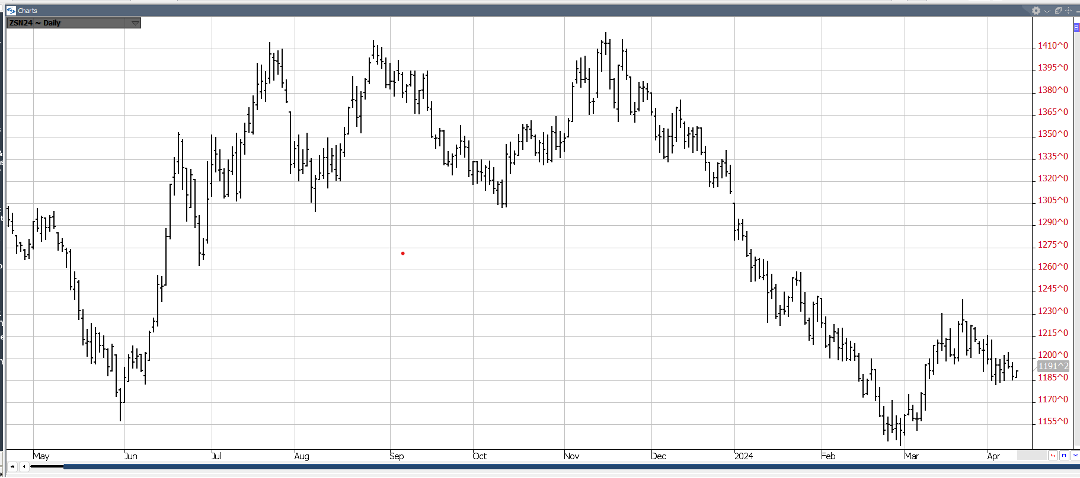

Agriculture Master Report

By: Bill Moore | April 17, 2024

JULY CORN

For the past 6 weeks, July Corn has been locked in a tight 20 cent range (440-460), as headwinds such as planting pressure, rains in the dry areas , the Iranian airstrike & the April WASDE Report push it down to the 440 level & tailwinds such as todays export at inspections 1.333 mmt & todays flash sale of 165,000 mt to Mexico lift it to the 460 level! Traders were generally disappointed by the wide disparity in the South American estimates tssued last Friday between the USDA (124) & CONAB (112) & feel the May WADSE will correct it! Common sense would say Brazil has a better handle on their crop size than the USDA!

JULY BEANS

1155 to 1230 has confined July Beans since Mar 1 as it also labors in a tight range buffeted by both positives & negatives! This past week, 3 export flash sales were reported to unknown destinations – 124,000, 254,000 & 124,000! But offsetting that was the USDA report last Thur at 11am CST – keeping the Brazil Beans at 155mmt vs the Conab estimate of 146mmt! This is a very wide discrepancy for this late in the growing season & we expect it to be rectified in the MAY WADSE REPORT! Meanwhile, the mkt is closely monitoring the early planting progress – with corn at 6% & beans at 2-3% complete – due out today at 3pm! With the mkt $2.50 under last Summer & a still sizeable short fund open interest, we feel the mkt leans to an upside bias – when it finally emerges from its sideways, consolidation pattern!

JULY WHT

July Wheat was able to back-and-fill its way higher for about a 40 cent rally – before the mkt’s negative reaction to last Thur’s WASDE forced a correction! However, we feel Russian’s recent export woes, the escalating Middle-East conflict, recent Russian military strikes & general dry conditions of their emerging wht crop all favor less production & more exports – and therefore higher prices!

JUNE CAT

Since late March, June Cattle has plummeted $16 (186-170) – mostly off the impetus of a bearish March Cattle-on-Report which reported placements at 10% over 2023 (est-6%)! The downswing was then exacerbated by the Bird Flu Epidemic which cast serious doubt on beef demand! However, this incident was later mitigated – leaving the mkt sharply over-sold! So, a fierce short-covering rally (170-176) ensued – sparked by our entry into the Spring Grilling season – the best demand period of the year! We look for the mkt to continue to recoup part of the $16 loss – triggered by the fateful March 22nd Cattle-on-Feed Report!

JUNE HOGS

On April 10th, a major Key Reversal occurred – with new contract highs scored early in the trading session – followed by a precipitous decline of nearly $5.00 & a close well under the previous 2-wk lows! The mkt continued down another $4-5.00 to last week’s low of about $101 – as heavier slaughter & pork production fueled the down! But after nearly an $8.00 drop, the mkt became quite oversold & being amidst the best demand period of the year, has rallied back $3.00! We look for all the outdoor grilling to push the mkt back up toward it early April highs! Helping that rally is the fact that China’s 1st Qtr pork production declined to 15.8 million tons – the first qtly fall in 4 years! This seems to indicate that they are finally getting their excess production under control – a positive for pork exports!

Read Full Story »»»

DiscoverGold

Biden’s Oil World. The Energy Report

By: Phil Flynn | April 17, 2024

Wars, rumors of war, record deficits, raging inflation and threating more taxes and regulations on US energy as Iran’s Oil production is allowed to hit a 5 and a half year high and they secretly meet with the Maduro regime while having to decide this week as to whther or not to impose sanctions. And now with the supplies of aluminum platinum tightening ask the CME Group and the London metals exchange decides to not deal with the Russian supply the Biden administration is now suggesting tariffs on Chinese metals.

Oil prices are pulling back as Israel has yet to respond to Iran’s unprecedented attack and stubborn inflation has Jerome Powell said that “If price pressures persist, the Fed can keep rates steady for “as long as needed” and the Biden administration and White House senior adviser John Podesta hinted at another release from the Strategic Petroleum Reserve to try to ease rising gas prices and try to improve his boss’s political fortunes.

The Biden Administration has made no bones about it that the mission of the SPR not just to be used in an emergency but as a political piggy bank where he can use taxpayer paid for oil to improve his political fortunes. Kind of like defying the Constitution and the Supreme court to use your money to pay off some college loans. Yes, President Biden has done this before releasing oil from the SPR before he welcomed a ‘minor incursion” by Russia into Ukraine and before his failed policy of deterrence with sanctions on Russia.

This comes as the American Petroleum Institute released a report that shows that gasoline inventories are tightening as well as diesel but did see an increase in crude oil supply. API reported that gasoline supplies fell by 2.51 million barrels in the current week. AAA pots gas prices at $3.660 A gallon up from $3.644 yesterday and up from $3.461 a month ago, Year over year they are about a penny lower, and that was when the market was getting regular released from the SPR that could be exported to China and India and Europe. Yes, oil exports in the US did hit record highs as we drained our SPR.

So, it’s probably good news that the API reported that we saw crude inventories rise by 4.09 million barrels, but it is more than likely that that’s going to change as refiners have to ramp up production. Gasoline supplies are below normal and so we’re distilling inventories and they fell to 427,000 barrels. The smaller than expected 169,000 drawdown and Cushing OK may be a sign that the crude oil supply increases could be coming to an end and that may pressure the Biden team to use SPR oil once again in an attempt to keep down gasoline prices.

First behind the backdrop is the market waiting to see how Israel is going to respond to that unprecedented attack by Iran on its own soil it seems like Iran is taking steps because I think they are starting to realize that after their failed assault maybe they bit off a little bit more than they can chew. Today Iran is talking about letting in nuclear weapons inspectors from the International Atomic Energy agency which would be the first time this year.

Bloomberg reported that Rafael Mariano Grossi, director-general of the UN’s nuclear watchdog, will visit Iran “soon,” the head of the Atomic Energy Organization of Iran said on Wednesday, according to the state-run Hamshahri newspaper. Mohammad Eslami said the date of Grossi’s visit had not yet been decided, Hamshahri reported. He also said that International Atomic Energy Agency cameras were installed and “constantly monitoring” Iran’s nuclear facilities. Remember the AP reported that the head of the International Atomic Energy Agency said Wednesday that Iran’s decision in September to bar several experienced U.N. inspectors from monitoring the country’s nuclear program constituted “a very serious blow” to the agency’s ability to do its job “to the best possible level” last November.

And while traders may be selling futures at the same time, we’re seeing a record amount of call buying for just in case scenarios some of the calls amazingly enough our way out of the money $250 Brent crude calls. If you buy enough of those options and you’ll get a spike in the price of crude oil you don’t have to get anywhere near $200 a barrel to do very well on a very cheap investment still it’s a long shot but it’s interesting that some serious money is making that bet.

of course geopolitical events sometimes really put a different perspective on good old fashioned supply and demand fundamentals. Once we see a significant change in the economic outlook the global oil market is going to continue to be undersupplied for the rest of the year. Misuse of strategic petroleum reserves around the world have discourage investment along with ESG responsible for taking away much needed funds from fossil fuel investment and putting them into other types of things that will not be able to help the global economy in the short run so it’s no wonder that these losing ESG investments s that were based more in false virtue instead of common sense Have some investors fleeing the sector and droves.

The American Petroleum Institute also is warning that Bidens lessee ban on Federal land is going to be bad for US economy and taxpayers. The API says “As energy demand continues to grow, oil and natural gas development on federal lands will be foundational for maintaining energy security, powering our economy and supporting state and local conservation efforts. Overly burdensome land management regulations will put this critical energy supply at risk. We are reviewing the rule to ensure the Biden administration is upholding its responsibilities to the American taxpayers and promoting fair and consistent access to federal resources.”

They point out some of the benefits that we will forgo such as the fact that “In FY 2022, onshore federal oil and natural gas development supported nearly 250,000 jobs, generated $19.4 billion in labor income, and contributed $36.7 billion to GDP.

In FY 2022, oil production on federal lands averaged 1.2 million barrels per day and marketed natural gas production averaged over 9 billion cubic feet per day. Between FY 2013 and FY 2022, oil and natural gas production on federal lands generated a total of $35 billion in disbursement revenue from bonuses, rents, and royalties, averaging approximately $3.6 billion per year. 53% of this disbursement revenue, totaling more than $19 billion, went to the federal government or programs, while state and local governments received the remaining 47%, totaling $16 billion.

In FY 2022, federal oil and gas development in the five highest producing states supported more than 170,000 jobs and more than 75,500 jobs in other U.S. states mainly through the supply chain and other purchasing. New Mexico: 105,300 jobs/ Wyoming: 24,400 jobs/Colorado: 21,000 jobs/Utah: 11,200 jobs/North Dakota: 10,000 jobs.

I guess we all wonder why that the Biden Administration is not as tough in enforcing Iranian sanctions and sanctions on Venezuela.

Who winters over winter is not over until we say it is. OK maybe that’s a little bit strong but we did get a little bit of a rebound in the beleaguered natural gas market after a report that we could get a may freeze. This is why here in Wisconsin you better not plant those flowers until Mother’s Day. Yet the overall outlook for natural gas continues to be bleak. EBW Analytics says that The mini rally in the May contract crashed lower last week as daily heating demand collapsed and acute weakness in LNG exports emerged alongside a bearish EIA storage surprise. Henry Hub prices in the $1.30s/MMBtu remain an alarming bearish warning sign of downside risks ahead of May expiration.

Acute weakness in LNG feedgas demand collapsing sub-10 Bcf/d represents near-term risks, although a probable rebound higher could help stabilize prices.

Natural gas production scrapes continue to descend more rapidly than projected, offering bullish upside into summer. Still, weak EIA storage figures pose a risk that imprecise pipeline scrapes may overstate supply losses. Near-term difficulties in sustainably lowering the storage surplus indicate likely continued weakness for near-term NYMEX futures. As weather headwinds ebb and storage surpluses decline into summer, however, natural gas may rise.

Read Full Story »»»

DiscoverGold

Lumber forming the dreaded tear drop pattern and is on track for its 11th consecutive red day

By: Barchart | April 16, 2024

• Lumber forming the dreaded tear drop pattern and is on track for its 11th consecutive red day.

Read Full Story »»»

DiscoverGold

Cocoa is crashing down 8.54% today

By: Markets & Mayhem | April 16, 2024

• Cocoa is crashing down 8.54% today.

Read Full Story »»»

DiscoverGold

Grains Report: Wheat, Rice, Corn and Oats, Soybeans, Canola and Palm Oil

By: Jack Scoville | April 16, 2024

• WHEAT

General Comments: Wheat was lower yesterday in range trading. Trends remain mixed in all three markets. The problems with Russian Wheat exporters continue. The reports indicate that the government is seeking more control of the exports and has made life very difficult on the private exporters in an effort to extract more sales and powers to the government. Russia is the world’s largest exporter and sets the world price and prices remain low. Big world supplies and low world prices are still around. Export sales remain weak on competition from Russia, Ukraine, and the EU as those countries look to export a lot of Wheat in the coming period. Black Sea offers are still plentiful, but Russia has been bombing Ukraine again and shipments might be hurt from that origin.

Overnight News: The southern Great Plains should get mostly dry conditions. Temperatures should be above normal. Northern areas should see mostly dry conditions. Temperatures will average above normal. The Canadian Prairies should see mostly dry conditions. Temperatures should average above normal.

Chart Analysis: Trends in Chicago are mixed. Support is at 539, 537, and 527 May, with resistance at 568, 575, and 580 May. Trends in Kansas City are mixed. Support is at 571, 561, and 552 May, with resistance at 597, 602, and 605 May. Trends in Minneapolis are mixed. Support is at 634, 625, and 618 May, and resistance is at 650, 655, and 660 May.

• RICE

General Comments: Rice closed sharply higher yesterday as the long liquidation by the funds is now complete. Futures were a little weaker at points during the week in reaction to the USDA supply and demand reports, but the rebound from the fund selling was more important. USDA cut domestic demand a lot but increased export demand for increased ending stocks levels. USDA also increased world ending stocks estimates for the year. Trends are up in this market on the daily charts. The market noted good planting and emergence progress in the weekly USDA reports released on Monday afternoon. Good demand for exports continues.

Overnight News:

Chart Analysis: Trends are up with no objectives of 1748 May. Support is at 1800, 1778, and 1725 May and resistance is at 1850, 1870, and 1907 May.

• CORN AND OATS

General Comments: Corn closed lower and Oats closed higher yesterdAY as traders think that good Spring weather here will greatly increase planted Corn area. The USDA supply and demand reports showed reductions in Corn ending stocks in line with trade expectations but still over 20 billion bushels. Increased demand was noted in all domestic categories, but export demand was left unchanged. South American production estimates were little changed. It is very expensive to plant Corn and Corn is considered unprofitable to plant right now, so planted are might not increase that much if at all. USDA issued its crop progress report for Corn and Corn planting is proceeding slowly. Demand for Corn has been strong at lower prices. Big supplies and reports of limited demand are still around, but futures have been very oversold. Funds remain very large shorts in the market.

Overnight News:

Chart Analysis: Trends in Corn are mixed. Support is at 426, 422, and 408 May, and resistance is at 437, 448, and 459 May. Trends in Oats are mixed. Support is at 344, 339, and 334 May, and resistance is at 369, 362, and 369 May.

• SOYBEANS

General Comments: Soybeans and Soybean Oil closed lower and Soybean Meal closed higher last week in response to the USDA supply and demand estimates that showed a greater increase in US ending stocks than the market had anticipated. South American production estimates were little changed. Brazil producers had been taking advantage on higher futures in the US and higher basis levels in Brazil, but the basis has fallen sharply in Brazil this week and sales have been less. Reports of great export demand in Brazil provide some support. Reports indicate that China has been a very active buyer of Brazil Soybeans this season. Ideas that South American production is taking demand from the US have pressured futures lower. Funds remain large shorts in the market. The US reports strong domestic demand.

Overnight News:

Chart Analysis: Trends in Soybeans are mixed. Support is at 1166, 1152, and 1140 May, and resistance is at 1181, 1193, and 1207 May. Trends in Soybean Meal are mixed to up with no objectives. Support is at 336.00, 330.00, and 325.00 May, and resistance is at 348.00, 352.00, and 35=7.00 May. Trends in Soybean Oil are down with objectives of 4430 May. Support is at 4520, 4420, and 4360 May, with resistance at 4730, 4830, and 4980 May.

• CANOLA AND PALM OIL

General Comments: Palm Oil was lower last week in sympathy with the price action in Chicago and on demand concerns. It wqs lower today on ideas of demand weakness. The export pace is expected to continue to really improve but this is part of the price already, in part due to stronger world petroleum prices that have affected world vegetable oils prices as well. Domestic biofuels demand is likely to improve. Ideas of weaker production ideas against good demand still support the market overall. Trends are turning up on the daily charts. Canola was lower in response to the USDA reports that showed plenty of oilseeds viable in the US and the world and on price action in Chicago.

Overnight News:

Chart Analysis: Trends in Canola are mixed to down with objectives of 617.00 and 596.00 May. Support is at 620.00, 616.00, and 610.00 May, with resistance at 637.00, 645.00, and 652.00 May. Trends in Palm Oil are mixed. Support is at 4110, 4040, and 3920 July, with resistance at 4180, 4220, and 4300 July.

Midwest Weather Forecast

Read Full Story »»»

DiscoverGold

Softs Report: Cotton, OJ, Coffee, Sugar, Cocoa

By: Jack Scoville | April 16, 2024

• COTTON

General Comments: Cotton was a little higher to relieve oversold conditions from weaker demand ideas. The export sales report showed poor dales once again. USDA made no changes to the domestic supply or demand sides of the balance sheets, but did cut world ending stocks slightly. Trends are still down on the daily and weekly charts. Demand has been weaker so far this year. The US economic data has been positive, but the Chinese economic data has not been real positive and demand concerns are still around. However, Chinese consumer demand has held together well, leading some to think that demand for Cotton in world markets will increase over time.

Overnight News: The Delta will get showers and rains and near normal temperatures. The Southeast will see showers and rains and near normal temperatures. Texas will have mostly dry conditions and near normal temperatures.

Chart Trends: Trends in Cotton are down with objectives of 77.20 May. Support is at 81.70, 80.80, and 79.30 May, with resistance of 86.20, 88.20 and 91.40 May.

This Week Last Qeek Last Year Average

Cotton Planted 8 5 7 8

• FCOJ

General Comments: FCOJ closed higher yesterday and remains at the top edge of a trading range. The move came in reaction to the latest USDA reports that showed less production. Florida production is now estimated at 18.8 million boxes, from 19.8 million last month. Reports of tight supplies are around. Florida said that Oranges production will be low, but above a year ago. Futures still appear to have topped out even with no real downtrend showing yet, so a range trade has been seen. Prices had been moving lower on the increased production potential for Florida and the US and in Brazil but is now holding as current supplies remain very tight amid only incremental relief for supplies is forecast for the coming new crop season. There are no weather concerns to speak of for Florida or for Brazil right now. The weather has improved in Brazil with some moderation in temperatures and increased rainfall amid reports of short supplies in Florida and Brazil are around but will start to disappear as the weather improves and the new crop gets harvested.

Overnight News: Florida should get scattered showers or dry conditions. Temperatures will average near normal. Brazil should get scattered showers and above normal temperatures.

Chart Trends: Trends in FCOJ are mixed. Support is at 350.00, 347.00, and 353.00 May, with resistance at 378.00, 389.00, and 391.00 May.

• COFFEE

General Comments: Both markets closed sharply higher yesterday and both show up trends on the daily and weekly charts. The lack of Robusta Coffee in the market continues to support futures. Robusta offers from Vietnam remain difficult to find and the lack of offer of Robusta is a bullish force behind the London market action. There were some indications that Vietnam producers were now offering a little Coffee, but not much and not nearly enough to satisfy demand. Vietnamese producers are reported to have about a quarter of the crop left to sell or less and reports indicate that Brazil producers are reluctant sellers for now after selling a lot earlier in the year. The next Robusta harvest in Brazil is starting now.

Overnight News: The ICO daily average price is now 223.13 ct/lb. Brazil will get mostly scattered showers with near normal temperatures. Central America will get mostly dry conditions. Vietnam will see scattered showers

Chart Trends: Trends in New York are up with no objectives. Support is at 214.00, 210.00, and 208.00 May, and resistance is at 235.00, 238.00 and 241.00 May. Trends in London are up with objectives of 4090 May. Support is at 3840, 3760, and 3700 May, with resistance at 4000, 4030, and 4060 May.

• SUGAR

General Comments: New York and London closed lower again yesterday and trends are down on the charts as the market seems to have supplies available for sale. There are still ideas that the Brazil harvest can be strong for the next few weeks if not longer. Indian production estimates are creeping higher but are still reduced from recent years. There are worries about the Thai and Indian production. Offers from Brazil are still active but other origins. are still not offering in large amounts except for Ukraine. Ukraine offers have suffered lately with the war. Demand reports from Europe have been strong.

Overnight News: Brazil will get rains in the south and scattered showers in the north. Temperatures should average above normal. India will get mostly dry conditions and below normal temperatures.

Chart Trends: Trends in New York are down with objectives of 1950 July. Support is at 2000, 1980, and 1940 July and resistance is at 2050, 2100, and 2150 July. Trends in London are down with objectives of 567.00 August. Support is at 579.00, 574.00, and 568.00 August, with resistance at 600.00, 608.00, and 617.00 August.

• COCOA

General Comments: New York and London were higher yesterday and trends are up. Production concerns in West Africa as well as demand from nontraditional sources along with traditional buyers keep supporting futures. Production in West Africa could be reduced this year due to the extreme weather which included Harmattan conditions. The availability of Cocoa from West Africa remains very restricted and projections for another production deficit against demand for the coming year are increasing. Ideas of tig8ht supplies remain based on more reports of reduced arrivals in Ivory Coast and Ghana continue. Ivory Coast arrivals are now 1,301 tons, down 26.7% from the previous year. Mid crop harvest is now underway and here are hopes for additional supplies for the market from the second harvest. Demand continues to be strong, especially from nontraditional buyers of Cocoa.

Overnight News: Isolated showers are forecast for West Africa. Temperatures will be near normal. Malaysia and Indonesia should see scattered showers. Temperatures should average near normal. Brazil will get isolated showers and above normal temperatures.

Chart Trends: Trends in New York are up with objectives of 11890 May. Support is at 10380, 10000, and 9630 May, with resistance at 11200, 11320, and 11440 May. Trends in London are mixed to up with no objectives. Support is at 8570, 8080, and 7930 May, with resistance at 9320, 9440, and 9560 May.

Read Full Story »»»

DiscoverGold

Inflation Nation Everywhere. The Corn & Ethanol Report

By: Daniel Flynn | April 16, 2024

We start off the day with Building Permits Prel, Building Permits MoM Prel, Housing Starts, and Housing Starts MoM at 7:30 A.M., Redbook YoY at 7:55 A.M., Industrial Production MoM & YoY, Capacity Utilization, and Manufacturing Production MoM & YoY at 8:15 A.M., 42-Day Bill Auction and 52-Week Bill Auction at 10:30 A.M., and API Energy Stocks at 3:30 P.M.

With inflation rocketing out of control and being on the brink of war physical gold and gold futures have repeatedly set new record highs, starting in early March, as buyers seek a home for cash to avoid lost purchasing power in US dollars. Last week, nearby gold futures reached a record high of $2,429/oz. The latest Commitment of Traders report showed that the week ending Apr 9th, funds bought 929 contracts of gold futures and held the largest net long position since July 2020. This is compared to commercial buying of 1,226 contracts, which resulted in a &82.50 price change for the week. The rally in gold prices appears to be much about limited commercial selling. In fact, commercials have been net buyers for the last month. With the US now adding $ 1 trillion in debt every 100 days in this out of sight-out of mind economy. Inflation rates are expected to rise in the coming months further robbing the US dollar for purchasing power. As such, Chinese demand for gold stays strong. In the overnight grain futures started out firmer but sold off due to strengthening US dollar. China’s economy grew at a better than expected 5.3% in the 1st quarter of 2024 on a 14% gain on exports year-over-year. However, Chinese retail sales grew by just 3.1%, which was lower than expectations of 4.6%. The Chinese GP growth helped bump grain/oilseed futures initially higher, but the strengthening dollar acted to tug commodities to weaker morning levels. Geopolitical fears are now also in the mix with runaway inflation and the usual suspects with seedings started and we will watch South American weather and monitor any movement of Ukraine product into the next phase of the US growing season.

Read Full Story »»»

DiscoverGold

Buying Rumors. The Energy Report

By: Phil Flynn | April 16, 2024

Global oil prices went through the ‘buy the rumor sell the fact’ on the Iranian attack on Israel and now are still waiting to see what Israel’s response will be. Reports by the Israeli Defense Minister Yoav Gallant said that Israel would have no choice but to retaliate and reports that the ground invasion in Rafah southern Gaza will be put off until the Iranian response happens. This raises more questions than answers. Iran’s attack on Israel seems to have given Israel surges in international support even by Arab nations that are tired of Iran’s goal to disrupt peace in the region.

Iran is the driving the force between Hezbollah, Hamas and the Houthi rebels that have basically destabilized the region and caused war and turmoil for almost every country in the world. It also clear that the failure to enforce sanctions on Iran has allowed Iran to raise oil output to a 5 and a half year high and the billions of dollars they are reaping for this has gone to fund terror and bloodshed. Now after the attack, many countries are urging Israeli restraint on its response to Iran but secretly behind the scenes, they would love nothing better than to see the Iranian regime fall because of all the havoc that they’ve been causing. Oil prices have sold off because of the expectation that Israel will be measured in the response and is putting pressure on prices, but it may not be long before we start buying the rumor of an attack once again.

Zero Hedge reports that new statements from the Pentagon issued Monday have said the Houthis fired over 90 ballistic missiles and drones – most of which were intercepted by US and allied forces over the past 48 hours, once the Iranian attack kicked off in the overnight hours of Saturday. US Central Command described that at one point during the attack the Houthis fired an anti-ship ballistic missile directly against US Navy and commercial ships in the Gulf of Aden. “There were no injuries or damage reported by US, coalition, or commercial ships,” CENTCOM said.

Oil prices seem to be getting mixed emotions from Chinese economic data. The gross domestic product seems to be better than expected but the report on consumer demand seemed to be disappointing especially because of past reports that over the Chinese holiday domestic demand was at pre COVID levels.

Domestic oil production also increased but make no mistake about it, they’re still going to need a lot of oil from other places. The Wall Street Journal wrote, “With familiar signs of weakness in consumption and real estate in the first three months of the year, many economists say Beijing still isn’t doing enough to support Chinese households and nurture a more balanced recovery. And the loss of some momentum in March compared with the preceding two months reinforced expectations that further stimulus will be needed to ensure that the government meets its growth target of around 5% for the year. China said its economy grew 5.3% in the first quarter compared with the same three months a year earlier, a faster pace than the 5.2% year-over-year growth rate that the country notched in the final quarter of 2023, China’s National Bureau of Statistics said Tuesday. The pickup was propelled by a rise in industrial production and swelling investment in factories. After a challenging few year, Chinese officials are steering activity and investment toward manufacturing and exports to compensate for domestic consumers’ reluctance to spend and a continuing crunch in the property market.”

It is very powerful that yesterday sell off oil price low set the low for the week. We expect modest drawdowns in crude oil and products and today’s American Petroleum Institute report and we expect to see an uptick in demand after the drop in demand that we saw over the Easter holiday weekend. I expect that the exports for oil and gasoline will rebound, and we should see an uptick in gasoline demand as well and with the ongoing risk to supplies, it’s unlikely that the market is at a point where it will collapse.

Reuter reports that – Russia has been able to swiftly repair some of key oil refineries hit by Ukrainian drones, reducing capacity idled by the attacks to about 10% from almost 14% at the end of March, Reuters calculations showed. Ukraine stepped up drone attacks on Russian energy infrastructure since the start of the year, hitting some major oil refineries across the world’s second largest oil exporter in attacks that sent up oil prices.

Natural gas cash prices are falling once again and even with the drop in US natural gas, rigs production may not be falling quite fast enough. Yahoo finance writes, “the bearish sentiment surrounding the commodity even prompted shale producers Chesapeake Energy CHK and EQT Corporation EQT to hit the brakes on new drilling. Chesapeake announced a reduction in its drilling rigs so as to lower volume. The company has decided to cut this year’s gas production expectations by around 20%. Chesapeake’s plans rippled through the market, with Appalachian Basin-focused EQT following on. The explorer and producer of natural gas said that it will lower its daily output by 1 Bcf to combat the supply glut in the U.S. market. According to EQT, the revised plan will likely reduce net production by 30-40 Bcf. While these production cut announcements temporarily drove natural gas prices higher, they have failed to galvanize the market.”

Read Full Story »»»

DiscoverGold

Commodities Daily Market Movers (% Price Change)

By: Marty Armstrong | April 16, 2024

• Top Movers

AU - Victoria Base-Load Electricity Futures 6.52 %

Rough Rice Futures (CBOT) 6.38 %

London Aluminum Spot 4.91 %

Coffee (NYCSCE) Futures 2.9 %

NY Copper Futures 2.83 %

• Bottom Movers

NY Natural Gas Futures 4.46 %

Palm Kernel Oil 3.05 %

London IPE Gas Oil Futures 3.01 %

Gold LBM per Oz (USD) 2.77 %

Zinc (99.995%) Spot 2.77 %

*Close from the last completed Daily

DiscoverGold

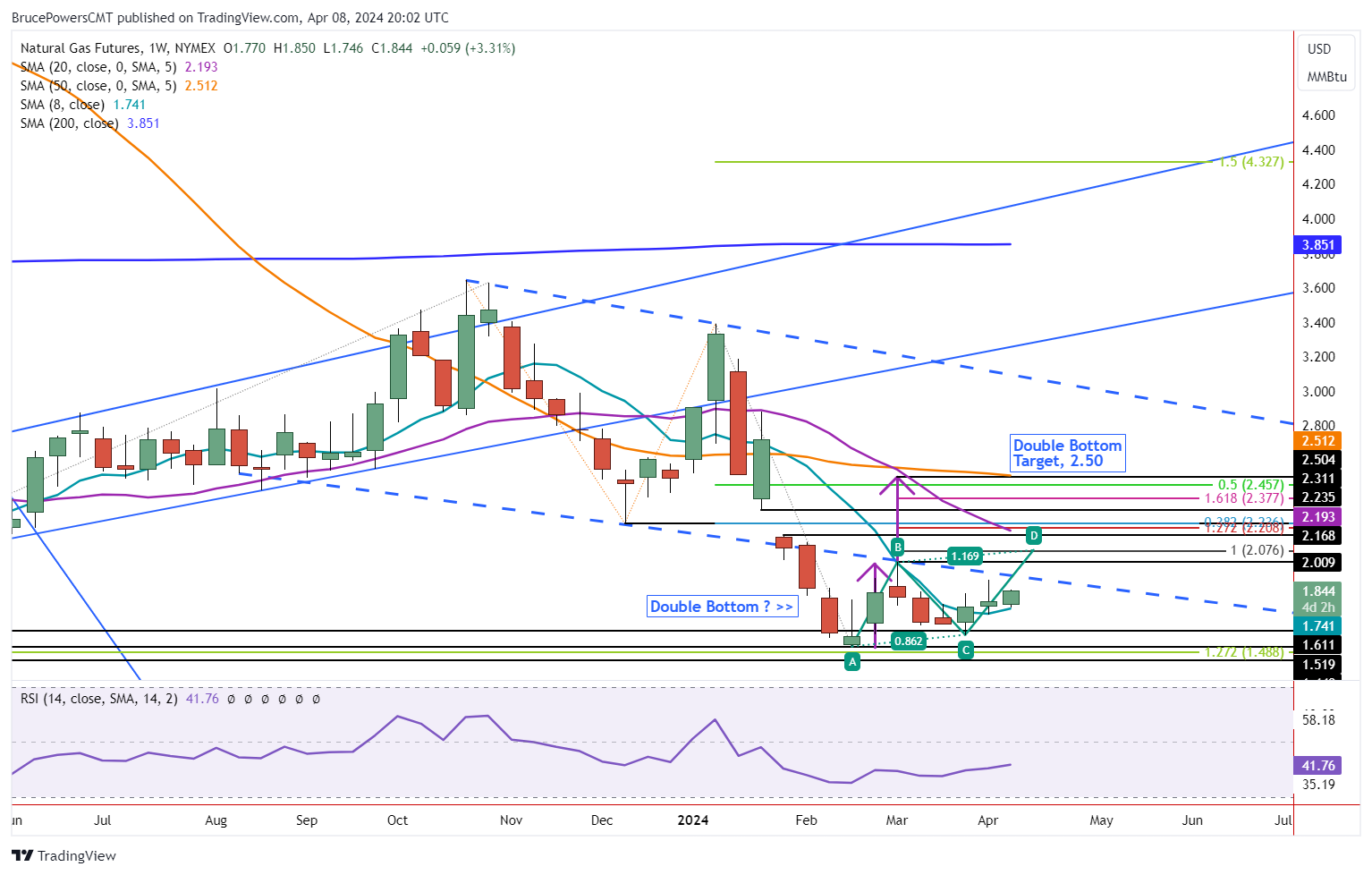

Natural Gas Testing Support Amidst Low Volatility

By: Bruce Powers | April 12, 2024

• Natural gas is testing support around the downtrend line and 20-Day MA. Signs of strength are crucial if the rally off trend lows has a chance to continue.

Natural gas dipped briefly below the minor 1.75 swing low from Monday before finding support at 1.73 and stalling the descent. Volatility diminished as it is on track to complete a narrow range day while further testing support around the long-term downtrend line and 20-Day MA, now at 1.76. If natural gas can advance above today’s high of 1.785 heading into next it has a chance to progress the near-term uptrend that starts from the higher swing low and potential second bottom (C).

Drop Below Today’s Low Points to Lower Triangle Line

However, a drop below today’s low without a quick recovery increases the chance that natural gas will further trace out a developing symmetrical triangle (purple). A drop below today’s low increases the chance of a test of support at the lower boundary line of the triangle. Recent minor signs of strength seen recently as natural gas recaptured both the 20-Day and 50-Day MAs would then be negated.

Rally Above 1.785 Would Be First Sign of Strengthening

Nevertheless, if natural gas can continue to find support around the downtrend line and 20-Day MA, followed by signs of strength, it will likely have completed a minor pullback. The chance for an eventual bull trend continuation will then become more likely. A rally above today’s high of 1.785 will provide an initial signal, but upside follow through will be key as to whether it can keep rising from there.

Weekly Chart Analysis

On a weekly basis, natural gas is on track to close weak, in the lower third of the week’s range and possibly with a doji. The weekly candle will be bearish unless natural gas can rise before today’s close. Last week also ended relatively weak. This week will be the second in a row where natural gas is closing in the lower area of the week’s range. In both cases support for the week was seen in the 8-Week MA.

Natural gas has been mostly below the 8-Week line since early-January. So, a successful test of support at the 8-Week line is one sign of strength. Regardless, the weekly performance did not confirm strength since this week and last week ended (likely) in the lower part of the range. Therefore, a drop below today’s low would also give a weekly bearish signal relative to this week’s low and the 8-Week MA.

Read Full Story »»»

DiscoverGold

Commodities Daily Market Movers (% Price Change)

By: Marty Armstrong | April 12, 2024

• Top Movers

AU - Victoria Base-Load Electricity Futures 4.05 %

Oats (CBOT) Futures 2.96 %

Oats (Minneapolis) 2.38 %

Coffee (NYCSCE) Futures 2.21 %

Zinc (99.995%) Spot 1.88 %

• Bottom Movers

NY Natural Gas Futures 6.42 %

Cheese 3.82 %

Soybean Oil CBT Futures 3.32 %

London Nickel Spot 3.03 %

Sugar World (CSCE) Futures 2.84 %

*Close from the last completed Daily

DiscoverGold

Natural Gas Testing Support Amidst Consolidation

By: Bruce Powers | April 11, 2024

• Natural gas prices test support at 20-day MA, poised for bullish reversal or failure to lower prices.

Natural gas retreats further from Wednesday’s 1.94 high on Thursday as it tests support around the 20-day MA with the day’s low of 1.77. The 20-Day line is at 1.76 and it is strengthened by the long-term downtrend line, which marks the same price area. Notice that the 20-Day line and trendline have joined together. This should lead to a rejection of price to the upside, but there are no signs of it yet.

Moving Averages Show Improving Strength

Natural gas rallied back above the 20-Day line on April 1, and there was one subsequent successful test of support at the 20-Day MA. Today provides the second such test. A bounce and bullish reversal off the 1.76 price zone should complete the test and clear the way for natural gas to continue to advance. Over the past week the 8-Day MA has risen back above both the 20-Day and 50-Day MAs. And there was recently a higher swing low (C), reflecting improving demand.

Further Consolidation Possible Until Clear Breakout

Nevertheless, there is also a possibility that natural gas traces out a consolidation pattern. A bearish pennant or symmetrical triangle is the form now taking shape. It remains valid until there is an upside breakout above Wednesday’s high of 1.87. A drop below Monday’s low of 1.75 will increase the likelihood that consolidation may continue.

Rise Above 1.89 Shows Strength

Near-term resistance is now at today’s high of 1.89. A breakout above that high will provide the next sign of strength that could lead to a breakout above Wednesday’s high of 1.94. Once there is a daily close above that level natural gas should be ready to progress higher. The neckline for a potential double bottom bullish pattern is at 2.01 (B), with the first higher target zone around 2.06 to 2.08. Other target areas of interest are marked on the chart.

Weekly Chart, Bullish Signs

The weekly chart (not shown) is not a screaming buy, but it does show bullish progression. Last week’s close was relatively weak as it was in the lower half of the week’s trading range. Further, this week’s performance is also at risk of closing in the lower half of the week’s range. At the same time, this week’s low and last week’s both found support around the 8-Week MA, now at 1.73.

Read Full Story »»»

DiscoverGold

Coffee Hits All-Time High

By: Barchart | April 11, 2024

• Coffee Hits All-Time High.

Read Full Story »»»

DiscoverGold

The Corn & Ethanol Report

By: Daniel Flynn | April 11, 2024

We kickoff the day with Export Sales, PPI MoM & YoY, Core PPI MoM & YoY, PPI, Initial Jobless Claims, Continuing Jobless Claims, Jobless Claims 4-Week Average, PPI Ex Food, Energy, and Trade, and PPI Ex Food, Energy, and Trade MoM & YoY at 7:30 A.M., Fed Williams Speech at 745 A.M., EIA Natural Gas Storage at 9:30 A.M., 4-Week & 8-Week Bill Auction at 10:30 A.M., Crop Production, USDA Supply/Demand, WASDE, Fed Collins Speech, and 15 & 30-Year Mortgage Rate at 11:00 A.M., 30-Year Bond Auction at 12:00 P.M., and Fed Bostic Speech at 12:30 P.M.

With Crop production, USDA Supply/Demand WASDE and CONAB data match up the PPI and Jobless Claims should steel the show. After the morning inflation numbers as we digest the numbers we will see if those numbers put a wrinkle in the April grain reports. There are reports of the FED sounding more hawkish as inflation is taking its toll with the working class and there will be consequences at the ballot box, especially if there is no end in sight. Pre-report long term fundamentals, featuring Ukrainian corn priced to sell. US competitive with South America through summer. Ukraine’s war, freight and insurance cost challenges have kept fob premiums there deflated, which has allowed the Ukraine to capture market share in E Asia. Including China. Otherwise, unlike recent years, US Gulf corn at $490/Bu is not expensive in the world marketplace. Export Sales stay elevated relative to last year into June & July. Spot Argentine fob basis has rallied to $.70 over May CBOT. Brazilian corn isn’t quoted prior to July. US corn for delivery is offer $.12/Bu below Brazilian and at parity with Argen tin when all fobbing costs are added. This is much different than summer 2022 and 2023, when US corn was the high cost origin – due to tight stocks. A year ago April forward Brazilian offers were a full $.90-100/Bu below US Gulf origin! An outright collapse in US export demand is unlikely. Add disease pressures on Argentine corn is knifing production. Traders are waiting and will focus on South American crop sizes and the disparity between CONAB & WASDE data. Most expect a bearish US and world balance sheet. The Brazilian number holds the key, while Argentine disease concerns may lurk in their expected overall good to excellent growing year.

Read Full Story »»»

DiscoverGold

Commodity price changes over last yr

By: Charlie Bilello | April 11, 2024

• Commodity price changes over last yr

Cocoa: +245%

Gold: +17%

Coffee: +16%

Silver: +13%

WTI Crude: +8%

Copper: +8%

Brent Crude: +7%

Aluminum: +6%

US CPI: +3.5%

Cotton: +3%

Heating Oil: +1%

Zinc: -2%

Gasoline: -2%

Sugar: -9%

Natural Gas: -13%

Wheat: -18%

Soybeans: -22%

Corn: -34%

Read Full Story »»»

DiscoverGold

Weighty Decisions. The Energy Report

By: Phil Flynn | April 11, 2024

Global oil markets must decide whether they are more worried about inflation or global conflict. Oil prices fluctuated on the prospect of a widening war with new potential battlefronts in the Middle East, the ongoing war between Russia and Ukraine and surging inflation that could delay or indefinitely postpone interest rate cuts. monitoring amid ongoing uncertainties to ensure a sound and sustainable oil market balance they also are keeping their demand growth forecast for 2024 at a very impressive 2.25 million barrels a day, The stakes are getting higher every day with lives, and sacred fortunes on the line.

The Consumer Price Index was a blow to those sacred fortunes and those trying to live paycheck to paycheck or those migrant debit cards. The consumer-price index, a measure of goods and services prices across the economy, rose 3.5% in March from a year earlier, the Labor Department said Wednesday. That was a touch higher than economists had forecasted and a pickup from February’s 3.2%. The so-called core prices, which exclude volatile food and energy categories, also rose more than expected on a monthly and annual basis according to the Wall Street Journal.

That hot inflation report took the odds of a June rate cut from better than 50% down to the low 20s. The reason for this hot inflation number is very simply corporate greed. How do I know that? Very Simply, Joe Biden said so. Biden urged, “corporations including grocery retailers to use record profits to reduce prices.” As corporations should know that they should be beholden to the Biden administration and not their shareholders. That is why he wants to tax them more so he can use that money to win favor with a student who can’t or refuse to pay back their loans or others that he thinks might vote democrat. So, don’t you listen to all the economists who try to tell you that inflation is caused by the government printing too much money or running up massive historic debt levels because Biden knows better? It seems that based on when Biden got elected it brought in a new era of greed! When President Trump was in office, corporations were not greedy because inflation was at historically low levels.

Of course, you can whine about not having enough money to buy groceries or fill your gas tank or weighty decisions about what you have to put back on the shelf that was in your grocery cart but that is because you don’t understand how good you have it under Biden. Remember he called out those companies that makes your potato chip bag smaller. Maybe that’ll make your waistline shrink a little too! So, to think you’re not better off just because your monthly bills are well above your wage increases, it is just because you have been psychologically damaged. Most likely due to climate change fears. And we all know that was President Donald Trump’s fault.

Even after the hot inflation number, oil tried to hold its ground even with an Energy Information Administration (EIA) report that was bearish on the surface. Yet thoughts about inflation or the volatility of the Weekly EIA were put aside on reports that an attack on Israel by Iranian proxies was imminent according to the United States. Reuters wrote that, “Oil prices settled up $1 on Wednesday after three sons of a Hamas leader were killed in an Israeli airstrike in the Gaza Strip, feeding worries that ceasefire talks might stall.”

The market had other concerns as to whether or not the United States would back Israel in a confrontation with Iran. Some people are suggesting that the Biden administration is emboldening Iran because there is this perception that the United States will not stand with Israel if Iran attacks. The flip side of that is the Biden administration seems to be walking a fine line between saying that they will defend Israel but at the same time trying to appease their base suggesting that they might not if they don’t approve a ceasefire in the Gaza Strip.

Israeli Prime Minister Netanyahu is saying that, “we are preparing for scenarios and challenges from other fields in other words getting ready to fight a war on many fronts. This comes as the Iranian Revolutionary Guard is bragging that they could shut down the Strait of Hormuz, the world’s most important oil chokepoint. This comes as Iranian-backed Houthi rebels are already causing havoc in the Red Sea transit routes. The attempt to shut these oil flows down could lead to an incredible price spike.

While the global oil price spreads are pricing in a very undersupplied market, the EIA is giving us a little reprieve in a weekly report that may be exaggerated due to the Easter Holiday. The EIA reported that oil supplies increased by a surprising 6.4 million barrels as U.S. oil exports plummeted to 2,708 million barrels a day from 4,022 million barrels a day in the holiday-shortened week. Week-over-week drops and demand was likely impacted by the holiday. Total Petroleum demand fell from 9,236 million barrels a day to 21,292 million barrels a day a drop of 2,056 Million barrels a day

Now overnight oil prices are pulling back as well as products as the imminent talk of a threat of an attack haven’t happened just yet. Traders may also be booking profits ahead of the producer price index which if it comes in hotter like the CPI did, it could cause the dollar to rally and put downward pressure on prices. I guess we have to wait to see how greedy corporate America is gonna be this week.

Today we get the natural gas inventories we’re looking for a small injection in the supply of about 11 to 14 BCF. The market does look like it’s trying to bottom here and it still is facing some incredible headwinds but production is starting to taper off.

Read Full Story »»»

DiscoverGold

Natural Gas Hits New Trend High and Pulls Back

By: Bruce Powers | April 10, 2024

• Natural gas triggered a new trend high today but could got turned around after encountering resistance at 1.94.

Natural gas continued its advance on Wednesday with a new minor trend high of 1.94. Although Tuesday’s closing price relative to the day’s range was not particularly strong, it did manage to close at its highest daily closing price in 23 trading days. Today’s advance was hit with selling pressure once the 1.94 high was reached. At the time of this writing natural gas is trading near the lows of the day and set to close relatively weak, in the lower quarter of the day’s range.

New Bullish Indications

Nonetheless, there are recent bullish indications showing underlying strength in the price of natural gas. The blue 8-Day MA has crossed up above the orange 50-Day and prior peak of the current short-term uptrend was exceeded yesterday. In addition, natural gas is holding above the 50-Day MA and above the long-term downtrend line. Support around the 50-Day line, currently at 1.80, should maintain support during weakness for recent bullish indications to remain valid.

Support Levels

The downtrend line can be priced currently because it has converged with the purple 20-Day moving average, now at 1.76. That is a more critical price area where support should be seen for the near-term bullish outlook to be retained. Given the potential for a weak close today, there is a possibility a pullback towards support may have already begone. However, it seems likely that it should be short lived if the growing bullish sentiment is to remain in charge.

Buyers Back in Charge Above 1.94

Further strength is signaled on a breakout above today’s high of 1.94. There is an initial target zone highlighted on the chart from 2.06 to 2.08. That price zone marks the completion of two rising ABCD patterns. The larger pattern is shown in green and labeled, while the smaller pattern is not labeled and starts from the most recent swing low at (C). Having such a fractal relationship between the two pieces of the developing uptrend should increase the chance for the targets to be reached. Also, a breakout above that price zone should also be met with enthusiasm from buyers.

Read Full Story »»»

DiscoverGold

Some commodity indices are up over 15% from their Q4 lows, too, suggesting that the inflation story is far from over.

By: Markets & Mayhem | April 10, 2024

• Some commodity indices are up over 15% from their Q4 lows, too, suggesting that the inflation story is far from over.

Read Full Story »»»

DiscoverGold

Agriculture Master Report

By: Bill Moore | April 10, 2024

JULY CORN

As is evident from the above chart, May Corn has been confined to a 30 cent range (420-450) since Mar 1! The friendly news such as the 3-28-24 Stocks/Seeding Report with an acres estimate 4.6 million acres less than 2023 & positive weekly export inspections & sales push the mkt up towards the top end & negative news such as planting pressure & rains for the dry areas pressure the mkt down to the 420 support! This week is another with sparse fresh news – as the mkt anticipates the onset of active planting after mid-April & the USDA April WASDE REPORT due out at 11am on Thur 4-11-24! Until then, the mkt will continue to chop around as traders “even up” in front of the report!

JULY BEANS

July Beans – much like its sister mkt July Corn – is range-bound (1185-1230) amid lackluster trade – as the mkt awaits updates from the USDA & CONAD on Thursday morning! Planting weather has been benign but some areas have been subject to flooding! Most producers seed corn first – with the wheels expected to roll in the 2nd half of April! Export interest has been meager but has been offset by strong domestic biodiesel demand! The fund short position is still sizeable – & the mkt is nearly $3.00 off its 2023 highs – so there is little margin for error for the US crops this Summer & Fall! South American production continues to ratchet down!

JULY WHT

July Wht has been slowly grinding higher since early Mar – occasionally buoyed by geopolitical issues from the escalating Russian-Ukraine War & dryness in the US Southwest plains! However, sluggish exports running 11% under 2023 & a 56% Gd-Ex crop rating has kept the wraps on recent rallies! Spring Wht planting is 3% in! Just like corn & beans, wht anxiously awaits the USDA’s April WASDE on Thur at 11am!

JUNE CAT

June Cattle topped out in late March – breaking $14 (186-172) due to a convergence of negatives including higher weights & slaughters, demand drying up in response to elevated prices, a bearish March Cattle-on-Feed Report – reflecting 10% more placements & finally the occurrence of Bird Flu in some dairy cattle prompting demand fears! As often happens, the break was overdone – especially as the Bird Flu news waned & the mkt recovered $5 of the plummet! The onset of the “grilling season” – the meats best demand period – will help stabilize June Cattle & cause them to consolidate well off their recent lows!

JUNE HOGS

June Hogs unabashedly took over the “upside leadership role” in the meats by staging a remarkable, meteoric $9 rally (100-109) since Mar 1 – including 7 consecutive higher closes! The move was spawned by several positives – a bullishly construed Pig Crop Report on Mar 28 where Farrowing Intentions implied lower supplies, a bird flu epidemic which transferred some demand from suspect beef to much cheaper pork & finally the advent of the best demand season of the year – when everyone pulls out their grills! However, the mkt has rallied into “overbought territory” -accumulating a big premium to cash – & is due for a correction soon!

Read Full Story »»»

DiscoverGold

War Torn Super Cycle. The Energy Report

By: Phil Flynn | April 10, 2024

The Commodity Supercycle that seemed dormant late last year has awakened, incredibly. While many thought that the cycle had passed, it is clear now that price respite was just the eye of the commodity prices super cycle hurricane. The historic record-breaking price surge that we have seen in cocoa may be a preview of what we may see in other commodities where it appears demand will outstrip supply. Commodities like copper, silver, platinum, palladium, and of course the world’s black gold, oil that Texas tea, are headed for supply squeezes unlike anything we have seen since the 1970s and it did not happen overnight. It happened while the world was sleeping.

Underinvestment in fossil fuels as well as a hostile regulatory environment, means global oil supplies are going to be short. Even the Energy Information Administration in their recent short-term energy outlook not only had to raise the oil prices but also had to adjust their downward projections of future demand in an attempt to perhaps justify their previous massive adjustments to their numbers. In other words, the EIA had to raise their demand forecasts before they could lower it. The EIA raised their forecast of WTI crude prices to average $83.78/ barrel(bbl) in 2024, versus an earlier forecast of $82.15/bbl. The EIA also raised its Brent Crude prices to an average of $86.98/bbl in 2025, versus an earlier forecast of $84.80/bbl. Yet it was demand where they had to raise the river instead of lowering the bridge to make their forecast jive.

Or as the EIA put it, “This month we revised the 2022 global liquid fuels consumption data available in our International Energy Statistics, increasing our assessment of global oil consumption that year by nearly 0.8 million barrels per day (b/d) compared to last month’s STEO. The historical data serves as a baseline for our short-term forecasts, affecting our view of energy markets this year and next. This month’s revision to historic data, as well as current market dynamics, led us to increase our forecasts for global oil consumption.” Yet if you want to be confused, then they go on to say that after the adjustment the EIA cuts forecast for 2024 world oil demand growth by 480,000 bpd, now sees 0.95 mln bpd year-on-year increase. And cuts forecast for 2025 world oil demand growth by 30,000 bpd, now sees 1.35 mln bpd year on year increase.” Are they trying to hide their meaning here?

What they won’t be able to hide is rising gasoline prices. The EIA raised its forecast for retail gasoline prices in 2024 to $3.59 a gallon, versus an earlier forecast of $3.48 a gallon.

Yesterday the market was reluctant to move higher as it tried to digest headlines surrounding geopolitical risk that could have major implications for the price of oil and the potential movement for oil. Last week oil put in a lot of risk premium on the expectations that Iran would respond directly against Israel after the attack on its compound in Lebanon. Yesterday there was an unconfirmed report that an Iranian envoy was en route to the United States for some talks to avoid a conflict and made the rounds even though the story wasn’t confirmed.

Another headline that took out some more premium was the report that the US Defense Secretary heard from Israel that there is no set date for its invasion of Rafah, raising hopes that there could be some hope for a ceasefire even if a ceasefire talks broke down. That was after Prime Minister Benjamin Netanyahu said Monday that he has set a date for the IDF to launch its much-anticipated offensive in the southern Gaza city of Rafah. All of this is happening and swaying the market.

Now the American Petroleum Institute (API)report seemed to suggest that supplies from the seasonal viewpoint are very tight but based on weekly numbers are less than inspiring to the bullish side of the market.

The API reported the crude supplies increased by 3.034 million barrels which was more than the market had anticipated but from a seasonal viewpoint smaller than most builds at this time of year. Gasoline inventories fell by 609,000 barrels and distillates rose by 120,000 barrels which wasn’t that inspiring to either the bulls or the bear. The products have been under pressure. This week’s report, if confirmed today by the Energy Information Administration report, could give us the bottom for the products.

Yet what may be important to the oil and product traders today will be the consumer price index. The market fixation on whether or not the Federal Reserve is going to have the ability to cut interest rates as inflation continues to be strong is the question on most traders minds. The key thing here is that even if the Federal Reserve has to backtrack on a rate cutting, the reality is it won’t impact oil demand quickly enough to save the market from a supply squeeze.

What we expect is that oil will react to a hot or cold report in the long run. It’ll be the supply deficit that will keep support under this market. Remember all that talk about peak oil supply and then the switch over to peak oil demand? Well apparently in the big picture neither one of those predictions is correct. There is a new report by Enverus Intelligence Research that expects global oil demand will grow by 108 million barrels a day by 2030 and will not see peak demand at the end of the decade. The quiet little secret known by many people in the oil industry is simply this: the predictions of peak oil demand were greatly exaggerated.

Speaking about being greatly exaggerated, did you know that Treasury Secretary Janet Yellen is trying to tell people that she believes that the Russian price caps worked? I’m not kidding you. My good friend and noted oil analyst Anas Alhajji said, “Yellen’s price caps on Russian oil are a joke and have no impact. Attacks on Russian refineries meant more crude to export. Here is what Argus wrote today: “Russian crude production rose by 30,000 b/d to 9.44mn b/d, just 10,000 b/d shy of its target. Drone attacks have damaged over 800,000 b/d of Russian refining capacity in recent months, freeing up more crude for export — shipments hit an 11-month high in March.” Take that, Vladimir. Now let’s talk about those so-called sanctions on Iran that have given them billions of dollars. Never mind…I am running out of time.

Let’s move on to natural gas quickly. Reports that Freeport is going to get back online a month earlier than expected and more capacity coming online for LNG exports is giving us a ray of hope that maybe the bottom is in for natural gas. What’s interesting to note is the Energy Information Administration pointed out that for the first time in history, the cost of natural gas is lower than coal. This should be incredible news for people who are concerned about greenhouse gas emissions. The United States is the biggest producer of natural gas and we can change the world by providing cheap natural gas to replace coal plants thereby reducing greenhouse gas emissions. Incredibly this comes even as the Biden administration plays politics with projects surrounding LNG exports.

In yesterday’s Short-Term Energy Outlook, the EIA reported that, “The U.S. winter natural gas withdrawal season ended with 39% more natural gas in storage compared with the five-year average. From April through October this year, EIA forecast less natural gas will be injected into storage than is typical, largely because we expect the United States will produce less natural gas on average in 2Q24 and 3Q24 compared with 1Q24. Despite lower production, EIA still expects the United States will have the most natural gas in storage on record when the winter withdrawal season begins in November. As a result of high inventories, we expect the Henry Hub spot price to average less than $2.00 per million British thermal units (MMBtu) in 2Q24 before increasing slightly in 3Q24. EIA forecast for all of 2024 averages about $2.20/MMBtu.

Read Full Story »»»

DiscoverGold

The Corn & Ethanol Report

By: Daniel Flynn | April 10, 2024