News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Those are thieves, ask you for front fee and never materialised, should be in prison.

Global Emerging Markets: GEM is another toxic death spiral funder https://www.gemny.com/team/

Williamsburg Venture Holdings, LLC is a toxic death spiral fund.

Ronald Glenn

Williamsburg Venture Holdings, LLC

395 Leonard Street, Suite 719

Brooklyn, NY 11211

E-mail: rg@williamsburg.ventures

Attention: Ronald Glenn, Managing Member

The SEC filed litigation against Adam Long, LG Capital LLC and Oasis Capital LLC, charging them as unregistered dealers.

https://www.sec.gov/litigation/litreleases/lr-25872

https://www.sec.gov/files/litigation/complaints/2023/comp25872.pdf

This article about the SEC Complaint against Long, L2 and Oasis includes a nice update on ALL of the SEC unregistered dealer cases over the past few years:

https://www.securitieslawyer101.com/2023/sec-charges-adam-r-long-and-his-two-companies-l2-capital-llc-and-oasis-capital-llc-as-unregistered-dealers/

Ionic Ventures Brendan O’Neil is another toxic death spiral funder with promissory notes that convert at a large discount to the lowest price over the prior 2 weeks

AWM Special Situations Fund is another toxic death spiral funder

Alex Silverman is the PM there: https://www.linkedin.com/in/alsilverman/

Can you please PM me I have a question for you, thank you! it's about one of your past posts and my current situation.

Acuitas Capital does toxic convertibles run by Ariel Davis steven wolberg Terren Peizer, this is the reason my MULN stock price is in the dumps

Pacific Lion LLC Jacob Fernane is another toxic funder with floating rate discounts targeting microcaps

https://www.linkedin.com/in/jacobfernane/

Pacific Lion LLC Jacob Fernane is another toxic funder with floating rate discounts focusing on microcaps https://www.linkedin.com/in/jacobfernane/

On June 1, 2023, the Securities and Exchange Commission (the “SEC”) announced charges against Auctus Fund Management, LLC (“Auctus Management”) and its co-owners Alfred Sollami of Brookline, Massachusetts and Louis Posner of Mansfield, Massachusetts, for failing to register as securities dealers with the SEC.

https://www.securitieslawyer101.com/2023/sec-charges-auctus-fund-management-llc-and-its-co-owners-louis-posner-and-alfred-sollami-with-acting-as-unregistered-securities-dealers/

Brenda identified more than 200 issuers that did deals with the Auctus family of companies between 2008 – 2020 (see link for full list). Majority (latter 148) occurred from 2016 – 2021, after Posner and Sollami were no longer registered brokers with FINRA.

Thanks for your updates.

I made you an assistant moderator for this forum.

If you want, you can even start your own section in the ibox to use to make a list of new toxic lenders as they show up.

Walleye Opportunities Master Fund Ltd is another toxic death spiral convertible note funder

Silverback Capital Corporation is another toxic death spiral funder: On March 31, 2022, the Company issued a Promissory Note to Silverback Capital Corporation (“Silverback”) in the amount of $360,000. The Company received $300,000, net of a $60,000 OID. The note bears interest at 8% per annum and matures in one year. Has floating rate conversion price of 20% discount to the five day trailing VWAP of the common stock. On February 21, 2023, Silverback fully converted the $360,000 note and $25,723 of interest into 19,286,137 shares of common stock.

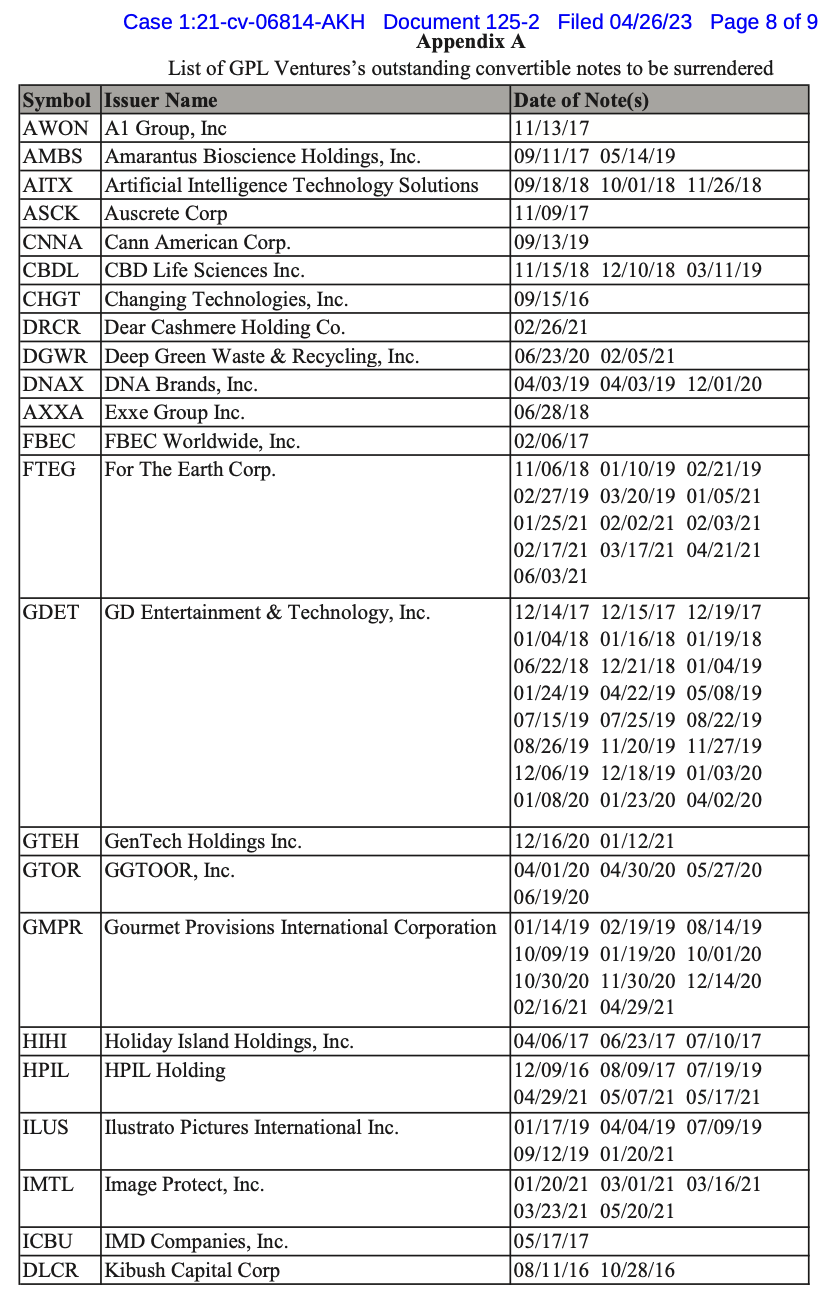

It sounds positive, but scanning that list, I notice a lot of companies are long out of business and their shares no longer trade. I would guess it is likely that is true of most of those notes, which is why GPL was still holding them - they can't be converted and the common shares sold.

Which means the cancellation and/or return of those notes is essentially meaningless.

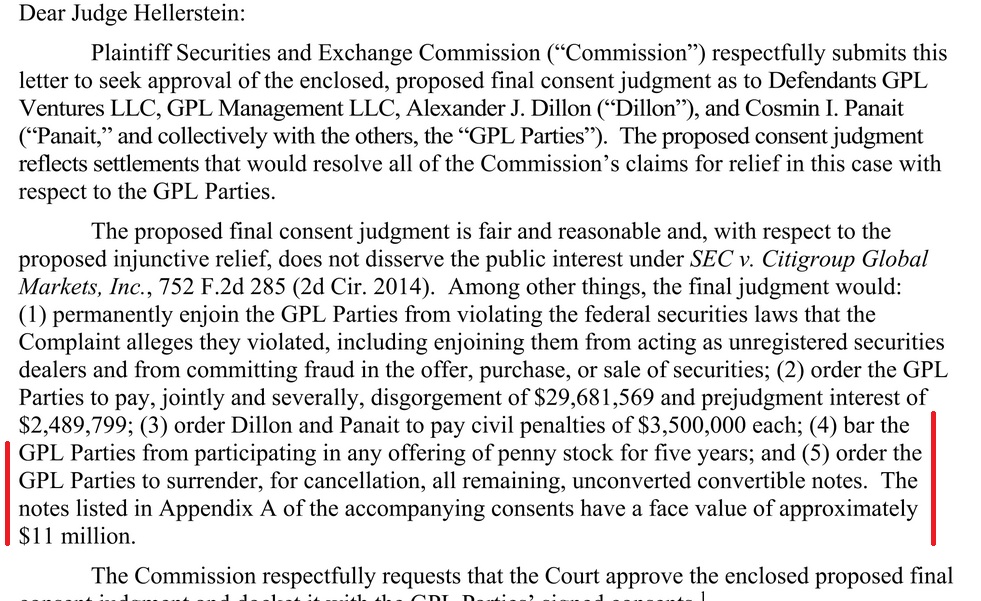

The Judge put 5-year penny stock bars on both Dillon and Panait. That should end GenCap's business.

Why do you keep posting the same thing? There is no point in making duplicate posts. One is enough.

I see your last is slightly different, so I'll leave it. But it would have been better simply to edit the original, if you had time. If not, then you should have written a new post saying its purpose was to add specific things to the original.

GPL Management is now GenCap Management run by both Alexander Dillon and Cosmin Panait from GPL and Blackbridge, so it looks like the 2nd name change they had to do, now on their 3rd fund since the SEC won their case against them and cancelled their investments.

GPLVentures is now GenCap Management run by both Alexander Dillon and Cosmin Panait from GPL and Blackbridge, so it looks like the 2nd name change they had to do, now on their 3rd fund since the SEC prosecuted them and cancelled their investments. Wonder how this 3rd time is going to work out.

Here are the GPL Ventures Notes being cancelled as a result of the settlement:

SEC versus GPL Ventures final settlement agreement approved by a NY court.

There are actually several private law firms that have been suing toxic funders in addition to the SEC actions. They have also been winning, but on a much narrower argument than what it seems OPTI is being sued for. Those other firms have been using New York's usury statutes, successfully arguing that the amounts of the massive discount these lenders use to convert their debt into common shares is covered under usury laws which severely limits the amount of interest and other considerations they can be paid. IIRC, several of the toxic funders have appealled and in each case the ruling against them was upheld. I don't recall the full terms of each judgement, but I remember that, just like in the SEC cases, the funders were required to return or cancel all remaining toxic debt and any unsold converted shares back to the lenders.

Yes, it's a lot...

The 45 bucks was the problem. Thats two twenty-dollar Amazon movies.

.

I would have gotten the complaint but it's 104 pages and 45 bucks.

..

Now that's interesting...

Sueing OPTI now...

$opti derivative shareholder lawsuit pic.twitter.com/rUq2u9pM3k

— Novice Investor (@Optimistic313) December 24, 2022

Waiting 2 years for Fife to be convicted and nothing yet! Did I miss it? WTF! SEC has no case, or the judge is to dumb interpret the laws.

SEC-v-LG CAPITAL FUNDING, LLC, and JOSEPH I. LERMAN,

Defendants, and DANIEL GELLMAN, BORUCH GREENBERG, and

ELI SAFDIEH.

https://www.sec.gov/litigation/complaints/2022/comp25410.pdf

1. From at least January 1, 2016 through at least December 31, 2021 (the “Relevant Period”), LG Capital Funding, LLC (“LG Capital”) and its managing member and 50% owner Joseph I. Lerman (“Lerman”), acted as securities dealers, engaged in the business of buying and selling large volumes of penny stocks for their own account, without being registered as a dealer with the SEC and without Lerman associating with an SEC-registered dealer.

2. LG Capital’s business model – which was carried out under Lerman’s direction and control – involved purchasing convertible promissory notes from penny stock issuers for the exclusive benefit of Lerman and its two other principals, later converting those notes into

unrestricted, newly issued shares of penny stocks at a substantial discount to the then-prevailing market price (typically 35% to 50%), and a quick re-sale of the post-conversion shares into the public markets to capture the benefit of the discount.

3. During the Relevant Period, LG Capital purchased or funded approximately 330 convertible notes of more than 100 different penny stock issuers, the majority repeat customers. It converted at least 150 of the 330 convertible notes into more than 23 billion unrestricted,

newly issued shares of common stock – shares that had never traded publicly until LG Capital introduced them into the public markets.

4. LG Capital’s convertible notes business was lucrative. It generated at least $30 million in gross stock sale proceeds and at least $20 million in profits from its post-conversion sale of shares. Upon information and belief, LG Capital continues to hold unconverted notes and shares derived from converted notes, and is still engaged in the convertible note business today.

5. In practice, LG Capital began to sell post-conversion shares soon after each conversion and derived profits principally from the discounted acquisition price, as opposed to appreciation in the market price of the issuer’s common stock.

6. Lerman at all times controlled and had final authority over LG Capital’s business decisions. His actions committed LG Capital to the initial investments and to the later acquisition and sale of discounted shares. He signed all of the agreements pursuant to which LG Capital

acquired the convertible notes. He signed a majority of the notices that LG Capital used to convert the notes into newly issued, free-trading shares. He controlled LG Capital’s bank accounts and authorized a majority of the funding wires. He controlled LG Capital’s brokerage

accounts and, in connection with a majority of conversions, executed the paperwork needed to deposit the converted shares into LG Capital’s brokerage accounts. He instructed LG Capital’s contract accountant on how to record the transactions in LG Capital’s books and records.

7. By failing to register as securities dealers, and by Lerman’s failure to associate with a registered securities dealer, LG Capital and Lerman avoided the regulatory obligations that govern dealer conduct. Those obligations include submitting to regulatory inspections and oversight, following financial responsibility rules, and maintaining books and records in accordance with applicable regulatory requirements.

8. Relief Defendants Daniel Gellman (“Gellman”), Boruch S. Greenberg

(“Greenberg”), and Eli Safdieh (“Safdieh”) each received a portion of the proceeds of Defendants’ violations, to which they have no legitimate claim.

(25 PAGES TOTAL)

MASTIFF GROUP LLC...toxic?

Owned/ run by attorney Jonathan Leinwand who provides/provided multiple attorney opinion letters for various tickers run/ fronted by Eddie Vakser --currently involved with his AURI which just authorized 10 billion new shares (13bn total).

Reminder (NoDummy)-- https://investorshub.advfn.com/boards/read_msg.aspx?message_id=82762356

ProTek Capital / Luxuriant Holdings Inc. Signs Funding Agreement--

"The commitment by Mastiff LLC is to provide up to $ 5,000,000.00..."

https://sports.yahoo.com/news/protek-capital-luxuriant-holdings-inc-135400901.html

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=98604128

Leinwand represented Eddie Vakser' ARTFEST INTERNATIONAL (ARTS fka ARTI.OB) before the SEC for claiming books were audited when they were not. Vakser again lied to the SEC which permanently revoked ARTS.

See /2016/08/DelaneyBA.pdf

Do you have any info on "Leonite Capital" that you can share?

Looks like they might be getting involved with the shell ticker ILST.

tia

That is an excellent outcome against Crown Bridge Partners.

Copied from your link, nodummy:

August 2, 2022 — The Securities and Exchange Commission (the “SEC”) today announced settled charges against a convertible note dealer, Crown Bridge Partners, LLC, and its managing members, Soheil and Sepas Ahdoot of Great Neck, N.Y., for failing to register with the SEC as securities dealers.

As part of the settlement, the Ahdoots and Crown Bridge agreed to pay more than $9 million in monetary relief and to surrender or cancel securities of 82 different issuers they allegedly obtained from their unregistered dealer activity.

The SEC’s complaint, filed in the federal district court in Manhattan, alleges that, between January 2016 and December 2020, Crown Bridge purchased about 250 convertible notes from 150 microcap issuers, and converted the notes into 35 billion newly issued shares of stock at a large discount from the market price. It then allegedly sold the newly issued shares into the market at a significant profit.

As alleged, neither Crown Bridge nor the Ahdoots were registered as dealers with the SEC or associated with a registered dealer, as their activities required them to do.

“When Crown Bridge and the Ahdoots allegedly failed to register with the SEC, they skirted important regulatory safeguards that support the integrity of our markets by, among other things, subjecting securities dealers to inspections and oversight,” said Mark Cave, Associate Director in the Division of Enforcement. “Today’s action secures comprehensive relief against the defendants – including the surrender or cancellation of securities of dozens of different issuers – and reflects our ongoing commitment to enforcing the registration provisions of the federal securities laws.”

Without admitting or denying the allegations, Crown Bridge and the Ahdoots agreed to be permanently enjoined from further violations of the registration provisions of the Securities Exchange Act of 1934, to pay disgorgement and prejudgment interest of $8,390,601.27 and a civil penalty of $810,307, and to a five-year penny stock bar.

Crown Bridge also agreed to surrender all conversion rights in its currently held convertible notes, surrender all unexercised warrants that it acquired in connection with convertible notes, and cancel any shares it holds that were acquired by converting notes or exercising related warrants.

The settlement is subject to court approval. Finally, Crown Bridge and the Ahdoots consented to the entry of a Commission order imposing a five-year collateral bar to be obtained in a follow-on administrative proceeding.

They got Crown Bridge Partners

https://www.securitieslawyer101.com/2022/sec-charges-convertible-note-dealer-crown-bridge-partners-llc-and-its-managing-members-soheil-and-sepas-ahdoot-for-failure-to-register/

This part is especially interesting:

Crown Bridge also agreed to surrender all conversion rights in its currently held convertible notes, surrender all unexercised warrants that it acquired in connection with convertible notes, and cancel any shares it holds that were acquired by converting notes or exercising related warrants.

And not surprisingly, it's all been downhill for BEGI since April 2021:

Todd was swapping his stock for PIpe deals.

On June 26, 2019, International Hedge Group, Inc. retired 139,831 shares (certificate listed as IHG, Inc.) to treasury simultaneously to the issuance of 139,831 shares issued under the Power Up Lending convertible promissory note.

There were 159,074,757 shares of common stock outstanding, 540,000 warrants issued for common stock, and 1,000,000 Class A Preferred Shares outstanding (owned by International Hedge Group, Inc.) as of March 8, 2022 .

On April 29, 2021 BlackStar Enterprise Group, Inc. and Adar Alef, LLC entered into a convertible promissory note totaling $550,000 and a securities purchase agreement. The Company initially reserved out of its authorized Common Stock 86,105,000 shares of Common Stock for conversion pursuant to the note. The note bears interest at 10%, with a default rate of 24%, and is convertible at the option of the holder, at any time after the date of issuance. The

7

Table of Contents

conversion price is to be calculated at 50% of the average of the three lowest closing bid prices of the Company’s common stock for the previous 20 trading days prior to the date of conversion. The lender agrees to limit the amount of stock received to less than 4.99% of the total outstanding common stock. There are no warrants or options attached to the note. The Company received the net proceeds from the loan of $462,000, after original issue discount, legal fees and offering costs of $88,000. Copies of the promissory note, securities purchase agreement, and transfer agent letter can be found in the Form 10-Q and exhibits filed on May 17, 2021. The Company and the holder executed the securities purchase agreement in accordance with and in reliance upon the exemption from securities registration for offers and sales to accredited investors afforded, inter alia, by Rule 506 under Regulation D as promulgated by the SEC under the 1933 Act, and/or Section 4(a)(2) of the 1933 Act. The company filed a Form D with the Securities and Exchange Commission on June 1, 2021.

No, I didn't. But that's interesting.

Did you see where Adar Bay/ Aryeh Goldstein just did a toxic lending deal with Todd Lahr's old Blackstar scam?

Nice Post. No mention of a contingency to the above funding until its disclosed later, in a 10Q filing below

Quote:

ITEM 5. OTHER INFORMATION

RB Capital Financing

In September of 2020, the Company negotiated a financing transaction with RB Capital Partners, Inc. (“RB Capital”), whereby RB Capital would provide the Company with up to $400,000 in financing. As a condition to the financing, the Company was required to reduce the conversion price of a $31,500 promissory note RB Capital acquired from a third-party down to $0.001 and immediately convert the note into 31,500,000 shares of unrestricted common stock. Such shares were issued on or about October 7, 2020.

https://www.sec.gov/Archives/edgar/data/1119897/000155479520000304/pctl1114form10q.htm

Since the initial conventional Note, PCT has PR'd several subsequent conventional loans from RBC without any contingencies mentioned in the PR, exactly as the initial loan.

PCTL is currently delinquent in their Q1 2021 filing, so no disclosure available of other significantly discounted shares being issued as contingency to subsequent loans.

This is the first of many, I hope!! They ought to look into the social media and public forum presences during the time leading up to said conversions and sales. Would be interesting to note any unusual social media/stock forum activity surrounding the times of said conversions, and then again at time of sales. I believe influencers were infact hired to manipulate public perspective. Both down for conversions, and then back up for sale.

Lets clean these streets! This is a big one.

SEC Sues New York Based Firm and Its Managing Member for Acting as Unregistered Securities Dealers

Litigation Release No. 25410 / June 7, 2022

Securities and Exchange Commission v. LG Capital Funding, LLC., and Joseph I. Lerman, et. al, 1:22-cv-03353 (E.D.N.Y. filed June 7, 2022)

The Securities and Exchange Commission today announced charges against LG Capital Funding, LLC ("LG Capital") and its managing member Joseph Lerman of Brooklyn, New York, for failing to register as securities dealers with the SEC. LG Capital and Lerman allegedly bought and sold billions of newly-issued shares of microcap securities, or "penny stocks," which generated millions of dollars for LG Capital and Lerman.

The SEC's complaint, filed in the Eastern District of New York, alleges that between at least January 2016 and December 2021, LG Capital engaged in the business of purchasing convertible notes from penny stock issuers, converting the notes into shares of stock at a large discount from the market price, and selling those newly issued shares into the market at a significant profit. LG Capital allegedly purchased over 300 convertible notes from more than 100 separate issuers and sold more than 22 billion shares of newly issued penny stock into the market, generating sales proceeds of approximately $30 million and net profits of approximately $20 million. As alleged, neither LG Capital nor Lerman were registered as a dealer with the SEC or associated with a registered dealer, in violation of the mandatory registration provisions of the federal securities laws. By failing to register, LG Capital and Lerman avoided certain regulatory obligations for dealers that govern their conduct in the marketplace, including regulatory inspections and oversight, financial responsibility requirements, and maintaining books and records.

The SEC's complaint charges LG Capital and Lerman with violating the registration provision of Section 15(a)(1) of the Securities Exchange Act of 1934, and charges Lerman with violating Section 20(a) of the Securities Exchange Act of 1934. The SEC seeks a permanent injunction, disgorgement of ill-gotten gains plus prejudgment interest, a civil penalty, a penny stock bar, and other equitable relief. The complaint also names as relief defendants LG Capital's two other members, Daniel Gellman and Boruch Greenberg, and LG Capital's primary employee, Eli Safdieh, who all allegedly received illicit proceeds from LG Capital and Lerman's violations.

The SEC's investigation was conducted by Elliot Weingarten, assisted by Suzanne Romajas and Robert Nesbitt, and supervised by Fuad Rana and Carolyn M. Welshhans. The litigation will be led by Suzanne Romajas and Elliot Weingarten, and supervised by Melissa Armstrong.

——-

https://www.sec.gov/litigation/complaints/2022/comp25410.pdf

I suspect more contingency shares have been issued - again

Additional RB Capital activity with PCTL (PCT Ltd)

Here PCT makes a PR in receipt of a conventional convertible note, convertible well above current market prices. No ratchet, no funny business.

Quote:

PCT LTD (OTC Pink: PCTL) today announced that it has received $400,000 in funding from California based RB Capital Partners, Inc. ("RB Capital"). RB Capital has provided funding to the Company in the form of two 12-month premium-to-market convertible notes. The notes accrue interest at 5% per annum, are convertible at a rate of $0.20 per share and do not include any ratchet clauses or warrant coverage. The entire $400,000 investment has been received by the Company as of October 16, 2020.

https://finance.yahoo.com/news/pct-ltd-pctl-received-400-120000097.html

No mention of a contingency to the above funding until its disclosed later, in a 10Q filing below

Quote:

ITEM 5. OTHER INFORMATION

RB Capital Financing

In September of 2020, the Company negotiated a financing transaction with RB Capital Partners, Inc. (“RB Capital”), whereby RB Capital would provide the Company with up to $400,000 in financing. As a condition to the financing, the Company was required to reduce the conversion price of a $31,500 promissory note RB Capital acquired from a third-party down to $0.001 and immediately convert the note into 31,500,000 shares of unrestricted common stock. Such shares were issued on or about October 7, 2020.

https://www.sec.gov/Archives/edgar/data/1119897/000155479520000304/pctl1114form10q.htm

Since the initial conventional Note, PCT has PR'd several subsequent conventional loans from RBC without any contingencies mentioned in the PR, exactly as the initial loan.

PCTL is currently delinquent in their Q1 2021 filing, so no disclosure available of other significantly discounted shares being issued as contingency to subsequent loans.

BR has been chatting it up on Twitter about PCTL as well

Lastly, a few Fridays ago PCTL traded in excess of 200m shares, a massive leap in its usual trading activity coinciding with some oil enhancement testing PR theyve been conducting. Of course, the spike in share price to .032 lasted less than 1 day and now its back to sub 2 cents

Murphy from Labrys Fund has a new one called Mast Hill Fund L.P.

https://www.sec.gov/Archives/edgar/data/0001880237/000188023721000001/xslFormDX01/primary_doc.xml

a deal with the devil:

Check out his disclaimer lol

Company has performed due diligence and background research on Investor and its affiliates including, without limitation, John M. Fife, and, to its satisfaction, has made inquiries with respect to all matters Company may consider relevant to the undertakings and relationships contemplated by the Transaction Documents including, among other things, the following: http://investing.businessweek.com/research/stocks/people/person.asp?personId ###-###-####&ticker=UAHC;SEC Civil Case No. 07-C-0347 (N.D. Ill.); SEC Civil Action No. 07-CV-347 (N.D. Ill.); and FINRA Case #2011029203701. In addition, Investor is involved in ongoing litigation with the SEC regarding broker-dealer registration (see SEC Civil Case No. 1:20-cv-05227 (N.D. Ill.)). Company, being aware of the matters described in subsection (xvi) above, acknowledges and agrees that such matters, or any similar matters, have no bearing on the transactions contemplated by the Transaction Documents and covenants and agrees it will not use any such information as a defense to performance of its obligations under the Transaction Documents or in any attempt to avoid, modify, offset or reduce such obligations.

Down Goes Keener!

The SEC wins summary judgment against toxic convertible note lender #justinkeener. This SEC win demonstrates that the courts are recognizing that purveyors of convertible notes, funders that purchase convertible notes from OTC Mark…https://t.co/vBhtlgWtTj https://t.co/2AxZDpDlyu

— Securities Attorneys (@TBLF_LawFirm) January 24, 2022

$PCTL VS AUCTUS FUND https://www.pacermonitor.com/public/case/43256345/PCT,_Ltd_v_Auctus_Fund_LLC

Fife Streeterville just funded $15 million to SHMP, a toxic nightmare even before Fife

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |