Small caps outperform ahead of Labor Day By Almanac Trader | August 15, 2017

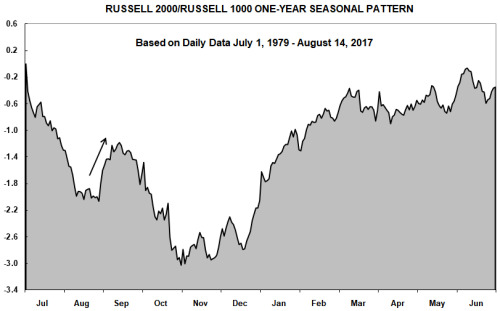

In the following chart, thirty-eight years of daily data for the Russell 2000 index of smaller companies are divided by the Russell 1000 index of largest companies, and then compressed into a single year to show an idealized yearly pattern. When the graph is descending, large-cap companies are outperforming small-cap companies; when the graph is rising, smaller companies are moving up faster than their larger brethren. The most prominent period of outperformance generally begins in mid-December and lasts until late-February or early March with a surge in January. This time of outperformance by small-caps is known as the “January Effect.”

In recent years, another sizable move is quite evident just before Labor Day. One possible explanation for this move is individual investors begin to return to work after summertime vacations and are searching for “bargain” stocks. In a typical year, small-caps would have been lagging and could represent an opportunity relative to other large-cap possibilities. As of today’s close, Russell 2000 is up 1.9% compared to the Russell 1000 being up 9.8% year-to-date. However, the small-cap advantage does wane around mid-September.

Click on "In reply to", for Authors past commentaries

Information posted to this board is not meant to suggest any specific action, but to point out the technical signs that can help our readers make their own specific decisions. Your Due Dilegence is a must! • DiscoverGold

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

News

News  Market Data

Market Data  Discover

Discover