News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

lmcat

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Death spirals occur when a company has zero assets with no future source of revenue, which is not the case with SIRG. The building and equipment on their claim are worth over $2,000,000 and their proven ore reserves are worth over $175,000,000.

These buildings are known as assets!

SIRG owns 80% of the Chloride Copper Mine.

The independent (April 2012) Rizzo Report increased the reserves and they are higher than previously estimated. The existing ore below the current bench levels from 3695 to 3420 values known between 3420 and 3310 could add another 13 Mlbs. Many holes were

abandoned with higher than cut-off grade Cu values in and around the existing pit. Their continuation at depth could prove additional resources. Based on the forgoing, it is safe to assume that the current known resources would provide a minimum of 50 Mlbs of ore; at 5Mlbs/annum, that would support a 10 year mine life.

The Company entered into a Convertible Promissory Note with Asher Enterprises Inc. on June 8, 2011 in the amount of $32,500. The note has an interest rate of 8% with the maturity date of March 13, 2012. During the course of the year ended December 31, 2011 Asher Enterprises converted $10,000 in principle balance of the note to the Company’s common stock in accordance to the terms of the Agreement. This obligation has been satisfied as of June 30, 2012.

The Company entered into a Convertible Promissory Note with Asher Enterprises Inc. on July 1, 2011 in the amount of $25,000. The note has an interest rate of 8% with the maturity date of April 5, 2012. This obligation has been satisfied as of June 30, 2012.

The Company entered into a Convertible Promissory Note with Asher Enterprises Inc. on August 30, 2011 in the amount of $37,500. The note has an interest rate of 8% with the maturity date of June 4, 2012. This obligation has been satisfied as of June 30, 2012.

http://www.otcmarkets.com/edgar/GetFilingHtml?FilingID=8854988 P.17

US Labor Dept drops bomb on gold traders, dents QE3

Frik Els | October 5, 2012

The price of December gold fell by as much as $17 an ounce to touch $1,775 on Friday after data showed a surprise drop in the US employment rate to under 8%.

The metal recovered somewhat during the day, but was still trading down $13.50 or 0.75% at $1,783 by the close after again failing to breach the psychologically important $1,800 level.

The better-than-expected non-farm payrolls number was good news for the dollar and diminishes gold's allure as an inflation hedge and storer of wealth amid currency depreciation.

Gold closed out the September quarter with its biggest quarterly gain since 2010 as QE3 Infinity – as the open-ended third round of quantitative easing in the US has been dubbed – weakens the dollar.

The jobs report may mean that the Federal Reserve will end its QE program to keep interest rates low and flood markets with cheap money sooner rather than later.

MarketWatch quotes a research note by Nomura Securities that says that "every one-tenth percentage point drop in the unemployment rate would shorten the Fed’s buying by about one month," and Friday’s data "implies a three to four month reduction in QE3-related buying".

QE has been a massive boon for gold.

The Fed's near-zero interest rate policy and bond purchases under QE1 kicked off on 16 December 2008. On 15 December 2008 an ounce of gold cost $837.50.

That's a more than 111% improvement for the precious metal on the back of QE1 and QE2 which followed in August 2010.

Another of the Fed's programs to keep interest rates low, Operation Twist, which started in September 2011 has also boosted the price of gold.

The gold price has taken a few hard knocks from 2011's record levels and the spikes downward have all been thanks to actions or pronouncements by chairman Ben Bernanke and the Fed.

At the same time volatility in the gold price has increased dramatically.

At the start of April for instance gold dropped some $60 an ounce in a single session when Fed minutes appeared to indicate QE3 was off the table and its policy of zero interest rates may be coming to an end sooner than previously thought.

The same thing happened on June 7 when gold dropped $50 to under $1,600 an ounce in a couple of hours after Bernanke delivered "anti-climactic" testimony to the US Congress.

That was not the first time traders got cold feet after breaking an important psychological level.

A similar pattern was followed in the days after the metal reached a record high above $1,900 an ounce in August 2011. The yellow metal slid for two days after hitting the record, losing $105 or 5.6% in value in a single day.

http://www.mining.com/us-labor-dept-drops-bomb-on-gold-traders-75566/?utm_source=digest-en-mining-121005&utm_medium=email&utm_campaign=digest

I wonder how this will affect gold mining companies like WSRA.

US Labor Dept drops bomb on gold traders, dents QE3

Frik Els | October 5, 2012

The price of December gold fell by as much as $17 an ounce to touch $1,775 on Friday after data showed a surprise drop in the US employment rate to under 8%.

The metal recovered somewhat during the day, but was still trading down $13.50 or 0.75% at $1,783 by the close after again failing to breach the psychologically important $1,800 level.

The better-than-expected non-farm payrolls number was good news for the dollar and diminishes gold's allure as an inflation hedge and storer of wealth amid currency depreciation.

Gold closed out the September quarter with its biggest quarterly gain since 2010 as QE3 Infinity – as the open-ended third round of quantitative easing in the US has been dubbed – weakens the dollar.

The jobs report may mean that the Federal Reserve will end its QE program to keep interest rates low and flood markets with cheap money sooner rather than later.

MarketWatch quotes a research note by Nomura Securities that says that "every one-tenth percentage point drop in the unemployment rate would shorten the Fed’s buying by about one month," and Friday’s data "implies a three to four month reduction in QE3-related buying".

QE has been a massive boon for gold.

The Fed's near-zero interest rate policy and bond purchases under QE1 kicked off on 16 December 2008. On 15 December 2008 an ounce of gold cost $837.50.

That's a more than 111% improvement for the precious metal on the back of QE1 and QE2 which followed in August 2010.

Another of the Fed's programs to keep interest rates low, Operation Twist, which started in September 2011 has also boosted the price of gold.

The gold price has taken a few hard knocks from 2011's record levels and the spikes downward have all been thanks to actions or pronouncements by chairman Ben Bernanke and the Fed.

At the same time volatility in the gold price has increased dramatically.

At the start of April for instance gold dropped some $60 an ounce in a single session when Fed minutes appeared to indicate QE3 was off the table and its policy of zero interest rates may be coming to an end sooner than previously thought.

The same thing happened on June 7 when gold dropped $50 to under $1,600 an ounce in a couple of hours after Bernanke delivered "anti-climactic" testimony to the US Congress.

That was not the first time traders got cold feet after breaking an important psychological level.

A similar pattern was followed in the days after the metal reached a record high above $1,900 an ounce in August 2011. The yellow metal slid for two days after hitting the record, losing $105 or 5.6% in value in a single day.

http://www.mining.com/us-labor-dept-drops-bomb-on-gold-traders-75566/?utm_source=digest-en-mining-121005&utm_medium=email&utm_campaign=digest

WRONG AGAIN!

it looks like Rod has sold 5 million shares since December 2011.

Augusta needs to tell their investors that there is a massive battle underway by the locals to halt the development of the mine.

U-TUBE posting about the Santa Ritas.

Nevada Copper buys almost 18% stake in Mercator Minerals

Fri 9:00 am by Brad Lemaire Nevada Copper, headquartered in Vancouver, will shell out 7.32 million of its own stock to buy 46 million shares of Mercator Minerals from Pala Investments.

Nevada Copper Corp. (TSE:NCU) has struck a deal to acquire a 17.8 per cent stake in Mercator Minerals, the company said Friday.

Nevada Copper, headquartered in Vancouver, will shell out 7.32 million of its own stock to buy 46 million shares of Mercator Minerals from Pala Investments.

Mercator Minerals owns the large tonnage copper and molybdenum Mineral Park Mine in Arizona, as well as its El Pilar copper deposit in the State of Sonora in northern Mexico.

The share purchase agreement, expected to close by October 12, is subject to some conditions and Toronto Stock Exchange approval.

Pala Investments, an insider of Nevada Copper, holds 27.38 million shares of Nevada reflecting a 37.4 per cent stake.

Following the deal's close, Pala Investments' stake will rise to 43.1 per cent, or a total of roughly 34.7 million shares.

Nevada said in a statement Friday that the shares of Mercator were acquired for "investment purposes."

Hinging on market conditions and other factors, the company said it may purchase more, or sell, shares in the open market or in private transactions.

Nevada, a junior natural resource company, owns a 100 per cent stake in the Pumpkin Hollow property, in the U.S.

Pumpkin Hollow is a large advanced stage development copper property, which boasts proven and probable mineral reserves of 4.29 billion pounds of copper, 952,000 gold ounces and 27.3 million silver ounces.

Measured and indicated resources, in the Western open pit deposits, as of September totalled 5.4 billion pounds of copper, 981,000 gold ounces and 34 million silver ounces.

In the inferred category, the resource stands at 1.4 billion pounds of copper, 219,000 ounces of gold and 9.3 million silver ounces. The company used a copper cut-off grade of 0.15 per cent.

Shares of Nevada Copper closed Thursday at $3.47 each on the TSX Venture Exchange.

That's called "leaving the door open" so that if by some miracle Marc coughs up the $100,000 due on Oct 20th, and then the $1,000,000 for the Azurite.

My guess is that Marc told Chaffee to have more patience, he is working on getting the funds he told Mr. Chaffee he had last Jan.

Neither WSRA nor GDSM has PR'd that a JV agreement to fund and develop the Azurite mine has been signed!

It is my opinion that there will be no JV for the Azurite unless or until GDSM can guarantee funding of $1,000,000.

Mr. Chaffee has been in 3 JVs with GDSM and all have been problematic with 2 of them going into default. He is not anxious to get into another one without guarantees!

Further there is the $100,000 due to WSRA on Oct 20th and without that payment the GC and GS JV goes into default.

The "Mexican Spotted Owl" as it is referred to here in Arizona is a federally-listed threatened endangered species.

If any of them are found on any of WSRA's mining claims it ends all operations!

And if anyone were out shooting them - there is a $5,000 fine!

TAGG is being pumped - got 2 emails today on it.

PUMPs & dumpS

Red Flagging DANGERS In The Penny Market

XFMY: Pump & Dump comes out ahead of notice of late financials. News must be pretty grim. WATCH OUT! This WILL close red today.

TAGG: TAGGed as "Cavet Emptor" by OTC Markets yesterday, complete with skull and crossbones. Better than 50% drop in last half hour of Thursday's trading.

CWET: Down by better than 50% since P & D began two weeks ago. Down 75% since February P & D. Do you want to hold this one when the pump is over?

TGWI: Already down 20% entering day 3 of Pump & Dump..

SMAA: Straight down from the git go and down 2/3 since May's P & D.

EKNL: Over 3 million shares of stock formerly held by insiders dumped in first week of P & D.

CARN: Losses of as much as 66% since P&D began 3 weeks ago.

From Victory Stocks

Our next pick is: TAGG

Hi Everyone,

Our new social media pick was up to almost 20 cents yesterday before oddly closing at 8 cents. We believe that this opportunity will not last long, and what yesterday showed us is just how quickly TAGG can soar.

If you wanted to buy TAGG yesterday but were not sure about getting in at 15+ cents today should be an absolute no brainer. You can BUY TAGG NOW for 8 cents at the open of the market.

As you know our last social media pick gained almost 1,000% after we alerted it to our members, and it wasn't even nearly as good as TAGG is.

The London, England based TagLikeMe Corp. is positioning itself at the forefront of the social media market.

TagLikeMe announced yesterday that its trial has been so successful that the company is already being compared to Pinterest. TagLikeMe has attracted 200,000 visitors during its trial, and it looks like the company is about to go viral.

The idea behind TagLikeMe is that people will generally go somewhere that has been recommended by someone they know or have interacted with through some form of common interest. By adding this social sharing capability and cross-reference to search results, TagLikeMe.com leverages human interaction to make TagLikeMe.com the most powerful social search and share platform online.

Pinterest is currently the most widely known of the emerging social information networks with over 20 million users and a market value that has rocketed to $1.5 billion, based on its rapidly growing audience that is over 90% female, according to Tech Crunch.

Facebook bought Threadsy . com (a social aggregator somewhat like TAGG) a few weeks ago for an undisclosed sum, but one can only assume it was huge as Facebook's acquisition of Instagram a few months ago carried a $1billion price tag.

Google a few weeks ago bought Wildfire Interactive for 450million dollars. Wildfire is also in the social media arena.

Google, Microsoft, Yahoo and Facebook are in a war where the winner will emerge on top of the social media empire, and the stakes are very high.

These Forbes 500 companies are making numerous acquisitions to give them an edge over their competitors and TagLikeMe could be their next buy out thanks to its unique proven model. It solves a problem that no other social media company has been able to address in the past.

Even a modest $500 million buy out of TagLikeMe would result in the TAGG stock soaring to over $1.50 and produce gains of almost 2,000% from current levels.

A buy out could occur at any moment which is why the time to buy TAGG is probably right now while it is still at around 10 cents because once a buy out is announced it'll be too late and we all know that.

You can visit TagLikeMe . com to start using TAGG's platform and that should convince you of how amazing the company is. Remember the first time you used Google to search for something?

We think that TAGG could hit 50 cents in the short term as WallStreet scoops up cheap shares in hopes and anticipation that Google, Facebook, Microsoft or Yahoo will come in soon and take it over.

Received as an email.

Excellent post!

There are no earthquakes, tornadoes, floods, forest fires or any other natural disasters in the are of the Chloride Copper Mine.

In fact, there is nothing around SIRG's mine that could cause the loss of SIRG's 50M lbs. of copper. With the EA approval SIRG can begin the restoration process and with the APP the construction of a new and enlarged heap leach pad/pond can begin. They will take about 30-45 days.

The old leach pond that will be replaced.

The Rizzo Report increased the reserves and they are higher than previously estimated. The existing ore below the current bench levels from 3695 to 3420 values known between 3420 and 3310 could add another 13 Mlbs. Many holes were abandoned with higher than cut-off grade Cu values in and around the existing pit. Their continuation at depth could prove additional resources. Based on the forgoing, it is safe to assume that the current known resources would provide a minimum of 50 Mlbs of ore; at 5Mlbs/annum, that would support a 10 year mine life.

JESSE JACKSON, WRIGHT 'ARRANGED' OBAMA MARRIAGE

Chicago sources claim president was part of dark subculture

This is the second of a series of articles WND has developed from months of confidential in-person interviews with members of

Trinity United Church of Christ in Chicago who have known Barack and Michelle Obama on a personal basis over many

years. In the first story, members of the church claimed Barack Obama benefited from Wright’s “Down Low Club,” part of a

documented underground subculture in which black men who engage in homosexual activity marry to maintain respectability in

public. Because of the personal risk the sources perceived they were taking to speak candidly about the president and his family,

their identities have been masked.

As a young single woman, Michelle Robinson was a fixture in the home of civil rights leader Jesse Jackson, who along with Rev.

Jeremiah Wright “arranged” her marriage to Barack Obama, according to sources in Chicago who know the couple.

Ads by Google

“If you want to understand Michelle Obama, you’ve got to go back to Jesse Jackson,” a woman called

“Robyn” for this article told WND.

Robyn, who spent several years working for Jackson’s Rainbow PUSH Coalition, explained to a WND

investigator in Chicago that Michelle Obama “just about grew up in Jesse Jackson’s home.”

“Jesse should have charged her rent and board for the amount of time she spent in his home instead of

her own,” she said. Jackson’s daughter, Santita, is still one of Michelle’s best friends. Santita and Jesse

Jr. call her “sis,” short for “sister.”

Santita Jackson said in an interview just before Obama took office in 2008 that she has known Michelle Obama since they car-pooled together as high school classmates. Santita was maid of honor at Michelle and Barack Obama’s wedding, and she is the godmother to the Obama’s older daughter, Malia.

Robyn also pointed out Jesse Jackson Jr., a Democratic Party member of the U.S. House from Illinois, served as the national co-chairman of Obama’s 2008 presidential campaign.

“It all relates back to Trinity and to the Jesse Jackson orbit of blacks here in Chicago who gave Obama

legitimacy and helped him establish his identity as a black man,” Robyn explained.

“The political left wanted to push a black to the presidency, and the key operatives in the Democratic Party decided long ago it wouldn’t be Jesse Jackson (Sr.). Then Jesse wanted it to be his son, but Jesse Jr. has serious drug and mental problems that the world knows about now. These were also known about in the past, and Jesse Jr. was never going to be the black president. So, the political left then chose Obama.”

In an interview with the Chicago Sun-Times in August, Sandi Jackson admitted her husband, Jesse Jr., was “completely debilitated by depression,” which has forced him to put his Washington home for sale to pay his medical bills, including his treatment at the Mayo Clinic. He has been absent from Congress since mid-June, putting his House seat at risk in the November election.

They met where?

Obama’s retelling of an event most spouses remember precisely for the rest of their lives has caused confusion. Exactly when and how did he first meet Michelle Robinson?

Before a speech at the New Economic School graduation in Moscow on July 7, 2009, Obama stated he first met Michelle in school.

“I don’t know if anybody else will meet their future wife or husband in class like I did, but I’m sure you’re all going to have wonderful careers,” he said, according to Newsweek.

The problem is that Michelle Obama earned her degree from Harvard Law School in 1988, and Obama did not arrive at Harvard Law School until that fall, graduating three years later in 1991.

The commonly accepted story is that they first met in Chicago in 1989, when Barack took a summer job as an intern at the Chicago law firm Sidley Austin, and Michelle, who was employed as a lawyer at the firm, was assigned to be his mentor.

WND has reported Allen Hulton, the U.S. postal carrier who delivered mail to the parents of Weather Underground bomber Bill Ayers in a Chicago suburb, met Obama in the summer of 1989, while Obama was an intern at Sidley Austin.

In 1991, during their engagement to be married, top Obama adviser Valerie Jarrett, then serving as the deputy chief of staff to Mayor Richard M. Daley, hired Michelle to a job in the mayor’s office.

“Michelle hated working for the city even more than she hated working at Sidley Austin,” Robyn told WND.

“At the law firm, she lasted so short of a time because they expected her to do work,” Robyn said. “At the City of Chicago, where she worked under Mayor Daley, Michelle had one of those ‘Jesse hires’ positions. These are patronage jobs where the recipients did nothing.”

Robyn claimed that while working for Daley, Michelle just collected a check, doing very little work.

“She sat at a desk and read the newspaper all day,” Robyn said. “Sometimes she read romance novel paperbacks. No one could say anything to her because she was a ‘Jesse hire.’ This meant if anyone did complain about her not working that Jesse Jackson would get mad at Daley over that, and there would be trouble.”

Robyn said Michelle was “essentially treated like she was Jesse’s daughter, and Michelle’s connections in Chicago were a key to Obama’s rise to power.”

Connections

Political connections played throughout Michelle’s young life in Chicago.

Her father, Fraser C. Robinson III, who was diagnosed with multiple sclerosis in his 20s and eventually walked with the use of crutches, was a volunteer Democratic precinct captain in addition to his job in the boiler room at Chicago’s water purification plant.

As Democratic precinct captain, Robinson had power and influence, given his access to “street money” the Daley machine freely handed out at that time in Chicago’s South Side to make sure black voters turned out to vote for Democratic Party machine candidates.

The Chicago sources told WND the selection of Michelle Robinson for Obama was made by Jesse Jackson, and Jeremiah Wright agreed it would be a good combination.

“It all relates back to Trinity United and to the Jesse Jackson orbit of blacks here in Chicago who gave Obama legitimacy and helped him establish his identity as a black man ‘from Chicago,’” Robyn explained.

“Michelle came from a political family; she was intelligent even if she didn’t really like to work. Wright knew Obama was gay, but he needed the cover of a wife if he were to succeed in politics.”

A current member of Trinity church who has known the Obamas for 20 years, “Carolyn,” confirmed Trinity “helped a lot of blacks get successful and connected.”

“That’s what Wright did for Obama,” she claimed. “He connected Obama in the community, and he helped Obama hide his homosexuality.”

According to Robyn, Jackson explained to Michelle that she would live a life of luxury once Obama was president, and that she never again would have to worry about money.

“Michelle was nasty, and most straight guys would never be able to put up with her moods and temperament,” Robyn maintained. “But Obama really didn’t care. Michelle had the credentials and she looked the part. Obama wasn’t interested in her for sex.”

A source WND will identify as Hazel, a long-term member of the Trinity congregation, insisted Obama remained sexually involved with men after his marriage to Michelle.

“I remember being at this function at Reverend Wright’s house, one of the many parties Wright had, in 1996,” Hazel recalled.

“I went to the room where all the coats were on the bed, because I wanted to leave. I was surprised to find the light in the room was off and the coats were on the floor,” she said. “Then I realized there were two men hugging and kissing in there. One of those men was Obama. This was long before anybody knew Obama, before he became famous like he is today.”

Hazel has been telling this story in Chicago since 1996.

Cushy job

When Jarrett left Mayor Daley’s office to head Chicago’s Department of Planning and Development, she took Michelle with her. Jarrett later became the chairwoman of the Chicago Medical Center, and Michelle again got “a cushy job at the Chicago Medical Center with a salary of $317,000,” as reported by Edward Klein on page 117 of his 2012 book “The Amateur: Barack Obama in the White House.”

New York Times reporter Jodi Kantor wrote in 2008 that Jarrett would have to be at the top of a list of people who helped Barack and Michelle Obama.

“Nearly two decades ago, Ms. Jarrett swept the young lawyers under her wing, introduced them to a wealthier and better-connected Chicago than their own, and eventually secured contacts and money essential to Mr. Obama’s long-shot Senate victory,” Kantor wrote.

Klein, in an interview with Fox News, described Jarrett as the “de facto” president of the United States, “the best friend of the first lady and soul mate of the president.”

Santita Jackson said in an interview just before Obama took office in 2008 that she has known Michelle Obama since they car-pooled together as high school classmates. Santita was maid of honor at Michelle and Barack Obama’s wedding, and she is the godmother to the Obama’s older daughter, Malia.

Robyn also pointed out Jesse Jackson Jr., a Democratic Party member of the U.S. House from Illinois, served as the national co-chairman of Obama’s 2008 presidential campaign.

“It all relates back to Trinity and to the Jesse Jackson orbit of blacks here in Chicago who gave Obama legitimacy and helped him establish his identity as a black man,” Robyn explained.

“The political left wanted to push a black to the presidency, and the key operatives in the Democratic Party decided long ago it wouldn’t be Jesse Jackson (Sr.). Then Jesse wanted it to be his son, but Jesse Jr. has serious drug and mental problems that the world knows about now. These were also known about in the past, and Jesse Jr. was never going to be the black president. So, the political left then chose Obama.”

In an interview with the Chicago Sun-Times in August, Sandi Jackson admitted her husband, Jesse Jr., was “completely debilitated by depression,” which has forced him to put his Washington home for sale to pay his medical bills, including his treatment at the Mayo Clinic. He has been absent from Congress since mid-June, putting his House seat at risk in the November election.

Obama’s retelling of an event most spouses remember precisely for the rest of their lives has caused confusion. Exactly when and how did he first meet Michelle Robinson?

Before a speech at the New Economic School graduation in Moscow on July 7, 2009, Obama stated he first met Michelle in school.

“I don’t know if anybody else will meet their future wife or husband in class like I did, but I’m sure you’re all going to have wonderful careers,” he said, according to Newsweek.

The problem is that Michelle Obama earned her degree from Harvard Law School in 1988, and Obama did not arrive at Harvard Law School until that fall, graduating three years later in 1991.

The commonly accepted story is that they first met in Chicago in 1989, when Barack took a summer job as an intern at the Chicago law firm Sidley Austin, and Michelle, who was employed as a lawyer at the firm, was assigned to be his mentor.

WND has reported Allen Hulton, the U.S. postal carrier who delivered mail to the parents of Weather Underground bomber Bill Ayers in a Chicago suburb, met Obama in the summer of 1989, while Obama was an intern at Sidley Austin.

In 1991, during their engagement to be married, top Obama adviser Valerie Jarrett, then serving as the deputy chief of staff to Mayor Richard M. Daley, hired Michelle to a job in the mayor’s office.

“Michelle hated working for the city even more than she hated working at Sidley Austin,” Robyn told WND.

“At the law firm, she lasted so short of a time because they expected her to do work,” Robyn said. “At the City of Chicago, where she worked under Mayor Daley, Michelle had one of those ‘Jesse hires’ positions. These are patronage jobs where the recipients did nothing.”

Robyn claimed that while working for Daley, Michelle just collected a check, doing very little work.

“She sat at a desk and read the newspaper all day,” Robyn said. “Sometimes she read romance novel paperbacks. No one could say anything to her because she was a ‘Jesse hire.’ This meant if anyone did complain about her not working that Jesse Jackson would get mad at Daley over that, and there would be trouble.”

Robyn said Michelle was “essentially treated like she was Jesse’s daughter, and Michelle’s connections in Chicago were a key to Obama’s rise to power.”

Connections

Political connections played throughout Michelle’s young life in Chicago.

Her father, Fraser C. Robinson III, who was diagnosed with multiple sclerosis in his 20s and eventually walked with the use of crutches, was a volunteer Democratic precinct captain in addition to his job in the boiler room at Chicago’s water purification plant.

As Democratic precinct captain, Robinson had power and influence, given his access to “street money” the Daley machine freely handed out at that time in Chicago’s South Side to make sure black voters turned out to vote for Democratic Party machine candidates.

The Chicago sources told WND the selection of Michelle Robinson for Obama was made by Jesse Jackson, and Jeremiah Wright agreed it would be a good combination.

“It all relates back to Trinity United and to the Jesse Jackson orbit of blacks here in Chicago who gave Obama legitimacy and helped him establish his identity as a black man ‘from Chicago,’” Robyn explained.

“Michelle came from a political family; she was intelligent even if she didn’t really like to work. Wright knew Obama was gay, but he needed the cover of a wife if he were to succeed in politics.”

A current member of Trinity church who has known the Obamas for 20 years, “Carolyn,” confirmed Trinity “helped a lot of blacks get successful and connected.”

“That’s what Wright did for Obama,” she claimed. “He connected Obama in the community, and he helped Obama hide his homosexuality.”

According to Robyn, Jackson explained to Michelle that she would live a life of luxury once Obama was president, and that she never again would have to worry about money.

“Michelle was nasty, and most straight guys would never be able to put up with her moods and temperament,” Robyn maintained. “But Obama really didn’t care. Michelle had the credentials and she looked the part. Obama wasn’t interested in her for sex.”

A source WND will identify as Hazel, a long-term member of the Trinity congregation, insisted Obama remained sexually involved with men after his marriage to Michelle.

“I remember being at this function at Reverend Wright’s house, one of the many parties Wright had, in 1996,” Hazel recalled.

“I went to the room where all the coats were on the bed, because I wanted to leave. I was surprised to find the light in the room was off and the coats were on the floor,” she said. “Then I realized there were two men hugging and kissing in there. One of those men was Obama. This was long before anybody knew Obama, before he became famous like he is today.”

Hazel has been telling this story in Chicago since 1996.

Cushy job

When Jarrett left Mayor Daley’s office to head Chicago’s Department of Planning and Development, she took Michelle with her.

Jarrett later became the chairwoman of the Chicago Medical Center, and Michelle again got “a cushy job at the Chicago Medical Center with a salary of $317,000,” as reported by Edward Klein on page 117 of his 2012 book “The Amateur: Barack Obama in the White House.”

New York Times reporter Jodi Kantor wrote in 2008 that Jarrett would have to be at the top of a list of people who helped Barack and Michelle Obama.

“Nearly two decades ago, Ms. Jarrett swept the young lawyers under her wing, introduced them to a wealthier and better-connected Chicago than their own, and eventually secured contacts and money essential to Mr. Obama’s long-shot Senate victory,” Kantor wrote.

Klein, in an interview with Fox News, described Jarrett as the “de facto” president of the United States, “the best friend of the first lady and soul mate of the president.”

http://www.wnd.com/2012/10/jesse-jackson-wright-arranged-obama-marriage/

They met where?

Does anyone know if HMNC poured any dore bars?

Dems are blaming the high altitude for odumber's poor performance!

Can't wait for the next debate! Ryan will make mincemeat out of Biden!

Look at the look on Michelle's face! She's afraid she is going to lose all those perks, trips and the celebrity life style!

A New Look at Old Mines

by Chris Ralph

(Old article but interesting.)

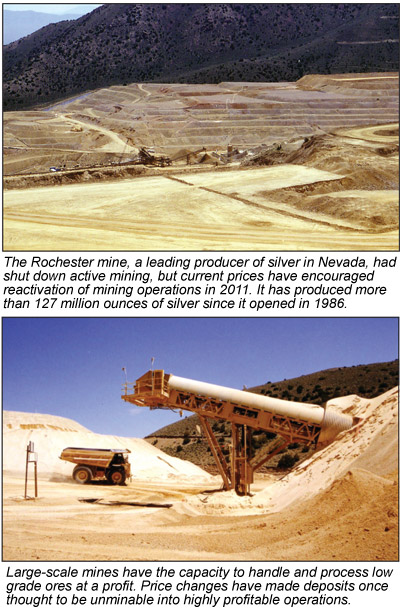

Record high precious metals prices have been prominent in virtually all forms of the news media in recent months. While many folks are looking to accumulate metals for themselves, these price changes are starting to produce a revolution in the precious metals mining industry. Elevated values are completely turning over the economics of gold mining around the world and creating new opportunities for gold prospectors and precious metals exploration companies. Gold and silver mining has never been easy, but the significant price increases of the past year have changed the concept of what ores can and cannot be profitably mined. Geologists and prospectors around the world are now moving quickly to take a new look at old mining properties once thought too low in grade to work as potential new sources of gold and silver.

The exploration boom of the 1980s and 1990s identified many rich new properties, but there were also a good number of low grade marginal properties in the western US and elsewhere. A fine example is the Goldbanks mine property in Pershing County, Nevada. Nearly put into production more than a decade ago by Kinross, initiation of production at the property was delayed and never actually started because of various reasons, mostly due to the low price for gold at the time. Falling prices sunk the project before it could get off the ground as the generally low grade of the deposit, combined with a poor outlook for gold prices, resulted in the project being deemed unprofitable at the time. The ore remains in place and it is still a well-identified resource that is now far more attractive given the current prices of precious metals.

The Pan deposit in White Pine County, Nevada, which is now being moved toward production by Midway Gold Corp., is another example of this type of situation. These examples are not just isolated unusual occurrences because a considerable number of similar lower grade properties also exist in many areas.

In addition to resources that were just never put into production, there are also many other projects that were mined during the same time frame but left behind large halos of lower grade material that were unprofitable to work at the time. Gold-bearing rock encircling these older pits may also now be of interest. Both the Hog Ranch and Wind Mountain properties in Nevada come to mind as examples of this type of situation. Even old heap leach piles, which were originally worked using uncrushed run-of-mine ore, may be economically removed, crushed and re-leached with the extra recovery from crushing paying for the costs of processing with a tidy profit left over. Even old low grade dumps may be of interest for processing under current conditions.

Consider this example of the simple economics that today’s higher metal prices offer: Using ballpark numbers for heap leach projects from the 1990s, a typical cost would be something in the range of $3 per ton to mine and process ore, and $1.50 to dig and dispose of waste. We can use as an example a low grade ore grading 0.03 ounces of gold per ton that has a recovery rate of 65% from heap leaching and requires 3 tons of waste to be moved for each ton of ore produced. With our ballpark costs and the example low grade ore numbers, it’s easy to show that at late 1990s prices it would not be economic to mine that ore. It would cost $7.50 per ton to mine and process the ore as well as move the necessary waste to access it, yet at $350 per ounce it would yield only $6.82 for 0.03 ounces of gold. Working that ore would be a money-losing proposition.

While this was just an example, the economics of the time were very real, and many gold mines working lower grade ores were shut down in the 1990s when gold dropped below $350 per troy ounce.

Let’s take a look at this same example using current prices and see what a difference adding $1,000 per ounce to the price of gold can make. Today’s mining costs would be a bit higher, so equivalent costs might be on the order of $5 to mine and process ore, with $2.50 needed to dispose of waste rock. Yet, in spite of higher costs, the economics are totally different. The same low grade ore would now cost $12.50 to mine and process, but at $1,350 per ounce it would yield $25.35, providing a generous profit of nearly $13 per ton. No question that making a profit of nearly $13 per ton is a whole lot better than losing about $0.70 for each ton. Multiply this by the typical production rate of a big open pit mine that would be handling many thousands of tons per day and you get a feel for why these new prices are creating such a rebirth in the mining industry. Given the proper leach and stripping characteristics, ores as low 0.007 ounces per ton, often considered as waste in the past, may be profitable to mine. It is this type of major change in the economics of low grade ore that has geologists all across the world scrambling to review old data on low grade deposits, as well as the lower grade halos surrounding previously mined deposits and the down dip extensions of previously mined deposits that were thought to be too deep to pay for the costs of overburden stripping.

This same concept applies not only to large scale open pit mines, but to smaller commercial placer mines as well. Gravels that were previously unprofitable are now in many cases potentially very worthwhile to mine. As a result, operations given up long ago as money losers now have the capability to yield handsome returns. Many placer operators are also re-evaluating any old properties with identified low grade resources. As placer operations are generally a lower cost to capitalize, many smaller operators are focusing on these opportunities. In fact, many folks not previously involved in gold mining are even considering this option, as demonstrated on a recent popular TV reality show about inexperienced placer miners in Alaska.

Since this whole effect of making low grade material profitable is based on elevated metals prices, one wonders how long will these high precious metal prices last. Could they just be a temporary flash in the pan? While they seem fairly stable at the present time, no one really knows for sure. If the price does stay high, its likely the coming years will bring increases in gold and silver production as some of these lower grade operations come on line. I had an old professor who used to say that nothing cures high prices like high prices. What he meant was that high prices attract new production, leading to a drop in those same high prices. It’s just the action of basic economic theories of supply and demand. New supplies come onto the market and meet the needs of excess demand, resulting in a drop in prices.

Yet the economics of gold are a lot different than they were in the 1980s and 1990s. During those times, many governments and related agencies like the International Monetary Fund were pumping large amounts of gold onto the world market. Gold was seen by many as a relic of the past—an inferior asset that yielded no interest and cost money to store. It was thought that it was best to get rid of it and at least get some cash that could be used or loaned out. Great Britain, once a large holder of gold, sold nearly every ounce it had. These actions seemed sensible to some at the time. The runaway inflation of the 1970s had been stopped, the dollar was king, and most governments were behaving responsibly with their currencies. Only banana republics headed by crazy dictators would be irresponsible enough to manufacture money out of thin air, leading to runaway inflation. The huge amounts of gold that were dumped onto the market by government sources, together with new production from operating mines, greatly depressed prices; gold spent years languishing at less than $350 per ounce.

Fast forward to the present time, and the idea of simply manufacturing large amounts of money has become something that our federal government does on a large scale and is seen by some economists as a wise practice. A number of governments now use techniques to intentionally depress the price of their currencies so that they can increase exports. Some have termed it a currency war or the “race to debase” (their currency). Each time a government manufactures money out of thin air, the value of their currency is automatically worth a bit less than it was before. To protect assets from this backhanded form of devaluation, both individuals and governments are now buying gold.

In the 1980s and 1990s governments were huge net sellers of gold, but things have changed and now they have become significant net buyers of gold. Individuals, fearing the consequences of reckless spending and unending money expansion have looked to gold, silver and other precious metals as an important store of wealth. These metals have become an alternative form of currency that is safer because no government can simply create gold out of thin air. The fundamentals of today’s gold and silver markets seem to promise even more strength than the precious metals markets of the late 1970s and early 1980s. So it appears that strong precious metals prices are not just a temporary blip on the world radar because changes in both government and investor demand for them means they will be with us for a while.

What can prospectors focus on to unlock this new opportunity and find these kinds of deposits? Look to regions where gold has been produced in the past and search for locations that may have been drilled previously but given up by the former operators as too small and too low in grade to be worthwhile. Old reports and industry records list past exploration drilling campaigns, including the unsuccessful ones. While few deposits of this type are likely still open to claim, there may still be a small number. Sometimes past exploration firms gave up on deposits of low grade ore without thorough drilling and testing simply because the marginal grades seemed too low to be worth pursuing or the exploration company found it difficult to raise additional funds based on seemingly uneconomic results. Those with only a few low grade holes are the ones most likely to be unclaimed.

Sometimes additional low grade deposits will line up along a fault zone on trend with known or previously mined deposits, especially in areas with similar geology to the known deposits. A soil sampling program may indicate unusual concentrations of gold or silver or pathfinder metals such as arsenic, antimony or mercury. Every district has its own unique characteristics, and it’s worthwhile to study the geology and structural controls that have formed valuable deposits. Those that understand the geology of the regions they are exploring will have a distinct advantage in their search.

Exploration companies are actively looking for properties with profitable potential, even if the ground was once cast off as too low in grade to be economically viable. This is especially true in states that are reasonably friendly toward mining and deposits in stable countries like the US, Canada and Australia are the most desirable. Smart prospectors will be out taking a look at the potential ground that just might meet those needs, find those opportunities and market their properties to the mining firms seeking favorable locations to explore.

A New Look at Old Mines

by Chris Ralph

Record high precious metals prices have been prominent in virtually all forms of the news media in recent months. While many folks are looking to accumulate metals for themselves, these price changes are starting to produce a revolution in the precious metals mining industry. Elevated values are completely turning over the economics of gold mining around the world and creating new opportunities for gold prospectors and precious metals exploration companies. Gold and silver mining has never been easy, but the significant price increases of the past year have changed the concept of what ores can and cannot be profitably mined. Geologists and prospectors around the world are now moving quickly to take a new look at old mining properties once thought too low in grade to work as potential new sources of gold and silver.

The exploration boom of the 1980s and 1990s identified many rich new properties, but there were also a good number of low grade marginal properties in the western US and elsewhere. A fine example is the Goldbanks mine property in Pershing County, Nevada. Nearly put into production more than a decade ago by Kinross, initiation of production at the property was delayed and never actually started because of various reasons, mostly due to the low price for gold at the time. Falling prices sunk the project before it could get off the ground as the generally low grade of the deposit, combined with a poor outlook for gold prices, resulted in the project being deemed unprofitable at the time. The ore remains in place and it is still a well-identified resource that is now far more attractive given the current prices of precious metals.

The Pan deposit in White Pine County, Nevada, which is now being moved toward production by Midway Gold Corp., is another example of this type of situation. These examples are not just isolated unusual occurrences because a considerable number of similar lower grade properties also exist in many areas.

In addition to resources that were just never put into production, there are also many other projects that were mined during the same time frame but left behind large halos of lower grade material that were unprofitable to work at the time. Gold-bearing rock encircling these older pits may also now be of interest. Both the Hog Ranch and Wind Mountain properties in Nevada come to mind as examples of this type of situation. Even old heap leach piles, which were originally worked using uncrushed run-of-mine ore, may be economically removed, crushed and re-leached with the extra recovery from crushing paying for the costs of processing with a tidy profit left over. Even old low grade dumps may be of interest for processing under current conditions.

Consider this example of the simple economics that today’s higher metal prices offer: Using ballpark numbers for heap leach projects from the 1990s, a typical cost would be something in the range of $3 per ton to mine and process ore, and $1.50 to dig and dispose of waste. We can use as an example a low grade ore grading 0.03 ounces of gold per ton that has a recovery rate of 65% from heap leaching and requires 3 tons of waste to be moved for each ton of ore produced. With our ballpark costs and the example low grade ore numbers, it’s easy to show that at late 1990s prices it would not be economic to mine that ore. It would cost $7.50 per ton to mine and process the ore as well as move the necessary waste to access it, yet at $350 per ounce it would yield only $6.82 for 0.03 ounces of gold. Working that ore would be a money-losing proposition.

While this was just an example, the economics of the time were very real, and many gold mines working lower grade ores were shut down in the 1990s when gold dropped below $350 per troy ounce.

Let’s take a look at this same example using current prices and see what a difference adding $1,000 per ounce to the price of gold can make. Today’s mining costs would be a bit higher, so equivalent costs might be on the order of $5 to mine and process ore, with $2.50 needed to dispose of waste rock. Yet, in spite of higher costs, the economics are totally different. The same low grade ore would now cost $12.50 to mine and process, but at $1,350 per ounce it would yield $25.35, providing a generous profit of nearly $13 per ton. No question that making a profit of nearly $13 per ton is a whole lot better than losing about $0.70 for each ton. Multiply this by the typical production rate of a big open pit mine that would be handling many thousands of tons per day and you get a feel for why these new prices are creating such a rebirth in the mining industry. Given the proper leach and stripping characteristics, ores as low 0.007 ounces per ton, often considered as waste in the past, may be profitable to mine. It is this type of major change in the economics of low grade ore that has geologists all across the world scrambling to review old data on low grade deposits, as well as the lower grade halos surrounding previously mined deposits and the down dip extensions of previously mined deposits that were thought to be too deep to pay for the costs of overburden stripping.

This same concept applies not only to large scale open pit mines, but to smaller commercial placer mines as well. Gravels that were previously unprofitable are now in many cases potentially very worthwhile to mine. As a result, operations given up long ago as money losers now have the capability to yield handsome returns. Many placer operators are also re-evaluating any old properties with identified low grade resources. As placer operations are generally a lower cost to capitalize, many smaller operators are focusing on these opportunities. In fact, many folks not previously involved in gold mining are even considering this option, as demonstrated on a recent popular TV reality show about inexperienced placer miners in Alaska.

Since this whole effect of making low grade material profitable is based on elevated metals prices, one wonders how long will these high precious metal prices last. Could they just be a temporary flash in the pan? While they seem fairly stable at the present time, no one really knows for sure. If the price does stay high, its likely the coming years will bring increases in gold and silver production as some of these lower grade operations come on line. I had an old professor who used to say that nothing cures high prices like high prices. What he meant was that high prices attract new production, leading to a drop in those same high prices. It’s just the action of basic economic theories of supply and demand. New supplies come onto the market and meet the needs of excess demand, resulting in a drop in prices.

Yet the economics of gold are a lot different than they were in the 1980s and 1990s. During those times, many governments and related agencies like the International Monetary Fund were pumping large amounts of gold onto the world market. Gold was seen by many as a relic of the past—an inferior asset that yielded no interest and cost money to store. It was thought that it was best to get rid of it and at least get some cash that could be used or loaned out. Great Britain, once a large holder of gold, sold nearly every ounce it had. These actions seemed sensible to some at the time. The runaway inflation of the 1970s had been stopped, the dollar was king, and most governments were behaving responsibly with their currencies. Only banana republics headed by crazy dictators would be irresponsible enough to manufacture money out of thin air, leading to runaway inflation. The huge amounts of gold that were dumped onto the market by government sources, together with new production from operating mines, greatly depressed prices; gold spent years languishing at less than $350 per ounce.

Fast forward to the present time, and the idea of simply manufacturing large amounts of money has become something that our federal government does on a large scale and is seen by some economists as a wise practice. A number of governments now use techniques to intentionally depress the price of their currencies so that they can increase exports. Some have termed it a currency war or the “race to debase” (their currency). Each time a government manufactures money out of thin air, the value of their currency is automatically worth a bit less than it was before. To protect assets from this backhanded form of devaluation, both individuals and governments are now buying gold.

In the 1980s and 1990s governments were huge net sellers of gold, but things have changed and now they have become significant net buyers of gold. Individuals, fearing the consequences of reckless spending and unending money expansion have looked to gold, silver and other precious metals as an important store of wealth. These metals have become an alternative form of currency that is safer because no government can simply create gold out of thin air. The fundamentals of today’s gold and silver markets seem to promise even more strength than the precious metals markets of the late 1970s and early 1980s. So it appears that strong precious metals prices are not just a temporary blip on the world radar because changes in both government and investor demand for them means they will be with us for a while.

What can prospectors focus on to unlock this new opportunity and find these kinds of deposits? Look to regions where gold has been produced in the past and search for locations that may have been drilled previously but given up by the former operators as too small and too low in grade to be worthwhile. Old reports and industry records list past exploration drilling campaigns, including the unsuccessful ones. While few deposits of this type are likely still open to claim, there may still be a small number. Sometimes past exploration firms gave up on deposits of low grade ore without thorough drilling and testing simply because the marginal grades seemed too low to be worth pursuing or the exploration company found it difficult to raise additional funds based on seemingly uneconomic results. Those with only a few low grade holes are the ones most likely to be unclaimed.

Sometimes additional low grade deposits will line up along a fault zone on trend with known or previously mined deposits, especially in areas with similar geology to the known deposits. A soil sampling program may indicate unusual concentrations of gold or silver or pathfinder metals such as arsenic, antimony or mercury. Every district has its own unique characteristics, and it’s worthwhile to study the geology and structural controls that have formed valuable deposits. Those that understand the geology of the regions they are exploring will have a distinct advantage in their search.

Exploration companies are actively looking for properties with profitable potential, even if the ground was once cast off as too low in grade to be economically viable. This is especially true in states that are reasonably friendly toward mining and deposits in stable countries like the US, Canada and Australia are the most desirable. Smart prospectors will be out taking a look at the potential ground that just might meet those needs, find those opportunities and market their properties to the mining firms seeking favorable locations to explore.

WRONG AGAIN! The market is open on Monday and it is not an observed market holiday.

The funding from Harmony was still in tact when Rod was elected CEO so he had no reason to search for funding until the middle of Oct.

Rod was elected CEO on Aug. 26, 2011. He has been on the job for 14 months and has accomplished twice as much in those 14 months than the former CEO did in his 16 months! It should have been the responsibility of the former CEO, Patrick Champney to research those permits instead of sitting on his butt!

October 12, 2011 This Agreement has been terminated by mutual agreement between the Company and Harmony. All prior terms of this agreement are void and no longer valid.

It was also said around 9 months ago that sirg had funding

WSRA has their current projects underway, the Silver Cord, Gold Basin and the Azurite.

WSRA has not been able to sell enough of those GDSM Series E Preferred Convertible shares to raise the $400,000 that was part of the JV funding agreement.

Just my guess for the reason Marc filed that Aug. 16th amendment to change that conversion rate to 15-1 to make those shares more attractive to investors.

Did you find the mistake in the last 2 filings and the likely reason Paradiso has not released the attorney letter? If not PM and I can show it.

Never said I did not check Arizona and please stop posting mis-leasing information. I called AZBOTR and they confirmed that Jenkins was not registered. Last May I did not know AZBOTR had a searchable database online and that confirms that he has NEVER been registered as either a geologist nor an engineer.

If you want to pursue the investigation it is Case #M13-008.

Sorry it appears a failure to read the entire post resulted in a mis-statement. I NEVER stated that he was revoked. Please read the post again!

Let us remember that Mr. Jenkins was under investigation with the American Society of Professional Geologists and resigned his membership/registration early last spring prior to either the GC, GS or Azurite reports being released!

The JV requires the Company to fund the 4 phases of development under the following funding schedule:

1) First Payment $25,000 due 10 business days of execution of this agreement (PHASE I)

2) Second payment of $50,000 due 30 days from first payment above (PHASE I)

3) Third payment of $350,000 due 120 days from first payment above (PHASE II)

4) Forth payment of $100,000 due 240 days from first payment above (PHASE III)

5) Fifth payment of $600,000 due 365 days from first payment above (PHASE IV)

6) Sixth payment of $250,000 due 425 days from first payment above (PHASE IV)

Note: Funding may be modified by mutual consent as development process progresses.

Western Sierra Mining agreed to sell 40mm Series E Preferred Stock it received in 2009 from the Company to a group of investors for $400,000.

These preferred shares were issued to Western Sierra Mining in 2009 as part of the parties previous joint venture efforts. Western Sierra Mining has agreed to apply these funds, on behalf of the Company, to the funding schedule above therefore completing the funding required for Phase I and II of the claims development.

As consideration for the sale of the preferred shares, the Company has agreed to assign back to Western Sierra Mining 5% of its joint venture interest in the claims. The Company may buy back the 5% interest for $100,000.

Additionally, the Company has agreed to issue Western Sierra Mining four million shares of a new series of preferred that may be converted to common in 1 year.

However the Amendment filed by Marc on Aug. 16th does not have a one year restriction and the conversion rate was changed to 15-1.

For the record, GDSM posting the Azurite report on their website is not what got Jenkins in trouble.

WSRA is moving forward as stated in Mr. Chaffee's Shareholder Update. Not so sure about GDSM as no further work has been done on the Gold Crown nor the Gold Star.

I am sure everyone must remember those "Phases"

Phase 2 is about to begin (April 24th )and will be complete in late summer (August / September?) of this year. This phase is small scale gold production.

Why has there been NO GOLD PRODUCTION?

NI 43-101 completion is to begin shortly. What is meant by "shortly" - that was April - this is October - is 6 months "shortly"?

Phase 3 to begin in late summer of this year. This is the beginning of full scale production.

It is now October and there is ZERO gold production and not the full scale production PRd by Marc. Clearly things did not progress as smoothly as promised.

It was previously posted that 9 months (last Dec) ago Rod was actively seeking another source of funding without the need to use Asher.

The article further shows that last Dec. Rod expected the permitting to take 4 to 6 months but didn't know that SIRG would be at the mercy of government agencies and beyond his control!

But instead of dropping the ball, Rod stepped up to the plate and hit a home run by hiring Rizzo & Assoc to get the MPO approved!

Now that the E is gone that fact leaves one less hurdle to jump over and one less negative event to discuss. And as threatened, SIRG did not get downgraded to the pinks.

Seeking funding of $2 million. Sierra Resource Group, Inc. is a past producing copper mine in Arizona with existing plant and equipment (retooling 90 days) and permits ( updating 4-6 months).

We seek $2 million (fully secured) to bring the mine into full production producing seven million pounds of 99.999% pure copper cathode per year.

The mine has proven reserves of 27 million pounds (NI 43-101 compliant Technical and 9.9 million pounds of copper in Tailings.

The Mine is fully developed for operation with substantial investments expended to date. SX/EW plant as well as required infrastructure to conduct the full operation is already in place.

Contact: J Rod Martin

Rodmartinmail@gmail.com

305 439 7416

serriaresgroup.com serriaresgroup.com

9 months ago

To easy, the big ole "E" was not dropped yesterday, and it will not be dropped today either. I see sirgE getting down graded again in the very near future. I Wonder which toxic financer paid for the recent pump?

I see that the Mining Property and Ore Reserves that are/were the assets of WSRA were removed from the ASSETS. GEAR also disclosed that the agreement was cancelled on April 1, 2012 so why were those assets included in their annual financial statement when the deal never was completed?

No clue why it took over 3 months to release this rather simple and mostly boiler plate financial statement.

The WSRA/GDSM JV for the Gold Crown and Gold Star is contingent on GDSM making the $100,000 payment due on Oct. 20th. If GDSM fails to make that payment the JV goes into default.

Clearly Chaffee is not spending any more time on those claims as he stated they are proceeding with the Silver Cord (without GEAR) and completing basic power and lighting installations.

We have continued to work closely with Pine Creek mining to re-open the Gold Basin placer mine. We have recently completed additional fencing and earth control barriers at the request of the U.S. Forest Service. We are looking at a variety of possibilities to Joint Venture the project with Pine Creek as an operating partner or as the mine operator for an outside or private developer.

That GDSM/WSRA shareholder meeting was announced on Aug. 21st and Mr. Chaffee told me that he was waiting for Marc to set a date, which never happened. It does not take 5 weeks to pick a date.

I fear things are not going as smooth as shareholders would like and publishing the Azurite report on the GDSM website without permission did not help the relationship and got Jenkins in trouble with the Arizona Dept of Technical Registration.

Harmony says Wafi-Golpu could support $9.8 billion mine

Frik Els | September 28, 2012

Johannesburg-based Harmony Gold Mining (NYSE:HMY) has outlined the potential of the Wafi-Golpu project, a 50-50 JV with Australia's Newcrest Mining in Papua New Guinea, saying in a presentation the deposit could support a $9.8 billion mine with peak annual production of 560,000 gold ounces and 335,000 tonnes of copper.

The mine with a 26-year mine life will cost $4.85 billion to bring to production with annual output at 490,000 ounces of gold and 290,000 tonnes of copper with start-up in 2019 followed by expansion.

The economics of the mainly underground mine located 80 km from the port of Lae is sweet – gold output will cost a negative $2,600 an ounce while copper would be extracted for just $0.54 a pound. Copper was trading at $3.76 in New York on Friday.

The market has been anticipating great things from Wafi-Golpu. Harmony's 2007 pre-feasibility study showed a 1.3 million oz gold and below 1 million tonnes of copper. This has now grown to contain roughly 12.4 million ounces of gold and 5.4 million tonnes of copper.

Harmony Gold says the site is highly prospective and will embark on a feasibility study next year with a focus on enhancing gold recovery which is pegged at 61% at the moment and a $400 million drilling program. Discussions with local landowners are also ongoing.

Harmony Gold's Australian partners Newcrest's (TSX:NM, ASX:NCM) Lihir gold mine in Papua New Guinea has run into trouble with landowners over compensation and the 600,000 gold oz per year mine had to be briefly shut in August.

The government of PNG has the option to take a 30% stake in the Wafi-Golpu mine at cost.

Chart is from Harmony Gold's presentation to analysts – click here for more on Wafi-Golpu.

http://www.mining.com/harmony-and-newcrests-wafi-golpu-could-grow-to-9-8-billion-project-54152/?utm_source=digest-en-cu-121002&utm_medium=email&utm_campaign=digest

Harmony says Wafi-Golpu could support $9.8 billion mine

Frik Els | September 28, 2012

Johannesburg-based Harmony Gold Mining (NYSE:HMY) has outlined the potential of the Wafi-Golpu project, a 50-50 JV with Australia's Newcrest Mining in Papua New Guinea, saying in a presentation the deposit could support a $9.8 billion mine with peak annual production of 560,000 gold ounces and 335,000 tonnes of copper.

The mine with a 26-year mine life will cost $4.85 billion to bring to production with annual output at 490,000 ounces of gold and 290,000 tonnes of copper with start-up in 2019 followed by expansion.

The economics of the mainly underground mine located 80 km from the port of Lae is sweet – gold output will cost a negative $2,600 an ounce while copper would be extracted for just $0.54 a pound. Copper was trading at $3.76 in New York on Friday.

The market has been anticipating great things from Wafi-Golpu. Harmony's 2007 pre-feasibility study showed a 1.3 million oz gold and below 1 million tonnes of copper. This has now grown to contain roughly 12.4 million ounces of gold and 5.4 million tonnes of copper.

Harmony Gold says the site is highly prospective and will embark on a feasibility study next year with a focus on enhancing gold recovery which is pegged at 61% at the moment and a $400 million drilling program. Discussions with local landowners are also ongoing.

Harmony Gold's Australian partners Newcrest's (TSX:NM, ASX:NCM) Lihir gold mine in Papua New Guinea has run into trouble with landowners over compensation and the 600,000 gold oz per year mine had to be briefly shut in August.

The government of PNG has the option to take a 30% stake in the Wafi-Golpu mine at cost.

Chart is from Harmony Gold's presentation to analysts – click here for more on Wafi-Golpu.

http://www.mining.com/harmony-and-newcrests-wafi-golpu-could-grow-to-9-8-billion-project-54152/?utm_source=digest-en-cu-121002&utm_medium=email&utm_campaign=digest

BC government rejects Morrison Lake mine for the salmon

The government of British Columbia has rejected plans for a combined copper-gold mine in the province's north-west due to fears it could threaten salmon populations in the Skeena River.

The Vancouver Sun reports that Environment Minister Terry Lake and Energy Mines and Natural Gas Minister Rich Coleman refused to provide the project with an environmental assessment certificate on the grounds that the project would affect sockeye salmon populations and water quality in Morrison Lake.

Pacific Booker Minerals had proposed the construction of the mine at Morrison Lake in the north-west of British Colombia, 65 kilometers north of Smithers.

The mine would have been situated directly adjacent to the 15-kilometre-long Morrison Lake at the headwaters of the Skeena River, which serves as the second-largest producer of sockeye salmon in the province.

Its facilities would have included processing plants, sewage and waste water management infrastructure, and storage for waste rocks, low-grade ore, tailings and sludge.

Local indigenous groups have heralded the surprise decision and the government's consideration of their interests, with Chief Wilf Adam of the Babine Lake First Nation saying "it's all about the protection of the salmon."

http://www.mining.com/bc-government-rejects-morrison-lake-mine-for-the-salmon-76631/?utm_source=digest-en-cu-121002&utm_medium=email&utm_campaign=digest

BC government rejects Morrison Lake mine for the salmon

The government of British Columbia has rejected plans for a combined copper-gold mine in the province's north-west due to fears it could threaten salmon populations in the Skeena River.

The Vancouver Sun reports that Environment Minister Terry Lake and Energy Mines and Natural Gas Minister Rich Coleman refused to provide the project with an environmental assessment certificate on the grounds that the project would affect sockeye salmon populations and water quality in Morrison Lake.

Pacific Booker Minerals had proposed the construction of the mine at Morrison Lake in the north-west of British Colombia, 65 kilometers north of Smithers.

The mine would have been situated directly adjacent to the 15-kilometre-long Morrison Lake at the headwaters of the Skeena River, which serves as the second-largest producer of sockeye salmon in the province.

Its facilities would have included processing plants, sewage and waste water management infrastructure, and storage for waste rocks, low-grade ore, tailings and sludge.

Local indigenous groups have heralded the surprise decision and the government's consideration of their interests, with Chief Wilf Adam of the Babine Lake First Nation saying "it's all about the protection of the salmon."

http://www.mining.com/bc-government-rejects-morrison-lake-mine-for-the-salmon-76631/?utm_source=digest-en-cu-121002&utm_medium=email&utm_campaign=digest

Western Sierra Mining Corp., (OTC:WSRA) confirmed today (9/24/2012) that it is in the process of re-opening the Azurite mine in the Bradshaw Mountains of Arizona.

The Azurite, formally know as the "Lower Davis Dunkirk" has historically produced gold, silver and copper in varying amounts since the late 1800's. Significant exploration work was expanded in 1980 and Western Sierra acquired the property early in the 3rd quarter of 2012.

The Company will first provide for access improvements reworking existing roads while simultaneously driving new roads intersecting the main vein structures in preparation for surface mining. The Company will also clear the historical mill site of brush and debris.

The initial work has begun and should be completed during the first week in October, 2012

Note: This PR does not mention GDSM nor does it claim GDSM as a JV partner on the Azurite.

Here are some pictures of the mine back in the 1930s!

The mine entrance today.

The Lower Cabin.

Yes it was nice of Mr. Chaffee to send me those pictures so everyone can see the road work that has been done.