News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

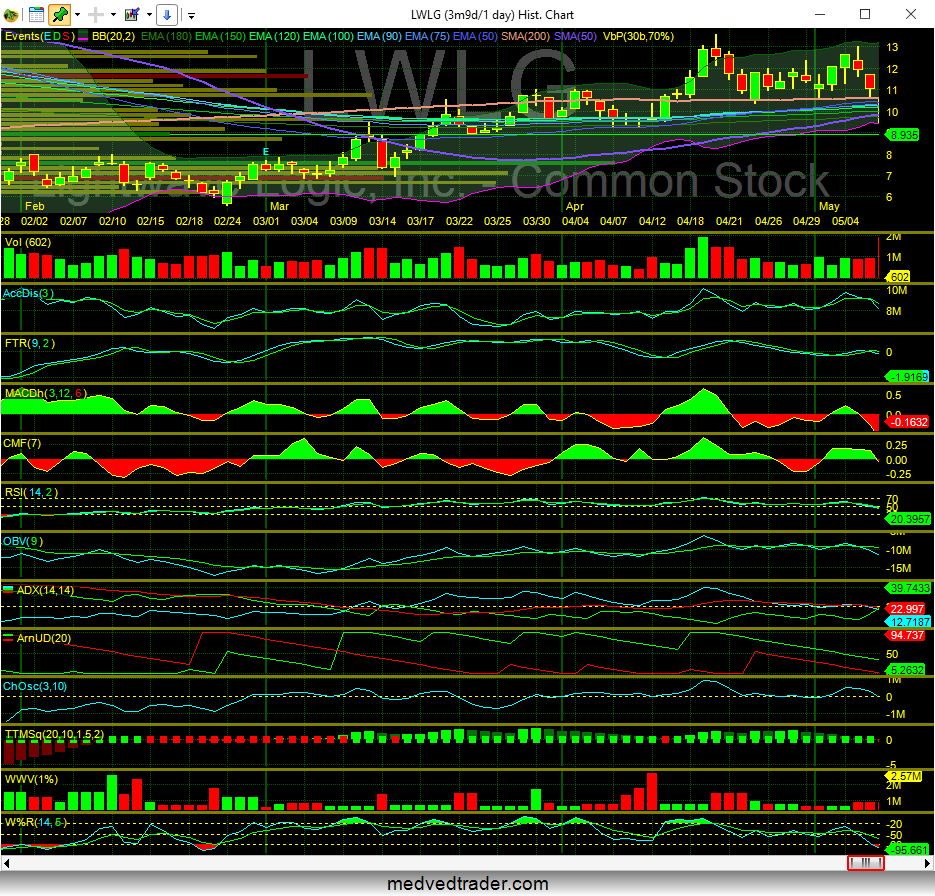

BMAS -

On November 4, 2015, the U.S. Attorney for the Eastern District of New York announced that Darren Ofsink, a Manhattan attorney and founder of Ofsink LLC; Michael Morris, a registered broker and managing director of Halcyon Cabot Partners, Ltd. (Halcyon); and Darren Goodrich, a registered broker for fourteen years at BMA Securities, a firm controlled by Burt Martin Arnold were arrested earlier today on charges of securities fraud, wire fraud, and conspiracy to commit securities fraud, mail fraud, and wire fraud in connection with a $300 million market manipulation scheme. In addition to the three defendants arrested today, the eleven-count superseding indictment unsealed this morning charges four additional defendants who were arrested in July 20

14: Abraxas J. Discala, also known as “AJ Discala,” the Chief Executive Officer of OmniView Capital Advisors LLC; Ira Shapiro, the Chief Executive Officer of CodeSmart Holdings, Inc., a publicly traded company; and Craig Josephberg, a registered broker. Three defendants, Marc Wexler, Matthew Bell, and Victor Azrak, who were charged in the underlying indictment, have pleaded guilty and are awaiting sentencing.

Ofsink and Morris will be arraigned later today. Darren Goodrich’s initial appearance for removal proceedings to the Eastern District of New York is scheduled for this afternoon at the United States Courthouse, 312 North Spring Street, Los Angeles, California. Discala, Shapiro and Josephberg will be arraigned on the superseding indictment at a later date.

A couple of GameStop articles that deal with NSS and share registration:

https://www.nasdaq.com/articles/all-about-failing-trades-2021-04-08

https://www.thestreet.com/memestocks/gme/gamestop-investors-are-turning-to-direct-registration-why-that-could-be-a-good-idea

On the significance and mechanics of FTD:

https://www.nasdaq.com/articles/all-about-failing-trades-2021-04-08

I don't think those stats are available but comparing short interest to VBP should give some clues.

In edit = 5/13 to 6/30 seems to be where most of the damage was done, days to cover have tripled since then.

Order of data:

Settlement Date/Short Interest/Percent Change/ Average Daily Share Volume/Days to Cover

01/31/2022 8,224,272 67.06 1,996,611 4.12

01/14/2022 4,922,847 9.97 1,113,918 4.42

12/31/2021 4,476,575 102.34 1,842,236 2.43

12/15/2021 2,212,448 28.67 1,649,231 1.34

11/30/2021 1,719,480 (5.48) 944,571 1.82

11/15/2021 1,819,143 (5.38) 715,036 2.54

10/29/2021 1,922,613 (9.60) 403,339 4.77

10/15/2021 2,126,831 38.81 477,119 4.40

04/29/2022 14,881,642 12.40 1,063,592 13.99

04/14/2022 13,239,579 3.50 678,095 19.52

03/31/2022 12,791,395 10.45 875,640 14.61

03/15/2022 11,580,686 5.05 890,355 13.01

02/28/2022 11,023,861 4.63 872,453 12.64

02/15/2022 10,536,146 28.11 977,195 10.78

06/30/2022 20,807,845 6.79 2,426,677 8.57

06/15/2022 19,485,684 10.05 1,865,235 10.45

05/31/2022 17,706,834 9.34 1,427,860 12.40

05/13/2022 16,194,010 8.82 1,715,225 9.40

You have three types of short sale numbers..

1) The quantity of shorted shares traded each day.

https://www.finra.org/finra-data/browse-catalog/short-sale-volume-data

Which probably correlates with dark pool activity:

https://chartexchange.com/symbol/nasdaq-lwlg/exchange-volume/

2) The number of short shares in circulation that have been reported which would of course not include NSS:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=170921173

Discussion of short interest with charts below. Over the weekend I will try to revive my DBXL skills and do some analysis of the data item 1, correlating it with the chart:

https://investorshub.advfn.com/boards/replies.aspx?msg=170799662

3) FTD data:

https://www.sec.gov/data/foiadocsfailsdatahtm

Institutional interest and control is increasing because of market wide manipulation - STUDY:

GFS owned Mubadala Investment Co PJSC 88 per cent

GameStop is a red herring IMO...

I strongly suspect that the Reddit thing was used as cover for a pump and dump setup in the general market. I also believe that BlackRock was a key player.

Why First Majestic Silver, Hecla Mining, and Other Silver Stocks Rallied out of the Gate Today

JAN 29, 2021 12:48PM EST

Uncertainty is definitely high right now, with all the hype surrounding GameStop, AMC Entertainment, and other names caught up in short squeezes. The CBOE Volatility Index (or VIX for short), which specifically measures investors' expectations of market volatility, is clearly spiking, as the chart above shows. In fact, it isn't at all shocking that investors would view the short squeeze feeding frenzy as a sign that the market has become frothy. After all, stocks are near all-time highs, and the short squeeze issue has caught the attention of the mainstream media and even some prominent politicians. With that background, buying some silver and gold to protect against downside risk makes logical sense.

https://www.nasdaq.com/articles/why-first-majestic-silver-hecla-mining-and-other-silver-stocks-rallied-out-of-the-gate

First Majestic Silver Says It’s Unaware Of Reason For Share Gain

JAN 29, 2021 1:29AM EST

Shares of First Majestic Silver popped by 13% in Thursday's extended market session after closing 22% higher on the day. The stock has gained about 67% over the past three months.

https://www.nasdaq.com/articles/first-majestic-silver-says-its-unaware-of-reason-for-share-gain-2021-01-29

The Next GameStop: Silver Bullion?

JAN 29, 2021 5:44PM EST

Data source: Yahoo! Finance.

The entire investing community has been fixated on what's been happening with shares of stocks that have high short interest. GameStop (NYSE: GME) and others have seen their share prices gyrate wildly, and at least in some people's eyes, it's turned into a battle between Wall Street and average investors. With some brokers having temporarily suspended trading in GameStop on Thursday, some investors are looking for other areas where short squeezes might occur. Even as many of those brokers allowed investors to buy GameStop stock again on Friday, some looked instead to silver stocks -- and the precious metal itself -- as possibilities for a similar short squeeze.

https://www.nasdaq.com/articles/the-next-gamestop%3A-silver-bullion-2021-01-29

courtesy of that for profit site .. ;) Share Structure Share Structure

and why NR (non retail) has a such a dilemma with

P2O's first sale/s' funds' conveyed

security details .. for comparison re: 2 OTC targets PTOI & IPIX and 2020 YTD *Volume* ..

note *Shareholders of Record & what is held via DTC*

IPIX YTD thru EO Nov 2020 ~ 576,394,226

IPIX SECURITY DETAILS

Market Cap Market Cap

70,289,578

12/28/2020

Authorized Shares

600,000,000

11/30/2020

Outstanding Shares

357,616,780

11/30/2020

Restricted

14,505,340

11/30/2020

Unrestricted

343,111,440

11/30/2020

Held at DTC

341,561,335

11/30/2020

Float

302,360,872

06/30/2020

Par Value

0.0001

Shareholders

Shareholders of Record 68

PTOI YTD thru EO Nov 2020 ~ 11,651,243

PTOI SECURITY DETAILS

Market Cap Market Cap

3,393,367

12/29/2020

Authorized Shares

250,000,000

12/29/2020

Outstanding Shares

124,756,158

12/29/2020

Restricted

31,893,743

12/29/2020

Unrestricted

92,862,415

12/29/2020

Held at DTC

87,509,624

12/29/2020

Float

90,809,215

05/30/2018

Par Value

0.001

Shareholders

Shareholders of Record 478

Total shares authorized: 250,000,000 as of date: 12/14/20

Total shares outstanding: 124,756,158 as of date: 12/14/20

Number of shares in the Public Float(2): 90,809,215 as of date: 12/14/20

Total number of shareholders of record: 478 as of date 12/14/20

SOR is a Shareholder of record---SOR are those entities that hold shares in certificate form or are registered on the companie's register thru the Transfer Agent...if your shares are held in a brokerage account, CEDE is the nominee SOR of your shares of which you are the beneficial owner...

the DTCC holds, clears, and settles trades electronically---see subsidiaries here for DTC and CEDE

https://en.wikipedia.org/wiki/Depository_Trust_%26_Clearing_Corporation

BMA was involved in the GOSY IPO.

UBS is using Dominion to generate fake locates and borrows...

Wonder who else is using this software to generate air shares???

Tic Toc

https://mb.ntd.com/400-million-sec-filing-links-dominion-ubs-and-china_536295.html

ever notice how the SEC goes for the low hanging fruit

years after the fact ..

BMA Fails to Close Out FTDs BMA’s Clearing Firm Properly Allocated to BMA

7. From January 2015 through at least August 2016, BMA’s clearing firm (the

“Clearing Firm”) reasonably allocated FTDs to BMA. BMA was responsible for closing out such

FTDs, per Rule 204.

8. In many instances, BMA simply ignored the allocated FTDs, and took no steps

whatsoever to close out those FTDs.

PTOI ~ Volume October 2020

interesting to see where NN *reported* to Finra

in NRs' giant *shell* game re: PTOI

6 out of 6 .. behind the *re-activated* ARCA (July 2020)

note the %s for NRs' washed efforts of 42%~ (first 3)

PTOI 866,511 1,032,195 10,479,789 CDEL 364,953 1 42.12%

PTOI 866,511 1,032,195 10,479,789 GTSM 223,413 2 25.78%

PTOI 866,511 1,032,195 10,479,789 ETRF 141,110 3 16.28%

PTOI 866,511 1,032,195 10,479,789 CSTI 82,262 4 9.49%

PTOI 866,511 1,032,195 10,479,789 ARCA 37,774 5 4.36%

PTOI 866,511 1,032,195 10,479,789 NITE 16,999 6 1.96%

https://otce.finra.org/otce/marketStatistics/monthlyShareVolume

back half (rough) ~ 301,607 .. of which known P2O investors picked off approx 200k (66%)

(haven't had the time to do % for back half of the month re: investors' buys)

PTOI ~ October 2020 Volume

10/30/2020 $0.019 2,375 $0.017 $0.019 $0.017

10/29/2020 $0.0209 N/A $0.0209 $0.0209 $0.0209

10/28/2020 $0.0209 2,735 $0.0209 $0.0209 $0.0209

10/27/2020 $0.016 116,534 $0.018 $0.0209 $0.016

10/26/2020 $0.019 11,520 $0.0209 $0.0209 $0.0187

10/23/2020 $0.0162 12,770 $0.021 $0.021 $0.0162

10/22/2020 $0.0172 34,868 $0.0164 $0.0187 $0.0164

10/21/2020 $0.0186 30,200 $0.0164 $0.0186 $0.0162

10/20/2020 $0.0161 5,000 $0.0185 $0.0185 $0.0161

10/19/2020 $0.0153 58,605 $0.02 $0.02 $0.0153

10/16/2020 $0.0181 27,000 $0.021 $0.021 $0.0151

10/15/2020 $0.015 299,684 $0.0162 $0.0162 $0.015

10/14/2020 $0.021 2,700 $0.021 $0.021 $0.021

10/13/2020 $0.0162 10,732 $0.016 $0.0162 $0.016

10/12/2020 $0.0161 53,817 $0.0209 $0.021 $0.016

10/09/2020 $0.016 8,200 $0.0209 $0.0209 $0.016

10/08/2020 $0.015 18,357 $0.015 $0.015 $0.015

10/07/2020 $0.015 30,600 $0.016 $0.021 $0.015

10/06/2020 $0.016 2,051 $0.021 $0.021 $0.016

10/05/2020 $0.0212 3,333 $0.0212 $0.0212 $0.0212

10/02/2020 $0.0204 111,450 $0.016 $0.025 $0.016

10/01/2020 $0.022 23,979 $0.016 $0.022 $0.016

Historical Short Volume Data for PTOI

Date Close High Low Volume Sht Vol % of Vol Shtd

Oct 29 NA NA NA 1 1 100.00%

Oct 28 NA NA NA 2,735 2,735 100.00%

Oct 27 NA NA NA 116,534 48,651 41.75%

Oct 23 NA NA NA 12,770 6,700 52.47%

Oct 21 NA NA NA 30,200 13,700 45.36%

Oct 20 NA NA NA 5,000 5,000 100.00%

Oct 19 NA NA NA 58,605 4,500 7.68%

Oct 16 NA NA NA 27,000 6,000 22.22%

Oct 15 NA NA NA 299,684 156,484 52.22%

Oct 13 NA NA NA 10,732 10,732 100.00%

Oct 12 NA NA NA 53,817 13,817 25.67%

Oct 07 NA NA NA 30,600 17,501 57.19%

Oct 06 NA NA NA 2,051 1,750 85.32%

Oct 02 NA NA NA 111,450 99,000 88.83%

Oct 01 NA NA NA 23,979 14,813 61.77%

*confirmation* via Finra makes PTOI's October 2020's *volume* of 866,511 the 2nd lowest for 2020 .. hmmm

OCT 2020 ~ 866,511

SEP 2020 ~ 1,032,195

AUG 2020 ~ 917,618

JUL 2020 ~ 1,025,276

JUN 2020 ~ 1,052,205

MAY 2020 ~ 600,356

APR 2020 ~ 1,561,699

MAR 2020 ~ 1,066,784

FEB 2020 ~ 993,682

JAN 2020 ~ 1,363,463

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=159243723

NR (non retail) = just a few probs

4kids

PTOI ~ (rough) October 2020 *volume*

CEs' reported data for October to Finra .. due out *shortly*

https://otce.finra.org/otce/marketStatistics/monthlyShareVolume

back half (rough) ~ 301,607 .. of which known P2O investors picked off approx 200k (66%)

first half (rough) ~ 564,903

PTOI ~ October 2020 *volume* (rough) = 866,510

10/30/2020 $0.019 2,375 $0.017 $0.019 $0.017

10/29/2020 $0.0209 N/A $0.0209 $0.0209 $0.0209

10/28/2020 $0.0209 2,735 $0.0209 $0.0209 $0.0209

10/27/2020 $0.016 116,534 $0.018 $0.0209 $0.016

10/26/2020 $0.019 11,520 $0.0209 $0.0209 $0.0187

10/23/2020 $0.0162 12,770 $0.021 $0.021 $0.0162

10/22/2020 $0.0172 34,868 $0.0164 $0.0187 $0.0164

10/21/2020 $0.0186 30,200 $0.0164 $0.0186 $0.0162

10/20/2020 $0.0161 5,000 $0.0185 $0.0185 $0.0161

10/19/2020 $0.0153 58,605 $0.02 $0.02 $0.0153

10/16/2020 $0.0181 27,000 $0.021 $0.021 $0.0151

10/15/2020 $0.015 299,684 $0.0162 $0.0162 $0.015

10/14/2020 $0.021 2,700 $0.021 $0.021 $0.021

10/13/2020 $0.0162 10,732 $0.016 $0.0162 $0.016

10/12/2020 $0.0161 53,817 $0.0209 $0.021 $0.016

10/09/2020 $0.016 8,200 $0.0209 $0.0209 $0.016

10/08/2020 $0.015 18,357 $0.015 $0.015 $0.015

10/07/2020 $0.015 30,600 $0.016 $0.021 $0.015

10/06/2020 $0.016 2,051 $0.021 $0.021 $0.016

10/05/2020 $0.0212 3,333 $0.0212 $0.0212 $0.0212

10/02/2020 $0.0204 111,450 $0.016 $0.025 $0.016

10/01/2020 $0.022 23,979 $0.016 $0.022 $0.016

Historical Short Volume Data for PTOI

Date Close High Low Volume Sht Vol % of Vol Shtd

Oct 29 NA NA NA 1 1 100.00%

Oct 28 NA NA NA 2,735 2,735 100.00%

Oct 27 NA NA NA 116,534 48,651 41.75%

Oct 23 NA NA NA 12,770 6,700 52.47%

Oct 21 NA NA NA 30,200 13,700 45.36%

Oct 20 NA NA NA 5,000 5,000 100.00%

Oct 19 NA NA NA 58,605 4,500 7.68%

Oct 16 NA NA NA 27,000 6,000 22.22%

Oct 15 NA NA NA 299,684 156,484 52.22%

Oct 13 NA NA NA 10,732 10,732 100.00%

Oct 12 NA NA NA 53,817 13,817 25.67%

Oct 07 NA NA NA 30,600 17,501 57.19%

Oct 06 NA NA NA 2,051 1,750 85.32%

Oct 02 NA NA NA 111,450 99,000 88.83%

Oct 01 NA NA NA 23,979 14,813 61.77%

with *confirmation* (FINRA) .. that would make PTOI's October 2020's *volume* of 866,510 the 2nd lowest for 2020 .. hmmm

SEP 2020 ~ 1,032,195

AUG 2020 ~ 917,618

JUL 2020 ~ 1,025,276

JUN 2020 ~ 1,052,205

MAY 2020 ~ 600,356

APR 2020 ~ 1,561,699

MAR 2020 ~ 1,066,784

FEB 2020 ~ 993,682

JAN 2020 ~ 1,363,463

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=159243723

NR (non retail) = just a few probs

4kids

PTOI ~ Volume by Month ~ 2020

PTOI ~ YTD Volume @ EO September 2020 = 9,613,278

SEP 2020 ~ 1,032,195

AUG 2020 ~ 917,618

JUL 2020 ~ 1,025,276

JUN 2020 ~ 1,052,205

MAY 2020 ~ 600,356

APR 2020 ~ 1,561,699

MAR 2020 ~ 1,066,784

FEB 2020 ~ 993,682

JAN 2020 ~ 1,363,463

PTOI ~ Volume by Month ~ 2019

PTOI ~ YTD Volume ~ 2019 = 23,994,633

PTOI ~ YTD Volume @ EO September 2019 = 11,515,439

JAN 2019 ~ 1,651,632 .. 604,990 sans 1.29.19's *volume*

FEB 2019 ~ 2,076,767 .. note 2M + 400k = 2.4M~

MAR 2019 ~ 1,612,549 .. note 1.6M identical to Jan 2019 (washed effort)

APR 2019 ~ 2,499,579 .. note 2.4M - 400k = 2M

MAY 2019 ~ 858,637 .. 2019 YTD Volume ~ 8,699,164

JUN 2019 ~ 491,063 .. 2019 YTD Volume ~ 9,190,227

JUL 2019 ~ 445,451 .. lowest volume month in 2019 .. 2019 YTD Volume ~ 9,635,678

AUG 2019 ~ 772,572 .. 2019 YTD Volume ~ 10,408,250

SEP 2019 ~ 1,107,189 .. 2019 YTD Volume ~ 11,515,439

OCT 2019 ~ 2,189,307 .. 2019 YTD Volume ~ 13,704,746

NOV 2019 ~ 8,847,829 .. *record* vol by NR breaks April 2011's *efforts/set up*

DEC 2019 ~ 1,442,058 .. 2019 YTD Volume ~ 23,994,633

PTOI ~ Annual Volume Totals: April 2009 - September 2020

2009 ~ 7,188,642 ** (mid April start)

2010 ~ 20,478,838 ** CSTI imported/first hit piece & complicit *letter* of 9/28/2010

2011 ~ 37,204,277 ** NON RETAILs' *set up* .. (includes April's record setting *volume* month of 8M~)

2012 ~ 26,989,328 ** aromatics & mgmt change out May 2012 .. set up for Jan 2013

2013 ~ 36,808,995. ** P2O wrested back mid August 2013 .. wash trading 101 with 2014

2014 ~ 36,381,060 ** wash trading 101 with 2013 .. note lower than 2013 and Jan 2014 6c reset and *volume*

2015 ~ 22,275,997 ** note *volume* significantly lower than 2014 .. PPS relentlessly compressed

2016 ~ 19,759,799 ** note still the lowest YTD volume for PTOI with lowest PPS

2017 ~ 13,540,583 ** down approx 6M and change from 2016's record setting low *volume*

2018 ~ 13,924,427 .. slight increase over 2017's 13M~ *volume* .. first turn since 2013

2019 ~ 23,994,633 ** includes November 2019's *record volume* of 8,847,829 surpassing NRs' effort of April 2011 *

2020 ~ 9,613,278 @ the EO September **

* April 2011 .. PPS range 80c to 3.00$ (8M~ x $2.00 = $16M)

** November 2019 .. PPS range 2c to 11c (8M~ x $.06c = $480,000)

from memory .. with receipts available

01.31.13 .. NRs' last illegal orchestration of significance $1.49/622k *volume*

09.30.13 .. CEO injects $2M (PPS 35c)

12.31.13 .. PPS *reset* 52 week low 10c

01.13.14 .. PPS *reset* 52 week low 06c

10.13.14 .. PPS *reset* 52 week low 05c memorable due to last aromatic flushed by burying ACC release on *volume*

so for 6 years and 1 month PTOI's PPS has been mostly held @ sub 5c

PTOI's I/O for the past 5 years~ 124,756,158

As of May 15, 2015, there were 121,246,158 shares of the Registrant’s common stock, $0.001 par value, outstanding.

https://www.sec.gov/Archives/edgar/data/1381105/000149315215002006/form10-q.htm

As of November 14, 2014, there were 116,861,535 shares of Common Stock, $0.001 par value per share, issued and outstanding.

https://www.sec.gov/Archives/edgar/data/1381105/000126493114000474/plastic2oil10q.htm

and in the last year .. holders increased from 450 to 478

Approximate number of holders of record as of the certification or notice date: 478

https://www.sec.gov/Archives/edgar/data/1381105/000149315220019558/form15-12ga.htm

and courtesy of that for profit site (with all that that implies)

PTOI Share Structure

Market Cap Market Cap

2,364,129

10/30/2020

Authorized Shares

250,000,000

10/30/2020

Outstanding Shares

124,756,158

10/30/2020

Restricted

31,893,743

10/30/2020

Unrestricted

92,862,415

10/30/2020

Held at DTC

87,509,624

10/30/2020

Float

90,809,215

05/30/2018

NR (non retail) has 10 years and 100 MILLION *reasons* for wanting P2O *to fail*

4kids

IPIX ..

If you look at the summary at the end of the 4kids post ... some of the numbers and events jump off the page.

2015 – IPIX SP begins year at $3.66 after peaking at $4.93 in December 2014

8/6/15 Mako hit piece immediately followed by bogus Rosen Class Action

2016 – IPIX SP begins year at $1.28

2017 – IPIX SP begins the year at $1.16 and closes year end at .73

2018 - 88M shares traded

-A then record amount of 55M or about 63% of the entire year total was traded in the last 4 months which was needed to compress IPIX SP from .53 to .07

2019 – 124M (almost a 50% increase in volume from 2018)

- May 2019 alone was 23M to negate the Alfasigma announcement

- YTD through October was 94M and 30M in the last 3 months to compress further down to .05 SP. NR had successfully crippled IPIX down to 5 cents a share making capital extremely expensive and dilutive for any science advancement.

2020 – A successful Phase 1 on B-IBD UC using BDD delivery system gives hope of a future licensing deal into a huge IBD market but then…….A worldwide pandemic strikes that no one saw coming INCLUDING the criminal cabal (also referred to as Non Retail or NR). An even bigger surprise is that our little baby bio investment IPIX’s Brilacidin, turns out to have far superior antiviral capabilities versus ANY other drug known to mankind against the CV19 virus and it not only reduces the overall viral load but kills the CV19 virus on contact, reduces inflammation and modulates the human immune response. Now back to the numbers!

2020 first 9 month volume is 524M. Note at this rate IPIX volume will be 699M in 2020 or ALMOST 6 TIMES THE VOLUME OF 2019. I personally believe that the last 10 weeks of volume in 2020 will be far greater than this rate due to milestone achievements discussed below.

Note that September of 2019 IPIX shareholders voted 90% in FAVOR of approving an increase in Authorized Shares from 300M to 600M. IMO this was an extremely strong vote of confidence that a vast majority of IPIX shareholders were in for the LONG haul. This shareholder confidence in IPIX science and management made it clear that very few IPIX investors were selling any of their position at these artificially compressed prices and by knowing what the own would not be selling under a several dollar SP. The criminals/NR know this very well and thus the comment that they are between a rock and a hard place.

A couple of examples of criminally compressed stocks that saw a sudden increase as NR lost control of SP and their naked position was forced into a squeeze.

- AMRN SP went from $3 to $26 in a very short period of time.

- OSTK SP was $2.23 this March and hit a peak of $123.00 this August. Does anyone on this board believe OSTK improved their business model by a factor of 55X over a brief few month period?

The entire contents above are simply proof points of criminal manipulation by NR but IMO IPIX will ultimately be valued based on their science making it through FDA trials and ultimately distributed successfully to the market to treat disease. My track record on predicting timing of events has not been great as I continue to be surprised at how long it takes to advance the science through FDA trials but with that said I believe we are getting very close to hitting some very huge milestones that will continue to de-risk our investment and bring life-saving drugs to the market. I am expecting to see:

In 30 days or less – FDA IND Approval and separately a Preprint of the RBL Peer Review paper.

In 45 days or less – Initiation of B-CV19 Human Trials

In 60-90 days – Interim Human Trial Results, Emergency Use and Compassionate Use approval. Major industry and investor exposure. Multiple media exposure in print, social media, television, radio discussing the treatment that kills CV19.

1stH 2021 – Large government order and/or government grant for volume shipment of Brilacidin for the masses in parallel with a Phase3 B-CV19 trial. International distribution partnership for B-CV19 to cover non-US demand. Separately a B-IBD UC Phase 2 trial kicks off as Brilacidin is further positioned as a franchise drug used for many different instances.

2ndH 2021 – IPIX will most likely have been already Up Listed off of the criminally controlled OTX to a legitimate exchange. Throughout 2021 the criminals will be scrambling to cover their naked position as an EPIC SHORT SQUEEZE takes place starting in the $2-4/share range but really kicking in the $5-$20 range. Remember that the criminals need REAL LONGS to sell REAL SHARES for them to cover their naked positions. IMO it will not be uncommon to see trading days where IPIX is trading at 10M+ shares daily and go up in $1 plus increments on days where no announcements are made. See the above OSTK example for both the magnitude of the SP increase and the short period of time that this could take place.

=====

the above post was written by another Innovation Pharma investor

who incorporated some of my *data* re: IPIX/CTIX .. publicly posted over the years *here and there*

courtesy of that for profit site (with all that that implies)

IPIX SECURITY DETAILS

Share Structure

Market Cap Market Cap

72,275,663

10/16/2020

Authorized Shares

600,000,000

09/30/2020

Outstanding Shares

349,579,992

09/30/2020

Restricted

14,468,552

09/30/2020

Unrestricted

335,111,440

09/30/2020

Held at DTC

333,561,335

09/30/2020

Float

302,360,872

06/30/2020

Par Value

0.0001

Market Value calculated only for respective security

Transfer Agent

West Coast Stock Transfer Inc.

Shareholders

Shareholders of Record 68

06/30/2020

quotes from this very venue (PTOI) .. re: *authoritative expertise* on the very subject of the DTC (CEDE) .. ;)

On April 7, 2017, there were 482 holders of record of our common stock, $0.001 par value per share.

Well, 481 who were crazy enough to give them their name and all the others with street name are in CEDE.

every public company has a shareholder of record named CEDE that counts as 1 in the # of shareholders of record...that "entity" is the nominee owner of all shares held by all beneficial owners at various brokerages who may number in the thousands...

CEDE, who is the nominee holder of every share held in a brokerage account and counts as 1 shareholder of record

One of those "entities"---the nominee holder of every share held in brokerage accounts called CEDE---counts as 1 and represents thousands of shareholders...

incredible how, with ~500 shareholders of record, (one of whom is CEDE, the nominee of the DTC that is the legal owner of every street named shareholder's shares) anyone could even fathom a guess on this...

curious to see how today's 3 PTOI *trades* are marked

PTOI 8K Filed

Section 8 – Other Events

Item 8.01 Other Events

In light of the circumstances and uncertainty surrounding the effects of the COVID-19 coronavirus pandemic on the business, employees, consultants and service providers of Plastic2Oil, Inc. (the “Company”), the Company’s Board of Directors and management have determined that it will delay the filing of its quarterly report on Form 10-Q for the three months ended March 31, 2020 (the “Quarterly Report”) by up to 45 days in accordance with the SEC’s March 4, 2020 Order (Release No. 34-88318) (the “Order”), which allows for the delay of certain filings required under the Securities and Exchange Act of 1934, as amended. The Company’s operations and business have experienced disruption due to the unprecedented conditions surrounding the COVID-19 pandemic spreading throughout the United States and the world and thus the Company’s business operations have been disrupted and it is unable to timely review and prepare the Company’s financial statements for the 2019 fiscal year. As such, the Company will be making use of the 45-day grace period provided by the SEC’s Order to delay filing of its Annual Report. The Company plans to file its Quarterly Report by no later than June 29, 2020, 45 days after the original grace period due date (May 14, 2020) of its Quarterly Report.

https://www.sec.gov/Archives/edgar/data/13811...-index.htm

News News Alert: Current Report Filing (8-k) 05/14/2020 05:01:19 PM

SEC Charges Marijuana Stock Investors With Fraud

By Bill Alpert

April 17, 2020 11:52 am ET

A Massachusetts financier arranged to bring public a cannabis social-media company and then manipulated trading in its stock so he could unload his shares, a complaint by the Securities and Exchange Commission alleged last week. Douglas H. Leighton and a group of friends made more than $3 million when they later sold their shares of the stock, MassRoots, alleged the commission, with the group accounting for more than 60% of MassRoots trading in the week it came public in 2015.

The 51-year-old Leighton and his six co-defendants agreed to settle the SEC fraud charges, without admitting or denying them, by paying about $1.5 million in disgorgement and penalties. Subject to approval by the federal court in Boston, the agreement calls for Leighton to be barred from the securities industry, from holding office at a public company, or from trading in penny stocks.

“Over the past year, we have fully cooperated with the SEC’s civil inquiry into the trading of MassRoots’ securities,” Leighton’s lawyer Alan Rose Jr. told Barron’s in an email.

MassRoots (ticker: MSRT) described itself as “a semi-anonymous mobile network” where people could discuss cannabis use. While it said it had one million users for its software app, its securities filings showed that its business model of selling ads has never yielded more than a few hundred thousand dollars in cumulative revenue while producing tens of millions in losses. In its first month of trading in April 2015, MassRoots stock price briefly topped $7, giving the company a market value of $350 million. At that point, its cumulative revenue had totaled $1,465.

Today, MassRoots shares go for 0.14 cent each in over-the-counter trading, and the company‘s last securities filing in March 2020 said it lacked the funds needed to complete its accounting for the 2019 year. Barron’s queries to the company went unanswered.

Starting in the mid-1990s, Leighton had been a prolific penny-stock financier who found tiny companies, became their consultant, and got millions of shares in their stock before helping them come public. His firm Dutchess Capital claimed it had helped more than 400 companies raise $1 billion in all.

As more states began to legalize marijuana under their own laws in the past decade, penny-stock promoters sensed a new story to pitch retail investors. The major U.S. exchanges wouldn’t list cannabis stocks because of the weed’s federal illegality, but micro-cap stock names began trading over-the-counter in the U.S. and Canada several years before the marijuana stock bubble that accompanied Canada’s 2018 legalization.

The SEC’s complaint said that MassRoots came to Leighton’s attention in 2013. He invested $50,000 in the business and became its consultant for coming public, said the SEC. In return, Leighton and his firms received the rights to 23% of MassRoots stock, the complaint said. He instructed the company to hire certain brokers, lawyers, auditors, and stock promoters, while putting additional shares in the hands of associates through a private offering, the SEC added.

The complaint alleges that Leighton orchestrated his associates’ trading to artificially boost the stock’s price before unloading his own shares. The SEC alleged that Leighton and his confederates should have made Form 13-D filings that showed they were acting as a group.

According to the SEC’s suit, Leighton’s trading group made most of its money in the year after MassRoots’ public listing in April 2015, but it continued to profit from its alleged scheme through 2018, By then, the company had come to the attention of better-known investors in the accelerating marijuana industry.

A July 2018 securities filing by MassRoots registered 51 million shares the company had sold in the previous year to a number of investors.

Write to Bill Alpert at william.alpert@barrons.com

https://www.barrons.com/articles/sec-charges-marijuana-stock-investors-with-fraud-51587138778

SEC Charges Seven in Microcap Fraud Scheme

Litigation Release No. 24791 / April 8, 2020

Securities and Exchange Commission v. Douglas Leighton et al., No. 1:20-cv-10686 (D. Mass. filed April 7, 2020)

The Securities and Exchange Commission charged Massachusetts resident Douglas Leighton for a scheme in which he allegedly acquired discounted shares in a microcap company, knowingly failed to disclose his holdings and sales, and manipulated the public market for those shares. Leighton, two entities he controlled, and six investors he directed agreed to settlements ordering them to pay nearly $1.5 million in civil penalties, disgorgement, and prejudgment interest.

The SEC's complaint, filed in federal court in Boston, alleges that Leighton orchestrated the fraud after acquiring millions of shares in MassRoots, Inc., a cannabis-social-media company now based in Los Angeles, California. As alleged, when MassRoots began selling its shares to the public in April 2015, Leighton directed Michael Sullivan, David Hall, Zachary Harvey, Paul Dutra, Jason Harman, and Jessica Geran to manipulate the public market for MassRoots stock, including by making open-market purchases at specific volumes and prices to create an appearance of active trading in and increase the price of MassRoots stock. According to the complaint, Sullivan also used accounts at two separate broker dealers to further create an appearance of volume in and affect the price of MassRoots stock. The complaint further alleges that Leighton acquired and sold shares through Dutchess Opportunity Fund II LP, Azure Capital Corp., and Bass Point Capital LLC, which along with Leighton and the other defendants never disclosed to the investing public, through required SEC filings, their sales and significant ownership of MassRoots stock.

Leighton, Azure Capital, Bass Point, Sullivan, Hall, Harvey, Dutra, Harman, and Geran have agreed to settle the matter by consenting, without admitting or denying the SEC's allegations, to the entry of final judgments, which are subject to court approval. The judgments would permanently enjoin all of the defendants from violating the beneficial ownership reporting provisions of Sections 13(d) and 16(a) of the Securities Exchange Act of 1934 and Rules 13d-3 and 16a-1 thereunder; Leighton, Bass Point, Azure, and Sullivan from violating the antifraud provisions of Section 17(a) of the Securities Act of 1933; Leighton, Bass Point, and Azure from violating the antifraud provisions Section 10(b) of the Exchange Act and Rule 10b-5 thereunder; and Leighton and Sullivan from violating the market manipulation provisions of Section 9(a)(2) of the Exchange Act. In addition, the judgment would bar Leighton from serving as an officer or director of a public company and order him to pay a civil penalty of $160,000, and would bar Leighton, Azure Capital, and Bass Point from trading in penny stocks, impose a conduct-based junction restricting their future trading in any stock, and order them jointly and severally to pay disgorgement plus prejudgment interest of nearly $1 million. Leighton has also agreed to settle a follow-on administrative proceeding that bars him from the securities industry. Sullivan has agreed to be barred from trading in penny stocks for five years and to pay a civil penalty of $40,000 and disgorgement plus prejudgment interest of $63,228. The final judgments would order Hall, Harvey, Dutra, Harman, and Geran to pay civil penalties of $15,000 each, and would order payments of disgorgement plus prejudgment interest of $67,080 by Hall, $32,720 by Harvey, and $28,906 by Dutra.

The SEC's investigation was conducted by Jonathan Allen, Sofia Hussain, Alexander Pevzner, Rachel Hershfang, and Amy Gwiazda of the Boston Regional Office, with assistance from Robert Nesbitt in the SEC's Office of Market Intelligence. The investigation originated from an examination conducted out the Boston Regional Office by Marie Hagelstein, Kenneth Leung, and Mayeti Gametchu of the SEC's Office of Compliance Inspections and Examinations.

https://www.sec.gov/litigation/litreleases/2020/lr24791.htm

Unfortunately for you, part of that judgment involved a finding of proven falsity.

So, denying ENSSFM fantasies won't cut it as something to file a lawsuit over.

PTOI Historical ~ 11.25.19 - 2.28.20

PTOI ~ rough *volume* count for FEB 2020 ~ 993,682

NR = Just A Few Probs

02/28/2020 0.039 0.0423 0.036 0.036 45,953

02/27/2020 0.0381 0.0491 0.0381 0.041 244,505

02/26/2020 0.0488 0.0491 0.045 0.045 39,994

02/25/2020 0.05 0.05 0.0401 0.046 143,791

02/24/2020 0.051 0.053 0.0401 0.05 92,128

02/21/2020 0.05 0.054 0.05 0.051 63,673

02/20/2020 0.0595 0.0595 0.0595 0.0595 2,600

02/19/2020 0.0531 0.0531 0.052 0.0529 19,300

02/18/2020 0.052 0.06 0.052 0.059 23,380

02/14/2020 0.0625 0.0625 0.0516 0.0585 59,105

02/13/2020 0.0617 0.0617 0.0515 0.061 92,480

02/12/2020 0.052 0.061 0.052 0.061 5,750

02/11/2020 0.0523 0.0581 0.0523 0.0581 23,500

02/10/2020 0.061 0.061 0.0531 0.06 18,903

02/07/2020 0.053 0.0613 0.053 0.0532 21,650

02/06/2020 0.053 0.0615 0.053 0.053 29,755

02/05/2020 0.054 0.06 0.054 0.058 12,066

02/04/2020 0.059 0.06 0.053 0.0597 43,000

02/03/2020 0.054 0.0622 0.054 0.0622 12,149

PTOI ~ MM Monthly JAN 2020 ~ 1,363,463

01/31/2020 0.05 0.0595 0.05 0.0595 7,715

01/30/2020 0.05 0.06 0.05 0.0595 11,550

01/29/2020 0.05 0.0565 0.05 0.0565 9,516

01/28/2020 0.055 0.06 0.054 0.054 112,100

01/27/2020 0.065 0.065 0.0554 0.057 105,385

01/24/2020 0.06 0.06 0.0578 0.0578 3,188

01/23/2020 0.0555 0.0624 0.0555 0.0578 34,020

01/22/2020 0.0599 0.0599 0.0564 0.0599 28,460

01/21/2020 0.0625 0.067 0.0555 0.0595 113,278

01/17/2020 0.06 0.0685 0.059 0.059 71,716

01/16/2020 0.06 0.062 0.057 0.06 120,945

01/15/2020 0.063 0.0679 0.0594 0.06 18,104

01/14/2020 0.0645 0.0684 0.0585 0.0684 66,115

01/13/2020 0.07 0.07 0.0658 0.0675 91,272

01/10/2020 0.0512 0.084 0.0512 0.075 261,951

01/09/2020 0.0525 0.087 0.0525 0.086 58,112

01/08/2020 0.052 0.058 0.0466 0.0506 208,632

01/07/2020 0.0412 0.052 0.0412 0.052 16,000

01/06/2020 0.0525 0.0525 0.0466 0.052 15,700

01/03/2020 0.047 0.053 0.047 0.053 1,504

01/02/2020 0.0425 0.0465 0.039 0.0465 8,200

PTOI ~ MM Monthly DEC 2019 ~ 1,442,058

12/31/2019 0.0368 0.0455 0.0368 0.0425 56,072

12/30/2019 0.037 0.0434 0.037 0.0408 50,230

12/27/2019 0.037 0.0402 0.037 0.0402 24,160

12/26/2019 0.0445 0.0445 0.037 0.0415 174,849

12/24/2019 0.0485 0.0485 0.0422 0.0434 31,192

12/23/2019 0.0485 0.0485 0.0451 0.0485 9,338

12/20/2019 0.0427 0.0485 0.0426 0.0485 11,500

12/19/2019 0.048 0.048 0.0436 0.0436 36,150

12/18/2019 0.0508 0.0508 0.0495 0.0495 3,911

12/17/2019 0.05 0.063 0.0445 0.0512 38,775

12/16/2019 0.05 0.056 0.05 0.05 28,789

12/13/2019 0.057 0.057 0.0483 0.057 927

12/12/2019 0.057 0.057 0.057 0.057 45,000

12/11/2019 0.0532 0.06 0.05 0.0554 179,885

12/10/2019 0.06 0.065 0.05 0.0527 419,955

12/09/2019 0.058 0.065 0.058 0.065 43,050

12/06/2019 0.065 0.065 0.057 0.06 30,399

12/05/2019 0.065 0.065 0.056 0.0605 25,903

12/04/2019 0.06 0.0621 0.0553 0.06 37,595

12/03/2019 0.0595 0.0598 0.0471 0.0598 166,412

12/02/2019 0.05 0.0565 0.05 0.0565 27,966

PTOI ~ MM Monthly NOV 2019 ~ 8,847,829

11/29/2019 0.0486 0.06 0.0431 0.05 88,673

11/27/2019 0.056 0.06 0.05 0.0555 103,310

11/26/2019 0.0594 0.0595 0.056 0.0595 32,248

11/25/2019 0.05 0.06 0.05 0.0585 159,641

to reiterate .. as of the 10K (annual) filed last year

PTOI has 450 holders of record .. 1 of which is a CE (colluding entity)

that is the DTC .. that leaves 449 with certs not deposited in a brokerage firm

how prescient

suspect after NRs' set up of November 2019 .. which imo would have worked had NR been able to *run*

PTOI as they did back in April 2011 (80c to 3.00) to garner CONnections' interest back then .. this time

around NRs' set up fizzled .. all that effort for a *run* from 035c to 11c .. which would be *laughable* to the

CONnections NR desperately needed .. more revealing and rather ironic .. is the clamp that appears to have

come down from various CEs (colluding entities aka brokerage firms) .. re: *access* to P2O investors' shares

always telling to see *NRs' patterns* change out

Date Close High Low Volume Sht Vol % of Vol Shtd

Feb 28 NA NA NA 45,953 35,132 76.45%

Feb 27 NA NA NA 244,505 48,160 19.70%

Feb 26 NA NA NA 39,994 11,000 27.50%

Feb 25 NA NA NA 143,791 107,672 74.88%

Feb 24 NA NA NA 92,128 41,508 45.05%

Feb 21 NA NA NA 63,673 12,700 19.95%

Feb 20 NA NA NA 2,600 2,600 100.00%

Feb 19 NA NA NA 19,300 1,700 8.81%

Feb 18 NA NA NA 23,380 6,690 28.61%

Feb 14 NA NA NA 59,105 16,105 27.25%

Feb 13 NA NA NA 92,480 76,355 82.56%

Feb 12 NA NA NA 5,750 750 13.04%

Feb 11 NA NA NA 23,500 22,313 94.95%

Feb 10 NA NA NA 18,903 18,651 98.67%

Feb 07 NA NA NA 21,650 15,050 69.52%

Feb 06 NA NA NA 29,755 6,720 22.58%

Feb 04 NA NA NA 43,000 10,000 23.26%

Feb 03 NA NA NA 12,149 700 5.76%

Jan 31 NA NA NA 7,715 6,000 77.77%

suspect *CEs* (colluding entities) are wash trading (resetting) for *volume*

90 day volume avgs cliff dive @ EOM (NR loses November's set up effort)

PTOI 1,363,463 1,442,058 1,363,463 CDEL 593,406 1 43.52%

PTOI 1,363,463 1,442,058 1,363,463 ETRF 298,939 2 21.92%

PTOI 1,363,463 1,442,058 1,363,463 NITE 203,031 3 14.89%

PTOI 1,363,463 1,442,058 1,363,463 GTSM 134,110 4 9.84%

PTOI 1,363,463 1,442,058 1,363,463 CSTI 133,977 5 9.83%

P2O/PTOI .. this scenario may be helpful in understanding why Non Retail

embedded for over a decade in PTOI (stock) .. has angst

with P2O's ability to execute

first unlike many OTC targets (OTC is totally fungible)

P2O's founder originally accessed non toxic capital

to fund something many of us still deem jaw dropping

.. table top to Flagship in mere years .. this is significant

(far more so today than even 6 years or so ago)

it's why noting actual shareholder certs (449) vs the 1 held

via a CE .. aka colluding entities (DTC) .. matters ..

more on those CEs in a bit

the one and only time access to toxic capital came to

pass (aromatics) .. all with interest saw how their efforts'

played out .. shorting against their own certs .. seemingly

deliberate sabotage @ NF and padding certain like minded

entities' pockets over and over again

P2O was wrested back in mid August 2013 .. the newly installed

CEO infused Multiple Millions on 9.30.13 .. NRs' response to

that .. relentlessly compressing PTOI (stock) from 35c (9.30.13)

to 10c on 12.31.13

This is NRs' MO .. it is a very specific playbook Non Retail follows

in approximate order ..

NR works OTC target for cycles of money .. UP & DOWN

NR eventually goes UPSIDE DOWN

NR sanctions hit pieces .. usually in alignment with the

importation of a new *MM* (Market maker/market manipulator) to aid/abet (resetting)

Atty Firms' on hedgies' speed dial start trawling/trolling for *retail* lead plaintiff

and when that didn't *part* actual investors from their *shares* ..

NR works CONnections .. but to do that .. NR has to *expend effort*

that is what April 2011's then *record* setting volume (8M~ and change) was done for

that effort by NR took PTOI's PPS from approx 80c at the start of the month to 3.00 by EOM

by CONtrast .. NRs' recent *effort* (and set up) of November 2019 (new record setting volume month)

took PTOI from approx 035c to 11c .. which of course is why NR then focused effort against Nulixo specifically

NR works cycles of money .. making $ on the way and on the resets

back down .. this can work for weeks/months or years .. until it *CANT*

then NR brutalizes the stock

and why NR has such *angst* re: P2O/PTOI .. compressing X OTC target down to sub 1c

(again for most of the past many years .. PTOI has been held @ sub 6c) almost always

is successful in NR getting actual targets' shareholders to sell

so *extra effort* kicked in back in July 2010 .. it began the first of many *set ups*

that NR would inflict on P2O and her retail investors

then think about what happens when that doesn't work

for the most part .. my focus remains on what has come to pass since mid August 2013

a *clean slate* for NR so to speak .. re: PTOI (stock)

remember the 1 *cert* held out of the 450 total .. that 1 cert is the DTC (a CE)

the DTC holds every *share* traded on the open market via other CEs (colluding entities)

brokerage firms/insurance companies/banks .. any *entity* that trades *equities*

realize too what 450 works out to (avgs) for 125M~ (I/O) .. about 277,777 *shares* per

now we know that is *nonsense* because some actual P2O investors hold *respectively*

500k .. 750k .. 1.2M .. 1.5M .. 2M .. 2.5M .. 3M .. 3.3M .. and of course the CE (DTC) holds the

1 cert for every *NR entity* that holds equities ..

think about that .. er .. *imbalance* if X OTC target .. executes

so here is what *imo* has *changed* in the last 18 months .. give or take a month or two

for years various CEs (brokerage firms) loaned out (allowed NR to access for a $fee) ..

PTOI *shares* held in retail clients' cash accounts

now even tho' *various CE charters may say they don't allow for that* .. remember the adage

embedded for decades .. the OTC is fungible and no retail entity would ever know that

because the *more aware* brokerage firms/CEs .. would only be loaning out a % of the firms total held

so say for example .. one well known X CE/brokerage firm holds 16M PTOI *shares* in various retail accounts

software analysis reveals that for years only 1M of the 16M place GTCs to sell .. leaving 15M just sitting there

NRs' clients respective cash accounts

X brokerage isn't stupid .. they won't loan out (allow NR to access) PTOI for more than say 20%

of the 15M balance not set via GTCs (3M total *shares*) .. so this is done for years for a $fee ..

and this scheme works .. until something changes .. and various X brokerage firms (CEs) want the 20%

loan out *reduced* to 10%

now say the embedded NR entity having wiped their abusive slate clean with aromatics' flushed

out of P2O by EO 2014 .. (imo they didn't but for this example we'll say they did) .. went back to

their habit and systematically accumulated an abusive tally .. since 2015 .. so over the last 5 years or so ..

that abusive tally gets added to .. slowly/steadily .. even tho' PTOI saw *decreasing* volume YOY

from 2015 to 2016 to 2017 .. 2018 saw a slight volume increase over 2017 .. and of course we all know

what 2019's *volume* was (smidge under 24M~)

the volume done on PTOI over 4 years (2015 to 2018) comes in @ just under 70M

factor in 2019 and rounding down that volume (for simplicity's sake) the 5 year total = 92M

69,500,806 (2015/2016/2017/2018)

23,994,633 (2019)

--------------------

93,495,439 (2015 to 2019)

JUN 2019 ~ 491,063

JUL 2019 ~ 445,451

PTOI ~ NOV 2019 ~ 8,847,829

PTOI ~ DEC 2019 ~ 1,442,058

PTOI ~ JAN 2020 ~ 1,363,463

11/20/2019 0.07 0.0701 0.0503 0.0623 1,227,466

11/15/2019 0.094 0.11 0.076 0.095 1,423,292

11/14/2019 0.071 0.109 0.0675 0.0749 1,574,854

11/13/2019 0.053 0.0704 0.053 0.07 1,208,504

01/29/2019 0.0113 0.08 0.0103 0.02 1,046,642

06/22/2017 0.0176 0.0202 0.0112 0.019 1,143,831

first unlike many OTC targets (OTC is totally fungible)

P2O's founder originally accessed non toxic capital

to fund something many of us still deem jaw dropping

.. table top to Flagship in mere years .. this is significant

(far more so today than even 6 years or so ago)

Hoping for success with Nulixo amid opposition

I think Steve Price never foresaw the battle going on between pro and con within P2O. Why should he update into this toxic garbage dump. There is a lot of money to be made in this emerging market as we have seen with the recent 260 million dollar investment and I would bet he has encountered strong opposition from those trying to malign their own agenda. He and his team know what they’re doing. I think he is better off to get his ducks in a row then let the world in on his successful enterprise. Also plastic waste is a nuisance of disgust on our beautiful planet and the world will applaud the riddance of it. Good luck to the believers! Hang in there!

nice to see ..

of course it's not surprising it's out of Canada ..

may that migrate to the US b4 too much longer

just last week watched a NR entity working an SMB @ this site

illegally hack into a company's website to alter content

the DESPERATION by an UPSIDE DOWN NR (non retail) entity

after trying to control said OTC's target's *outcome* for over a decade now ..

is off the charts these days .. hmmm

thx for the link/read 7/10/11

4kids

Changes coming!!!

Anonymous internet trolls cannot hide behind a forum that encourages, enables, and empowers behavior as listed below...

https://www.blogto.com/city/2020/01/toronto-company-just-successfully-sued-some-anonymous-internet-trolls-over-100k/

Changes coming!!!

Anonymous internet trolls cannot hide behind a forum that encourages, enables, and empowers behavior as listed below...

https://www.blogto.com/city/2020/01/toronto-company-just-successfully-sued-some-anonymous-internet-trolls-over-100k/

PTOI >> MM Monthly November 2019

====================

PTOI *Volume by Month* 2019

JAN 2019 ~ PTOI 1,651,632 797,034 1,651,632 NITE 998,043 1 60.43% (7 reporting)

FEB 2019 ~ PTOI 2,076,767 1,651,632 3,728,399 NITE 918,349 1 44.22% (6 reporting)

MAR 2019 ~ PTOI 1,612,549 2,076,767 5,340,948 CDEL 670,739 1 41.59% (7 reporting)

APR 2019 ~ PTOI 2,499,579 1,612,549 7,840,527 NITE 1,049,696 1 41.99% (7 reporting)

MAY 2019 ~ PTOI 858,637 2,499,579 8,699,164 NITE 387,319 1 45.11% (7 reporting)

JUN 2019 ~ PTOI 491,063 858,637 9,190,227 CDEL 244,292 1 49.75% (6 reporting)

JUL 2019 ~ PTOI 445,451 491,063 9,635,678 ETRF 172,229 1 38.66% (5 reporting)

AUG 2019 ~ PTOI 772,572 445,451 10,408,250 CDEL 565,950 1 73.26% (6 reporting)

SEP 2019 ~ PTOI 1,107,189 772,572 11,515,439 ETRF 276,054 1 24.93% (7 reporting)

OCT 2019 ~ PTOI 2,189,307 1,107,189 13,704,746 CDEL 863,594 1 39.45% (6 reporting)

NOV 2019 ~ PTOI 8,847,829 2,189,307 22,580,375 CDEL 3,429,608 1 38.76% (9 reporting)

https://otce.finra.org/otce/marketStatistics/monthlyShareVolume

PTOI ~ November 2019 .. MM Monthly

PTOI 8,847,829 2,189,307 22,580,375 CDEL 3,429,608 1 38.76%

PTOI 8,847,829 2,189,307 22,580,375 NITE 2,199,843 2 24.86%

PTOI 8,847,829 2,189,307 22,580,375 ETRF 876,858 3 9.91%

PTOI 8,847,829 2,189,307 22,580,375 GTSM 831,542 4 9.40%

PTOI 8,847,829 2,189,307 22,580,375 ASCM 787,895 5 8.90%

PTOI 8,847,829 2,189,307 22,580,375 CSTI 494,365 6 5.59%

PTOI 8,847,829 2,189,307 22,580,375 CFGN 188,518 7 2.13%

PTOI 8,847,829 2,189,307 22,580,375 OTCX 38,000 8 0.43%

PTOI 8,847,829 2,189,307 22,580,375 INTL 1,200 9 0.01%

duly noted ~ ASCM/CFGN/INTL ~ importation for PTOI's *record* setting volume

month of November 2019 (which replaced April 2011's *set up* by NR) and of course CANT/GTSM

the given is the obvious .. timing tho' intriguing

PTOI Historical November 2019

(8,847,829) .. 0351c to 11c

11/29/2019 0.0486 0.06 0.0431 0.05 88,673

11/27/2019 0.056 0.06 0.05 0.0555 103,310

11/26/2019 0.0594 0.0595 0.056 0.0595 32,248

11/25/2019 0.05 0.06 0.05 0.0585 159,641

11/22/2019 0.06 0.0647 0.0545 0.0642 44,177

11/21/2019 0.0624 0.0639 0.055 0.059 125,735

11/20/2019 0.07 0.0701 0.0503 0.0623 1,227,466

11/19/2019 0.098 0.098 0.07 0.077 338,612

11/18/2019 0.09 0.109 0.0885 0.095 525,765

11/15/2019 0.094 0.11 0.076 0.095 1,423,292

11/14/2019 0.071 0.109 0.0675 0.0749 1,574,854

11/13/2019 0.053 0.0704 0.053 0.07 1,208,504

11/12/2019 0.047 0.059 0.047 0.059 451,420

11/11/2019 0.049 0.05 0.046 0.049 250,083

11/08/2019 0.036 0.046 0.036 0.045 444,222

11/07/2019 0.0372 0.0375 0.0372 0.0372 48,327

11/06/2019 0.0371 0.0371 0.0358 0.0371 41,378

11/05/2019 0.0352 0.0375 0.0352 0.0356 357,077

11/04/2019 0.036 0.0375 0.0354 0.0355 400,141

11/01/2019 0.0351 0.0351 0.0351 0.0351 2,904

PTOI Historical April 2011

APR ~ Total Share Volume 8,093,592/to this day PTOI's *record* setting volume .. $set up .. 82c to 3.00

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=128315021

04/29/2011 2.24 3.00 2.05 2.78 417,170

04/28/2011 1.96 2.25 1.94 2.25 174,529

04/27/2011 1.57 2.05 1.55 1.92 392,824

04/26/2011 1.59 1.64 1.52 1.61 285,316

04/25/2011 1.87 1.87 1.68 1.68 286,864

04/21/2011 1.22 1.84 1.05 1.84 736,234

04/20/2011 1.96 2.08 1.17 1.26 949,402

04/19/2011 2.15 2.15 2.00 2.14 171,325

04/18/2011 2.05 2.17 2.05 2.14 131,592

04/15/2011 2.20 2.25 2.00 2.17 234,742

04/14/2011 2.10 2.32 1.90 2.25 375,545

04/13/2011 2.21 2.38 1.88 2.3 692,446

04/12/2011 1.80 2.12 1.78 2.12 686,209

04/11/2011 1.40 1.93 1.30 1.75 907,578

04/08/2011 1.10 1.24 1.04 1.24 220,368

04/07/2011 1.05 1.14 0.96 1.11 160,793

04/06/2011 1.01 1.10 0.98 1.05 155,038

04/05/2011 1.07 1.07 0.95 1.00 322,332

04/04/2011 0.88 1.13 0.85 1.04 658,574

04/01/2011 0.84 0.85 0.82 0.85 138,711

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=145949296

4kids

PTOI 10Q Filed News Alert: Quarterly Report (10-q) 12/16/2019 04:32:48 PM

https://www.sec.gov/Archives/edgar/data/1381105/000149315219019294/form10-q.htm

World's largest pension fund halts stock lending to short sellers

Reuters By Tim Kelly

TOKYO (Reuters) - Japan's Government Pension Investment Fund (GPIF), the world's largest pension fund, has suspended stock lending for short selling, calling the practice inconsistent with its responsibilities as a long-term investor.

The move, announced by the GPIF on Tuesday, is a blow for short sellers, who rely on securities lending to bet against companies and who are facing renewed moves in a number of countries to curb their activities.

"The current stock lending scheme lacks transparency in terms of who is the ultimate borrower and for what purpose they are borrowing," the GPIF said on its website.

The move by the fund will affect shares in its 42.5 trillion yen ($391.20 billion) foreign equities portfolio.

Japanese and overseas shares account for half of the GPIF's 160 trillion yen worth of assets. It said it will continue to lend debt securities and may reconsider the halt to foreign stock lending if it sees an improvement in transparency. It does not lend its holdings of domestic shares.

Short sellers borrow shares and immediately sell them, betting the price will fall before they buy back the shares and return them, pocketing the difference.

Advocates see them as a healthy counterbalance to investor over-confidence and corporate spin. Critics argue they are destabilising because they have an incentive to drive down a company's share price.

Elon Musk, the chief executive of Tesla, a popular target for short sellers, was quick to applaud the GPIF's move.

"Bravo, right thing to do! Short selling should be illegal," the high tech entrepreneur said in a tweet.

Musk has previously criticised fund managers for lending shares for hedge funds to short, saying the fund firms made "excessive profit" from the practice.

Securities lending has emerged as a small but significant source of extra returns for funds. GPIF earned 37.58 billion yen ($345.91 million) in fees from lending shares from its foreign equity portfolio over three years to the end of its 2018 financial year.

BlackRock, the world’s largest asset manager, reported total securities lending revenue of $597 million in 2017, compared with $579 million in 2016, according to a securities filing.

In the July-September quarter, GPIF reported a profit of 1.8 trillion yen. Amid Japan's ultra-low interest rates, the fund, which is closely watched by global investors, has retreated from unprofitable domestic bonds in favour of foreign assets.

($1 = 108.6400 yen)

(Additional reporting by Takashi Umekawa in Tokyo; editing by Andrew Heavens, Larry King and Carmel Crimmins)

https://www.yahoo.com/finance/news/worlds-largest-pension-fund-halts-124400162.html

PTOI >> MM Monthly October 2019 PTOI 1,107,189 772,572 11,515,439 ARCA 16,300 6 1.47% 09:55:20 0.0171 16300 OTO .. targeted trade done below 0185 *bid* 09:30:14 0.0248 16300 OTO .. hidden (B/024/34250 .. A/028/165797)

ah yes .. the *scam* of NR (non retail) who illegally manipulate OTC targets by rote .. ;)

reminder .. GTSM/CANT

reminder .. (July 2019) PTOI had the lowest *volume* reported by Non Retail (NR) in 2019

with the then classic NR ploy of parking decoy OTCX on bid and ask almost daily ..

ECN for hire swapped out in October .. ARCA replaced OTCX for *last position reporting of 16300*

interesting to note the 16300 was also done on 9.24.19 .. and noted in September MM Monthly by ARCA

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=151577734

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=151360381

https://otctransparency.finra.org/otctransparency/AtsIssueData

October's version was done on 10.9.19

https://investorshub.advfn.com/boards/replies.aspx?msg=151596308

====================

PTOI *Volume by Month* 2019

JAN 2019 ~ PTOI 1,651,632 797,034 1,651,632 NITE 998,043 1 60.43% (7 reporting)

FEB 2019 ~ PTOI 2,076,767 1,651,632 3,728,399 NITE 918,349 1 44.22% (6 reporting)

MAR 2019 ~ PTOI 1,612,549 2,076,767 5,340,948 CDEL 670,739 1 41.59% (7 reporting)

APR 2019 ~ PTOI 2,499,579 1,612,549 7,840,527 NITE 1,049,696 1 41.99% (7 reporting)

MAY 2019 ~ PTOI 858,637 2,499,579 8,699,164 NITE 387,319 1 45.11% (7 reporting)

JUN 2019 ~ PTOI 491,063 858,637 9,190,227 CDEL 244,292 1 49.75% (6 reporting)

JUL 2019 ~ PTOI 445,451 491,063 9,635,678 ETRF 172,229 1 38.66% (5 reporting)

AUG 2019 ~ PTOI 772,572 445,451 10,408,250 CDEL 565,950 1 73.26% (6 reporting)

SEP 2019 ~ PTOI 1,107,189 772,572 11,515,439 ETRF 276,054 1 24.93% (7 reporting)

OCT 2019 ~ PTOI 2,189,307 1,107,189 13,704,746 CDEL 863,594 1 39.45% (6 reporting)

PTOI ~ October 2019 .. MM Monthly

PTOI 2,189,307 1,107,189 13,704,746 CDEL 863,594 1 39.45%

PTOI 2,189,307 1,107,189 13,704,746 ETRF 522,017 2 23.84%

PTOI 2,189,307 1,107,189 13,704,746 NITE 375,484 3 17.15%

PTOI 2,189,307 1,107,189 13,704,746 GTSM 306,088 4 13.98%

PTOI 2,189,307 1,107,189 13,704,746 CSTI 105,824 5 4.83%

PTOI 2,189,307 1,107,189 13,704,746 ARCA 16,300 6 0.74%

https://otce.finra.org/otce/marketStatistics/monthlyShareVolume

PTOI Volume by Month July 2018 ~ October 2019

JUL 2018 ~ 1,198,826 .. 2018 YTD Volume ~ 7,810,868

AUG 2018 ~ 2,328,321 .. highest volume month 2018

SEP 2018 ~ 1,225,259

OCT 2018 ~ 1,023,420 .. 2018 YTD Volume ~ 12,387,868

NOV 2018 ~ 739,525

DEC 2018 ~ 797,034 .. 2018 YTD Volume ~ 13,924,427

JAN 2019 ~ 1,651,632 .. 604,990 sans 1.29.19's *volume*

FEB 2019 ~ 2,076,767 .. note 2M + 400k = 2.4M~

MAR 2019 ~ 1,612,549 .. note 1.6M identical to Jan 2019 (washed effort)

APR 2019 ~ 2,499,579 .. highest volume in 2019 (note 2.4M - 400k = 2M)

MAY 2019 ~ 858,637 .. 2019 YTD Volume ~ 8,699,164

JUN 2019 ~ 491,063 .. 2019 YTD Volume ~ 9,190,227

JUL 2019 ~ 445,451 .. lowest volume month in 2019 .. 2019 YTD Volume ~ 9,635,678

AUG 2019 ~ 772,572 .. 2019 YTD Volume ~ 10,408,250

SEP 2019 ~ 1,107,189 .. 2019 YTD Volume ~ 11,515,439

OCT 2019 ~ 2,189,307 .. 2019 YTD Volume ~ 13,704,746

PTOI Volume by Month January 2017 ~ June 2018

JAN 2017 = 511,955

FEB 2017 = 507,372

MAR 2017 = 621,468

APR 2017 = 341,667 .. lowest volume month 2017

MAY 2017 = 1,975,943

JUN 2017 = 3,220,064 .. 1M+ volume day on 6.22.17 .. next 1M+ volume day on 1.29.19

JUL 2017 = 478,262

AUG 2017 = 1,167,489

SEP 2017 = 480,903

OCT 2017 = 1,848,518

NOV 2017 = 757,927

DEC 2017 = 1,629,015

JAN 2018 = 2,039,578 .. (London Calling front half Jan imo approx 750,000 shares)

FEB 2018 = 510,679

MAR 2018 = 404,356 .. lowest volume month 2018

APR 2018 = 622,409

MAY 2018 = 1,983,852

JUN 2018 = 1,051,168

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=145949296

hmmm

4kids

SEC Charges 18 Traders in $31 Million Stock Manipulation Scheme

FOR IMMEDIATE RELEASE

2019-216

Washington D.C., Oct. 16, 2019 —

The Securities and Exchange Commission has filed an emergency action and obtained an asset freeze against 18 traders in a scheme to manipulate more than 3,000 U.S.-listed securities for over $31 million in illicit profits.

The SEC alleges that the traders, who are primarily based in China, manipulated the prices of thousands of thinly traded securities by creating the false appearance of trading interest and activity in those stocks, thereby enabling them to reap illicit profits by artificially boosting or depressing stock prices. For example, according to the SEC's complaint, the traders used multiple accounts to place several small sell orders to drive down a stock’s price before using a different set of accounts to buy larger amounts of the stock at the artificially low prices. After accumulating their position, the traders then flipped the script and placed several small buy orders to push up prices so they could then sell their stock at artificially high prices.

"We allege that defendants engaged in an extensive manipulation scheme and went to great lengths to evade detection, placing trades in over one hundred separate accounts at several different brokerage firms and submitting falsified documents to open new accounts in the names of others," said Joseph G. Sansone, Chief of the SEC's Market Abuse Unit. "Despite their efforts, the SEC staff was able to uncover the connections between these seemingly unrelated accounts and expose the defendants' coordinated pattern of illicit trading."

In a parallel action, the U.S. Attorney's Office for the District of Massachusetts announced criminal charges against two of the traders, Jiali Wang and Xiaosong Wang.

The SEC's complaint filed in federal court in Boston and unsealed today, charges the traders with violating and aiding and abetting violations of the antifraud provisions of the securities laws. In addition to the asset freeze and other emergency relief obtained, the SEC seeks disgorgement of ill-gotten gains plus interest, penalties, and injunctive relief.

The SEC's investigation was conducted by Andrew Palid and Michele T. Perillo of the SEC's Market Abuse Unit in the Boston Regional Office with assistance from John Marino of the Market Abuse Unit, and was supervised by Mr. Sansone. The litigation will be led by Eric Forni of the Boston Regional Office and Mr. Palid. The SEC appreciates the assistance of the U.S. Attorney's Office for the District of Massachusetts, the Federal Bureau of Investigation, and the Financial Industry Regulatory Authority.

https://www.sec.gov/news/press-release/2019-216

original link courtesy of thepennyguru

PTOI 8K FILED News News Alert: Current Report Filing (8-k) 10/08/2019 05:17:38 PM

Item 1.01 Entry into a Material Definitive Agreement.

On October 2, 2019, Plastic2Oil, Inc., a Nevada corporation (the “Company”), entered into an agreement (“Agreement”) with Nulixo, Inc. (the “Buyer”), whereby the Buyer agreed to appoint the Company as the exclusive supplier for plastic to oil processors for a period of twenty (20) years. Specifically, the Buyer agrees to purchase at least eight (8) processors over a period of three (3) years, and at least one (1) to be ordered upon the effectiveness of the Agreement. Pursuant to the first purchase order, for which the company is awaiting initial funding of the purchase order, the Buyer ordered two (2) processors for Six Million Dollars ($6,000,000) with an initial payment of Three Million Dollars ($3,000,000). Any subsequent processor purchased shall be at a fixed rate of ($3,000,000). In addition, the Company has further agreed to provide monitoring and servicing services for a fee to be determined on a case by case basis.

https://www.sec.gov/Archives/edgar/data/1381105/000149315219015252/form8-k.htm

==================

curious to see re: RC's Master Agreement

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=140571930

reminder .. HM

http://heddleshipyards.com/

PTOI >> MM Monthly September 2019

ah yes .. the *scam* of NR (non retail) who illegally manipulate OTC targets by rote .. ;)

interesting to see that 24% for September 2019 .. wash trading 101 by Non Retail .. see below

reminder .. GTSM/CANT

reminder .. (July 2019) PTOI had the lowest *volume* reported by Non Retail (NR) in 2019

with the classic NR ploy of parking decoy OTCX on bid and ask almost daily ..

with nary one trade *reported* by OTCX for the entire month of July .. OCTX mirrored ETRF in August

and last month .. OCTX came in 7th out of 7 (September 2019) .. (5,304 7 0.48%)

JAN 2019 ~ PTOI 1,651,632 797,034 1,651,632 NITE 998,043 1 60.43% (7 reporting)

FEB 2019 ~ PTOI 2,076,767 1,651,632 3,728,399 NITE 918,349 1 44.22% (6 reporting)

MAR 2019 ~ PTOI 1,612,549 2,076,767 5,340,948 CDEL 670,739 1 41.59% (7 reporting)

APR 2019 ~ PTOI 2,499,579 1,612,549 7,840,527 NITE 1,049,696 1 41.99% (7 reporting)

MAY 2019 ~ PTOI 858,637 2,499,579 8,699,164 NITE 387,319 1 45.11% (7 reporting)

JUN 2019 ~ PTOI 491,063 858,637 9,190,227 CDEL 244,292 1 49.75% (6 reporting)

JUL 2019 ~ PTOI 445,451 491,063 9,635,678 ETRF 172,229 1 38.66% (5 reporting)

AUG 2019 ~ PTOI 772,572 445,451 10,408,250 CDEL 565,950 1 73.26% (6 reporting)

SEP 2019 ~ PTOI 1,107,189 772,572 11,515,439 ETRF 276,054 1 24.93% (7 reporting)

note if one adds the first 3 *reporting* to Finra for September 2019 .. % comes to 72.48% .. 73.26 - 72.48 = 0.78 (difference of)

PTOI 1,107,189 772,572 11,515,439 ETRF 276,054 1 24.93%

PTOI 1,107,189 772,572 11,515,439 NITE 266,099 2 24.03%

PTOI 1,107,189 772,572 11,515,439 CDEL 260,456 3 23.52%

PTOI 1,107,189 772,572 11,515,439 GTSM 239,787 4 21.66%

PTOI 1,107,189 772,572 11,515,439 CSTI 43,189 5 3.9%

PTOI 1,107,189 772,572 11,515,439 ARCA 16,300 6 1.47%

PTOI 1,107,189 772,572 11,515,439 OTCX 5,305 7 0.48%

https://otce.finra.org/otce/marketStatistics/monthlyShareVolume

PTOI Volume July 2018 to September 2019

JUL 2018 ~ 1,198,826 .. 2018 YTD Volume ~ 7,810,868

AUG 2018 ~ 2,328,321 .. highest volume month 2018

SEP 2018 ~ 1,225,259

OCT 2018 ~ 1,023,420 .. 2018 YTD Volume ~ 12,387,868

NOV 2018 ~ 739,525

DEC 2018 ~ 797,034 .. 2018 YTD Volume ~ 13,924,427

JAN 2019 ~ 1,651,632 .. 604,990 sans 1.29.19's *volume*

FEB 2019 ~ 2,076,767 .. note 2M + 400k = 2.4M~

MAR 2019 ~ 1,612,549 .. note 1.6M identical to Jan 2019 (washed effort)

APR 2019 ~ 2,499,579 .. highest volume in 2019 (note 2.4M - 400k = 2M)

MAY 2019 ~ 858,637 .. 2019 YTD Volume ~ 8,699,164

JUN 2019 ~ 491,063 .. 2019 YTD Volume ~ 9,190,227

JUL 2019 ~ 445,451 .. lowest volume month in 2019 .. 2019 YTD Volume ~ 9,635,678

AUG 2018 ~ 772,572 .. 2019 YTD Volume ~ 10,408,250

SEP 2018 ~ 1,107,189 .. 2019 YTD Volume ~ 11,515,439

PTOI Volume January 2017 to June 2018

JAN 2017 = 511,955

FEB 2017 = 507,372

MAR 2017 = 621,468

APR 2017 = 341,667 .. lowest volume month 2017

MAY 2017 = 1,975,943

JUN 2017 = 3,220,064 .. 1M+ volume day on 6.22.17 .. next 1M+ volume day on 1.29.19

JUL 2017 = 478,262

AUG 2017 = 1,167,489

SEP 2017 = 480,903

OCT 2017 = 1,848,518

NOV 2017 = 757,927

DEC 2017 = 1,629,015

JAN 2018 = 2,039,578 .. (London Calling front half Jan imo approx 750,000 shares)

FEB 2018 = 510,679

MAR 2018 = 404,356 .. lowest volume month 2018

APR 2018 = 622,409

MAY 2018 = 1,983,852

JUN 2018 = 1,051,168

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=145949296

hmmm

4kids

Short Sale Circuit Breaker

The SEC adopted amendments to Regulation SHO with a compliance date of November 10, 2010. Among the rule changes, the SEC introduced Rule 201 (Alternative Uptick Rule), a short sale-related circuit breaker that when triggered, will impose a restriction on prices at which securities may be sold short. The SEC also issued guidance for broker-dealers wishing to mark certain qualifying orders 201cshort exempt.201d For more details, refer to Amendments to Regulation SHO (Release 34-61595).

Trade Date Download Link File Creation Timestamp

Friday, October 4,2019

Download

10/4/2019 4:15:26 AM

Symbol Security Name Market Category Trigger Time

GPRO GoPro, Inc. Class A Common St Q 10/3/2019 9:30:00 AM

TC TuanChe Limited ADS R 10/3/2019 9:30:00 AM

CFFAW CF Finance Acquisition Wt R 10/3/2019 9:30:00 AM

AXTI AXT Inc Q 10/3/2019 9:30:00 AM

ANGO AngioDynamics, Inc. Q 10/3/2019 9:30:00 AM

ENLV Enlivex Therapeutics Ltd. R 10/3/2019 9:30:00 AM

JAGX Jaguar Health, Inc. Cmn R 10/3/2019 9:30:00 AM

MTFB Motif Bio plc ADR R 10/3/2019 9:30:01 AM

RECN Resources Connection Inc Q 10/3/2019 9:30:03 AM

SES Synthesis Energy Sytems Inc R 10/3/2019 9:30:57 AM

PNTG The Pennant Group, Inc. Q 10/3/2019 9:31:15 AM

SQBG Sequential Brands Group Cmn R 10/3/2019 9:31:26 AM

SNNA Sienna Biopharmaceuticals Cmn Q 10/3/2019 9:31:45 AM

PSTVZ PLUS THERAPEUTICS, Wts R 10/3/2019 9:32:43 AM

MESO Mesoblast Limited ADS Q 10/3/2019 9:33:43 AM

OCGN Ocugen, Inc. Common Stock R 10/3/2019 9:33:53 AM

CYRXW CryoPort, Inc. Warrants R 10/3/2019 9:36:06 AM

AMRH Ameri Holdings, Inc. Cm St R 10/3/2019 9:37:35 AM

RVLT Revolution Lighting Tech Cmn R 10/3/2019 9:41:48 AM

QRTEB Qurate Retail Sr B Cm Q 10/3/2019 9:45:00 AM

SCON SUPERCONDUCTOR TECH R 10/3/2019 9:46:07 AM

DEST Destination Maternity Cp Q 10/3/2019 9:46:16 AM

AMRS Amyris, Inc. Q 10/3/2019 9:46:50 AM

MOSY MoSys, Inc. R 10/3/2019 9:48:03 AM

BCYC Bicycle Therapeutics plc ADS Q 10/3/2019 9:52:17 AM

CTXRW Citius Pharmaceuticals Wt R 10/3/2019 9:53:19 AM

DLPNW Dolphin Entertainment, WTS R 10/3/2019 9:59:19 AM

NAKD Naked Brand Group Limited Ord R 10/3/2019 10:00:40 AM

CGIX Cancer Genetics, Inc. R 10/3/2019 10:01:23 AM

NDRAW ENDRA Life Sciences Inc. WT R 10/3/2019 10:02:19 AM

TLGT Teligent, Inc. Common Stock Q 10/3/2019 10:03:55 AM

QUIK QuickLogic Corporation R 10/3/2019 10:03:59 AM

HYACW Haymaker Acq Corp. II Warrant R 10/3/2019 10:09:23 AM

XSPA XpresSpa Group, Inc. R 10/3/2019 10:11:20 AM

DMTKW DermTech, Inc. Warrant R 10/3/2019 10:13:14 AM

GSM Ferroglobe PLC OS Q 10/3/2019 10:13:59 AM

PHIO Phio Pharmaceuticals Corp. R 10/3/2019 10:15:10 AM

BNTC Benitec Biopharma Ltd ADS R 10/3/2019 10:15:57 AM

TROV TrovaGene, Inc. Common Stock R 10/3/2019 10:17:33 AM

BVSN BroadVision Inc R 10/3/2019 10:18:47 AM

LIVX LiveXLive Media, Inc. Cm St R 10/3/2019 10:21:29 AM

STNLW Sentinel Energy Services WT R 10/3/2019 10:23:02 AM

FAMI Farmmi, Inc. Ordinary Shs R 10/3/2019 10:25:27 AM

VXRT Vaxart, Inc. R 10/3/2019 10:38:56 AM

VRML Vermillion, Inc. R 10/3/2019 10:43:40 AM

NNDM Nano Dimension Ltd ADS R 10/3/2019 10:47:31 AM

SAUC Diversified Restaurant Hldgs R 10/3/2019 10:47:43 AM

STKL SunOpta, Inc Q 10/3/2019 11:05:00 AM

OTLKW Outlook Therapeutics Ser A Wt R 10/3/2019 11:06:24 AM

CUR Neuralstem, Inc. Common Stock R 10/3/2019 11:35:13 AM

TKKSW TKK Symphony Acquisition WT R 10/3/2019 11:51:32 AM

APEX Apex Global Brands Inc. R 10/3/2019 11:51:55 AM

ALIM Alimera Sciences Inc Q 10/3/2019 11:57:12 AM

CREX Creative Realities Inc. Cmn R 10/3/2019 12:05:06 PM

THOR Synthorx Inc Cmn Stk Q 10/3/2019 12:05:44 PM

MHLD Maiden Holdings, Ltd. Q 10/3/2019 12:10:35 PM

THCAW Tuscan Holdings Corp. II Wt R 10/3/2019 12:20:11 PM

PETZ TDH Holdings, Inc. Cmn Shrs R 10/3/2019 12:23:19 PM

GNPX Genprex, Inc. CM R 10/3/2019 12:30:18 PM

HSACW Health Sciences Acq Warrants R 10/3/2019 12:46:30 PM

RAVE Rave Restaurant Group, Inc. R 10/3/2019 12:47:31 PM

THWWW Target Hospit Cp Wts R 10/3/2019 12:58:43 PM

KZIA Kazia Therapeutics Limited ADS R 10/3/2019 1:04:41 PM

INPX Inpixon Common Stock R 10/3/2019 1:35:42 PM

TBLTW ToughBuilt Ind Warrant R 10/3/2019 1:50:23 PM

JFU 9F Inc. ADS Q 10/3/2019 1:58:23 PM

EYEGW Eyegate Pharmaceuticals Wts R 10/3/2019 2:01:32 PM

WAFU Wah Fu Education Group Ltd Ord R 10/3/2019 2:15:37 PM

ARTL Artelo Biosciences, Inc. CS R 10/3/2019 2:17:09 PM

EYEG Eyegate Pharmaceuticals Cm R 10/3/2019 2:43:17 PM

USWSW U.S. Well Services, Inc. Wts R 10/3/2019 3:06:05 PM

LKCO Luokung Technology Ord Shs R 10/3/2019 3:24:25 PM

DEACW Diamond Eagle Acquisition WTS R 10/3/2019 3:36:13 PM

HHHHW Wealthbridge Acquisitn Ltd Wts R 10/3/2019 3:40:16 PM

PLL Piedmont Lithium Limited ADS R 10/3/2019 3:44:51 PM

PHUNW Phunware, Inc. Warrants R 10/3/2019 3:53:09 PM

HHHHR Wealthbridge Acquistn Ltd Rts R 10/3/2019 3:59:26 PM

TAST Carrols Restaurant Group, Inc. Q 10/3/2019 3:59:34 PM

IPIX ..

truly worth *digesting* the last week or so of IPIX *trades*

there are a few things that a decade of observation and documentation has revealed to me

first and foremost .. NR/CEs do not want an educated retail investor

a decade ago (b4 2 events in 2010 came to pass .. Finra's live DRS link and May 2010's flash crash

when then SEC Chair had to publicly admit that in May 2010 that the SEC had no way to reconstruct

any trade .. regardless of where *traded* .. but rather the SEC had to rely on the various brokerage firms

yada yada for that info) .. that it was *easy* to CON retail via SMBs .. NRs' embeds and trading crews

had a slick op whereby .. literally very specific *aliases* could show up on a SMB .. and retail would sell first and ask questions second ..

that *controlled outcome* started to change as the rot of the system was revealed from 2008 into 2010

what has been more disgusting to me .. has been to watch those who *normalize* the abnormal ..

(basically trying to condition by rote) legitimize the illegal manipulation .. and those who aid and abet

those specific entities who rig the game by rote (SEC/DTCC the list goes on for a while)

on any given day for years now *imo* .. IPIX has max 20% retail .. 80% non retail

this NR entity *imo* (probably at least 2 maybe 3) .. has for years now tried to kill off the company ..

NRs' hand off from last significant take up @ EO 2014 .. into 2015

when Overstock/OSTK took on GS (and *imo* most of what has been done against targets and retail) has been by a loosely woven network (i used to call it the old

boy network) .. that ran .. if memory serves .. about 5 years and about $20Million in discovery costs .. part of discovery is ascertaining who is behind the trades (clearly excluding retail investors here)

this is why *documentation* is despised by Non Retail and their minions

I get frustrated when folks I respect use words like *slop* or mischief as if this shit

is innocent in nature ..

it is anything but ..

these SOBs don't give a damn about what the *target* does .. it could be life saving science .. or life altering technology ..

they don't care .. literally

to those who illegally rig the game .. it always comes down to being upside down and trying to kill the target .. no matter how long it takes

======

last week an LT IPI investor asked me about *wash trading and resets*

i view them as 2 separate categories that can occasionally overlap ..

this morning another IPI investor sent me this:

some of you may recognize her name .. I watched her for years as a guest on CNBC

Naked, Short and Greedy

Wall Street's Failure to Deliver

By Susanne Trimbath

https://spiramus.com/naked-short-and-greedy

new book due out ..

here is a tweet from Ms. Trimbath

True. NSCC resubmits all fails so they get a new start date the next morning. Fails went dark pool after Reg SHO put them in the spotlight. NYSE member balance sheets still report hundreds of billions in FTDs and FTRs that don't show up in NSCC/SEC numbers.

resubmits all fails so they get a new start date the next morning

Naked, Short and Greedy resubmits all fails so they get a new start date the next morning

Wall Street's Failure to Deliver

By Susanne Trimbath

https://spiramus.com/naked-short-and-greedy

new book due out ..

here is a tweet from Ms. Trimbath (watched her appearances .. years .. on CNBC)

True. NSCC resubmits all fails so they get a new start date the next morning. Fails went dark pool after Reg SHO put them in the spotlight. NYSE member balance sheets still report hundreds of billions in FTDs and FTRs that don't show up in NSCC/SEC numbers.

i refer to this:

as *resets r possible* .. as in CEs' (colluding entities) reset start date ..